When the Standard & Poor’s credit rating agency downgraded the French government last week, it made quite a splash in the media.

With a touch of smugness, Al Arabiya commented that the downgrade was “a blow to Emmanuel Macron’s government days before EU parliamentary elections.” Russian news and commentary outlet TopWar.ru struck a similar tone in their comment: they highlighted that S&P analysts do not expect the French government’s budget deficit to fall below 3% of GDP before 2027.

In a longer commentary, Reuters elaborated:

After raising its estimates in April, the government now expects to cut its public sector budget deficit from 5.1% of economic output this year to 4.1% next year, with aim of reducing the fiscal shortfall to an EU ceiling of 3% by 2027.

The Gateway Pundit bombastically called the downgrade “a brutal wakeup call” for President Macron, while French newspaper LeMonde took a less dramatic approach:

After months of suspense, the American rating agency Standard & Poor’s downgraded the rating that assesses the quality of French debt on the evening of Friday, May 31, 18 months after issuing its first warning

They also noted that this was “the second time in just over a year” for France: in April last year Fitch lowered its rating of the French government’s credit status.

In my analysis of that downgrade, I said:

The question is how the French government responds to this downgrade. If it responds responsibly, it can turn this negative experience into a fiscal turning point … If, on the other hand, [President] Macron and [then-Prime Minister] Borne decide that Fitch’s analysts are wrong … then their country will inevitably be hurled into a downward spiral of credit downgrades, skyrocketing interest rates, and galloping budget deficits.

With the S&P downgrade, France has taken one more step in this direction, and there is not much that suggests a reversal. On the contrary, we have good reasons to expect further downgrades in the future.

