In the movie Titanic from 1997, when the ship has struck the iceberg, Captain Smith asks the ship’s designer, Mr. Andrews, how much time the pumps will buy him. Mr. Andrews replies: “minutes only.”

As a political economist focused on the fiscal affairs of modern welfare states, there are days when I feel like Mr. Andrews. Today is one of those days, as I watch the U.S. government struggle to get a grip on its runaway debt.

To stick to the Titanic metaphor, the government has already hit the iceberg. The budget deficit is the hole through which water is rushing in. The investors who express increasingly alarming concerns about the rising debt are the rising water levels that threaten to engulf the ship and sink it.

Instead of doing what needs to be done to stop the sinking, i.e., to avoid a fiscal crisis, Congress and the U.S. Treasury are both engaged in time-buying activities. Their hands are on the proverbial pumps that will put off the inevitable just a little bit longer.

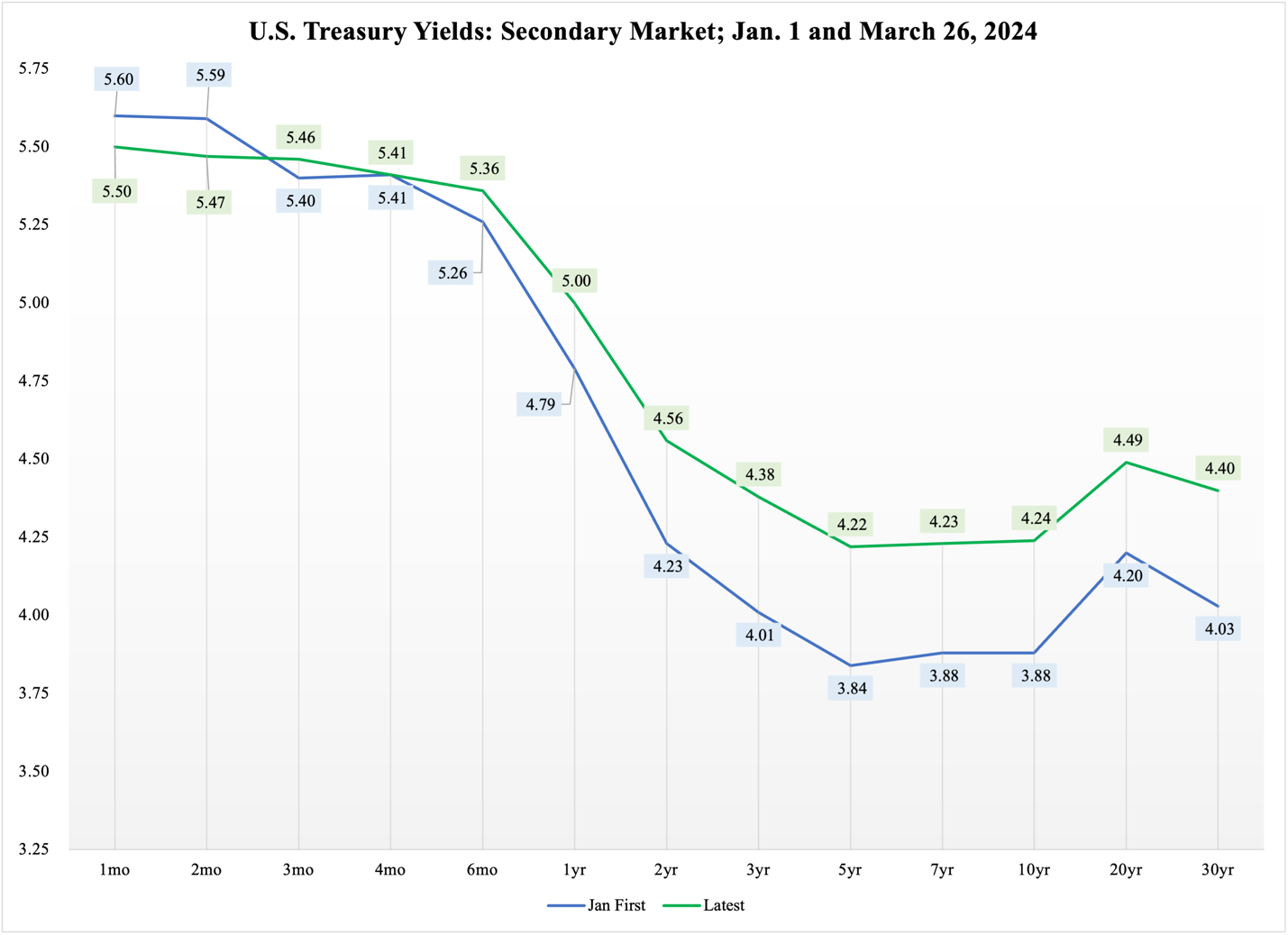

One of the many reasons why investors have signaled their worries is that the cost of the debt is rising faster than the debt itself. This, in turn, is due in part to how the U.S. Treasury has managed its debt. For reasons that elude rational analysis, they have insisted on selling an increasing share of their debt as Treasury bills that mature in one year or less. These securities come with the highest interest rates; normally, longer-term debt costs more, but that is not the world we live in currently.

