On June 21st, under a drastic headline, Fortune Magazine dramatically declared that Sweden has gone from a peaceful society to a haven for criminals as a result of the country transitioning from cash to an almost all-electronic payments system. The reason, Fortune declares, is that criminals—often affiliated with gangs or crime-family-like structures—have learned how to con people out of money when they use an electronic citizen identification system known as BankID to make payments.

The whole transition from cash to electronic payments is fascinating. It is being discussed globally, sometimes with reference to more or less conspiratorial theories about a looming worldwide ban on cash for population control purposes.

I am not interested in those theories—my curiosity steers me toward investigating the idea that electronic payments can somehow successfully replace cash. But before I delve into that issue, let me point out that contrary to what Fortune Magazine suggests, it was not the transition from cash to cashless transactions that made Sweden a haven for organized crime. My native country has been slipping into the hands of criminals for much longer than the politicians and corporate executives have tried to eliminate cash. One reason why merchants (as visitors to Sweden have experienced) have shied away from accepting cash payments is—the very real risk of robbery which, again, was high long before the cashless transition began.

As for the transaction from cash to cashless, a conceptual note is in place. We usually associate cash with ‘money’ and think of it almost as two sides of the same coin. However, the concept of money is much more complicated than that. In fact, there is an entire branch of economics devoted to money.

Making a career as a monetary economist is not only fun, but it can be lucrative if you lean toward the empirical end of it. Many monetary economists get into central banking; others end up working in commercial banking or the financial industry.

It may seem strange that economists have an entire sub-branch of their discipline devoted to money—after all, we all know what money is, right? In an everyday sense of the term, that is definitely true, but money is so much more than what we use when we pay our bills or buy something at the local supermarket.

The best way to understand money is to replace the term with ‘liquidity.’ The reason why the Swedish cashless experiment did not stop criminal activity is that the system simply replaced one form of liquidity with another.

Traditionally, cash is understood as the highest form of liquidity; coins have been used for as long as man has traded with man. Bills became cash gradually during the golden era of the Italian city-states when the banking system evolved to almost modern levels of sophistication. One of the innovations was a paper certificate of the deposits you had made with a bank. With a judicial system strong enough to secure the safety of such certificates, those documents became trusted evidence of bank deposits.

Over time, as trade grew in volume and value, merchants began using shortcuts to make payment systems more efficient. If Jack wanted to buy a large quantity of merchandise from Joe, he would show his certificate to Jack as evidence that he had the money. Then he would go to his bank, make a withdrawal, and pay Joe in cash. However, sometimes the circumstances of trade could put a considerable amount of time between the trade agreement and payment; in order to speed up trade and make life easier for all, merchants began using the deposit certificates from their banks as a means of payment.

In other words, instead of going to the bank to get the cash, Jack would simply sign over his deposits to Joe. If he wanted to sign over a smaller share than his full deposit, he could write a separate note of transfer.

This is how the bills of cash and the modern check system evolved. Over time, the deposit certificates were standardized; you went to your bank with your deposits, and they handed you deposit certificates of different values, with a total value equal to your deposit. These certificates were standardized and unique to every commercial bank.

Later on, as central banks emerged, they took it upon themselves to centralize and standardize the bills. Which—long story short—led to the cash we have today.

It is important to understand this background to the money of our time. Every society that wants to evolve beyond primitive barter will need some form of cash. The same is true for an advanced economy that wants to stop using bills and coins, but what do you replace them with and still preserve the maximum degree of liquidity that cash has?