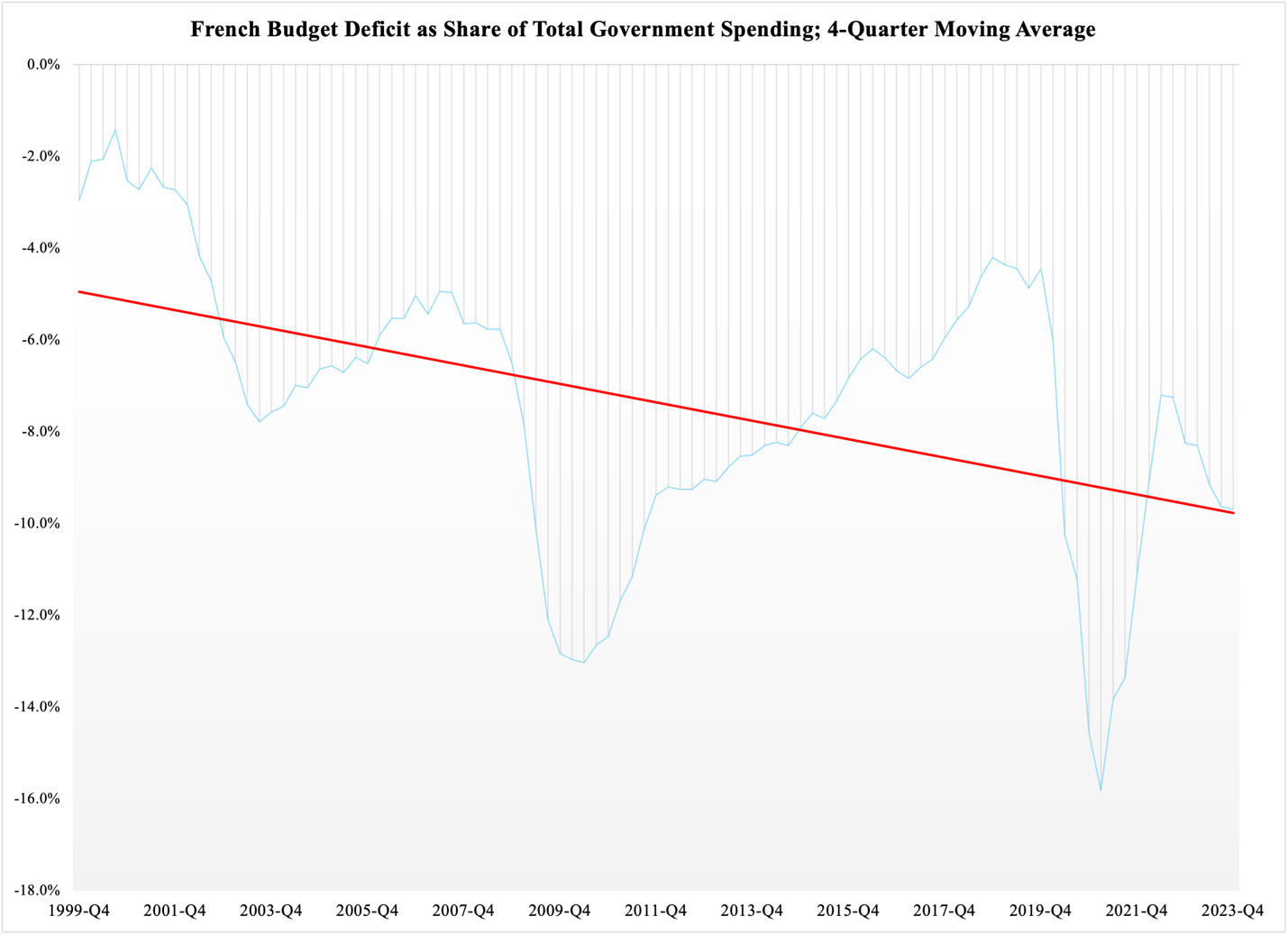

Part of the reason for this prediction is reported in Figure 1, namely that French public finances have been eroding for a long time. The deficit for the consolidated government, measured as a percentage of its total spending, has been through some violent swings in the past 25 years, but each trough has been followed by a weaker recovery:

Figure 1

This long-term deterioration of public finances is combined with one of Europe’s most confiscatory tax systems. In 2023, France imposed higher taxes on its businesses and households than any other EU member state except Finland. In fact, as reported in Table 1 below, the total burden of taxes on the French economy is 5.5 percentage points higher than the euro zone average, and a full six percentage points above the EU average:

Table 1

Government spending takes up an even bigger share of the economy, which has two consequences. First of all, when government sets up a spending program—be it for health care or education or any other item—it closes the free market in that sector of the economy. The free market is the final arbiter of whether or not economic resources are being used as efficiently as they could be used. By definition, government spends resources according to a centralized plan. This plan is defined by politically set goals, which means that the distribution and utilization of resources under government are also politically determined.

In short: the bigger the share of the economy that is spent by government, the lower the overall efficiency of the utilization of economic resources. As a direct consequence, economic growth declines; economic growth is generated when entrepreneurs produce more and better goods and services by using less resources—in other words, when they are more efficient. A bigger government means less overall efficiency, and less growth, in the economy as a whole.

The second consequence of a bigger government is higher taxes. Governments that spend big money always take more from their households and businesses in taxes than governments that spend less. This holds true even when some big-spending governments run large, endless budget deficits. High taxes distort economic activity, make it costlier to open, run, and grow a business, and they take a sizable toll on household finances.