Figure 1 reports the secondary-market yields on all the maturity classes of U.S. Treasury debt. The blue line represents the yields on January 1st; the green line reports the ‘latest’ yields, in this case, March 26th:

Figure 1

Due to the higher yields on short-term debt, the Treasury has unnecessarily pushed the total debt cost higher than it needs to be. A change for the better seemed to be on its way when on February 1st, the U.S. Treasury announced that they were going to shift new debt sales from short maturities to Treasury notes with a maturity date between 2 and 7 years.

So far, we have not seen many signs of this strategy at work. Therefore, it was only logical that investors continued to express uneasiness with the rising debt. Likewise, it was not surprising when the sovereign debt market sent clear signals of worry. Their eyes were on both Congressional inaction and the U.S. Treasury’s laggardly response to rising debt costs.

At long last it looks like the Treasury has begun putting its debt-shift plan to work. The share of debt that is sold under longer maturities is increasing.

On March 25th, the Treasury sold $66 billion in 2-year notes, up from $42-46 billion last spring and summer. This debt volume was also 11.3% higher than the batch of 2-year debt it replaced. A day later, the Treasury sold $67 billion worth of 5-year notes, which is $20-24 billion higher than the debt sold under this maturity 6-9 months ago.

This batch of 5-year debt was 63% bigger than the batch that matured and this sale therefore replaced.

The March 12th auction of 10-year Treasury notes brought in $39 billion, some $7 billion above the smallest auctions last year.

Meanwhile, the debt volumes sold weekly under short maturities are falling, though not by any dramatic numbers. The most recent 4-week bill auction sold $85.1 billion, which is 11% less than the volume sold a month earlier; the auctioned volume of 8-week bills is down 6%, and the 13-week bill is down 5.3%.

At the same time, there is not yet any reduction in the debt sold under the 17- or 26-week bills. Furthermore, the reductions in 4-, 8-, and 13-week bill auctions are barely visible in a longer 6-month perspective. It is therefore hard to draw any conclusions as to how far the Treasury has come in shifting its debt issuance toward longer maturities.

Time is not on the side of the Treasury. They promised to have the shift implemented by the end of April, which means only 4-5 more auctions for the short maturities that are sold weekly. For the longer, monthly-auctioned maturities, they only have one auction left to put their debt-shift strategy in full gear.

Congress is bringing nothing of substance to the efforts to fend off a U.S. fiscal crisis. The good news is that the pressure is building on them to take some kind of action. The bad news is that the debate over what to do is increasingly centered on the appointment of a bipartisan fiscal commission. Its duty would, simply, be to come up with fiscal reforms that would lower the budget deficit.

One of the most recent contributions to the conversation about a fiscal commission comes from the Los Angeles Times. On March 23rd, they explained that corporate CEOs regard the “burgeoning U.S. national debt and deficits” as “the geopolitical risk” of greatest concern. Citing Lori Esposito Murray of the Conference Board’s Committee for Economic Development, the L.A. Times adds that “a Bipartisan Congressional Commission on Fiscal Responsibility” would be instrumental in reducing the federal government’s debt.

It is worth noting that Murray has a background to the left of the center in American politics. This means that the idea of a fiscal commission is gaining bipartisan support. The same idea has been propagated for the better part of a year by the Cato Institute, a libertarian think tank. This may seem like the beginning of a victory for bipartisanship, but so far, no proponent of the commission has explained how the Left and the Right are going to agree on the directives for a commission.

According to the L.A. Times article, Murray wants the commission to “address the biggest drivers of deficits”, namely “Medicare and Social Security”. These two entitlement programs—which provide health insurance and pension benefits for retirees—are the biggest structural contributors to the deficit, which makes it natural to target them for reforms.

So far, we can assume that the Cato Institute would agree. But what about taxes? Here is what Lori Esposito Murray said to the L.A. Times:

To address the revenue challenge, the Commission should undertake comprehensive tax reform based on the principles of fairness, efficiency and simplicity

If we assume that by fairness, Murray means that corporations and wealthier individuals should pay more in taxes, it will be interesting to hear how the Cato Institute agrees with Murray on this point.

The plain truth is that a fiscal commission cannot succeed. It will only serve as a vehicle for Congress to punt on an issue that requires urgent action.

So far, the Treasury has been able to interact with the market for U.S. debt and avert a fiscal crisis. However, that ability can only buy Congress a little bit more time; if that time is not used wisely, then the disaster known as a fiscal crisis is still awaiting us in the near future.