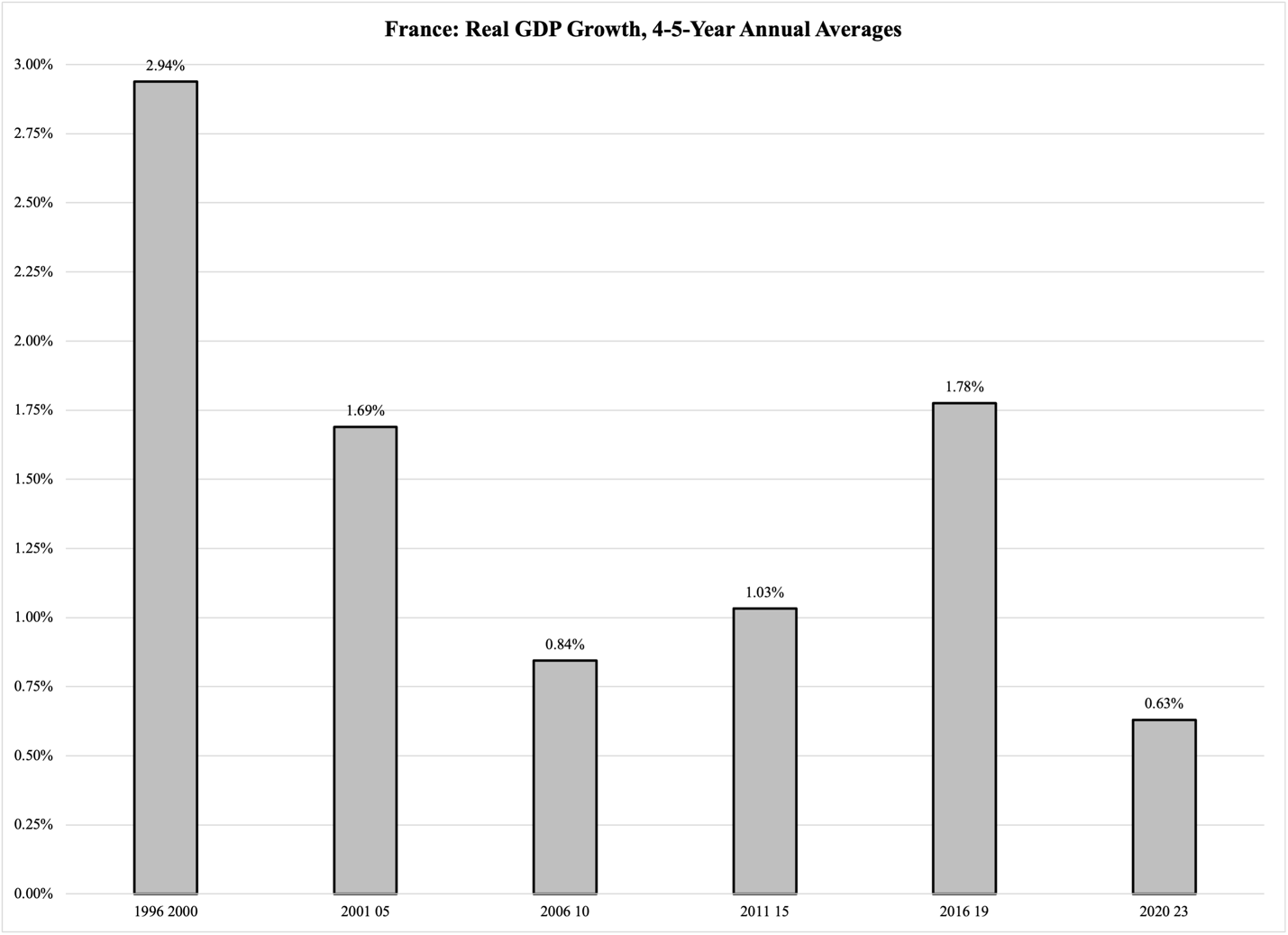

All in all, higher taxes, like big government’s efficiency losses, depress economic growth. As Figure 2 reports, France has a significant problem with low economic growth, and it is not new. We have to go back to the 1990s to find a period when the French economy sustained reasonably good annual growth rates:

Figure 2

It is worth noting in Figure 2 that the pandemic and its recovery, included in the period from 2020 through 2023, left the French economy virtually at a stand-still. Other economies have done better: of the EU’s 27 member states, four managed to grow more than 4% per year, and another six produced annual growth rates in the 2-4% range.

The French government’s budget problems originate in an irresponsible ambition to sprawl government in all directions. As a telling example, France is one of only five EU countries where government spends more than 40% of its money on social protection benefits. This shows a high ambition to redistribute income, consumption, and wealth among its citizenry; economic redistribution is directly antithetical to economic growth.

Since it stifles economic growth, it also stifles the growth in tax revenue that is necessary for a government to continue to fund its ambitious programs for economic redistribution.

Unless the bright minds in Paris abandon their redistributive ambitions and set a new course for their government, they will continue to suppress both economic growth and their own tax revenue. This paves the road for future budget deficits—and future credit downgrades.