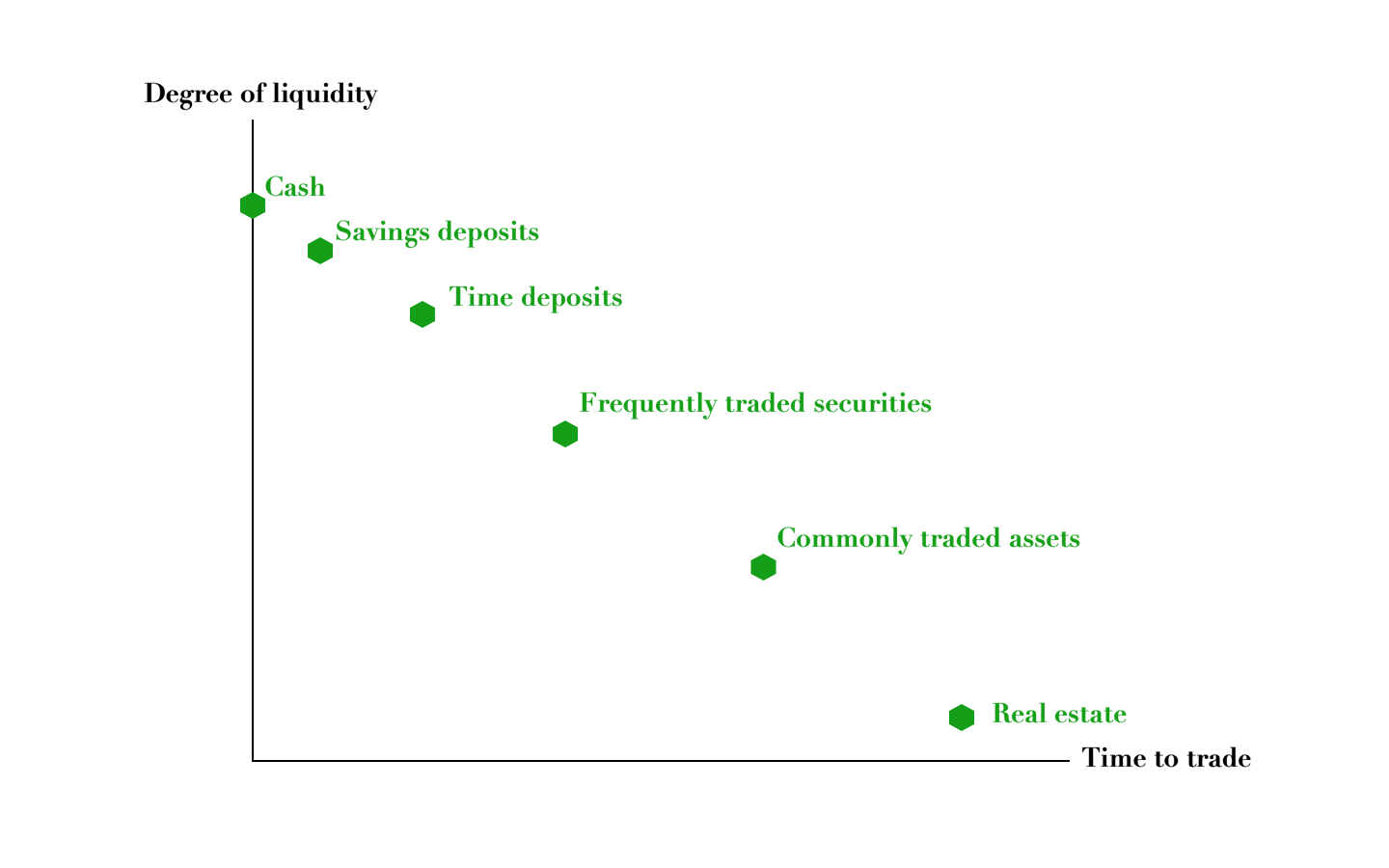

To see what the Swedes did, let us first take a look at Figure 1a, which ties the degree of liquidity of an asset to its tradability, i.e., how easily we can exchange it for something else. The higher we go on the vertical axis, the more liquid an asset is; the further out we go on the horizontal axis, the more time it takes to convert an asset to liquidity—in short, use it as a means of payment.

Cash has the highest degree of liquidity. With modern debit cards, we count deposits linked to such cards as being equally liquid. Savings deposits are typically a bit less liquid: you have to go into the bank and move the money from that account to a checking account, or withdraw cash, before you can use it for payments.

Real estate is among the least liquid assets we can have:

Figure 1a

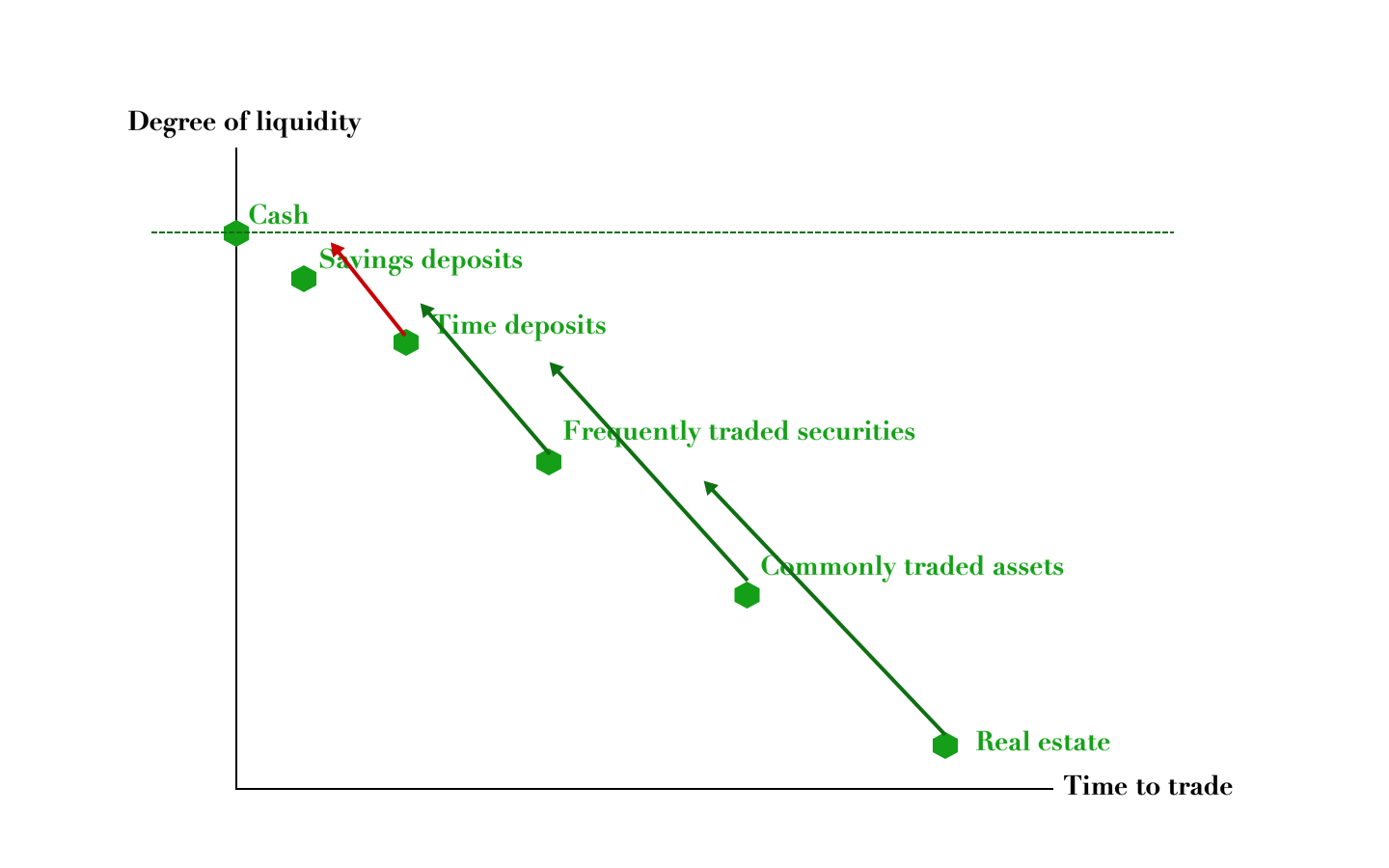

When Sweden tried to eradicate cash, the country needed a replacement. Their choice fell to checking deposits linked to a high-grade electronic identity, or BankID. Initially, these deposits were not nearly as useful as cash, in part because the security process needed to verify the transaction. This placed the BankID-linked deposits at a lower level of liquidity, comparable to traditional bank time deposits.

Over time, though, the Swedish banking industry worked up the system to become virtually equivalent to cash; see the red arrow in Figure 1b below:

Figure 1b

Generally, our economy has evolved in the direction of raising the liquidity level of more and more assets. For an intriguing analysis of this phenomenon, see Okun, A: Prices and Quantities (Brookings 1981). Frequently traded assets, such as stocks, could in the past only be traded through a rigorous system where paper shareholder certificates were exchanged for cash; today, it is easy to trade stocks through electronic instant-trade systems.

Commonly traded assets like cars can now be sold online, but they can also be used for liquidity by means of, e.g., title loans. They will never reach the same liquidity level as cash, of course, but the trend in the financial industry has been toward developing new products that shorten the gap between, in this case, car ownership and drawing liquidity from that same ownership.

Real estate is perhaps the most striking asset form where the distance between ownership and liquidity has shrunk. There are credit-based bank products that essentially allow homeowners to use their property as a source of cash on demand.

As a long-term trend in economic evolution, this increased level of liquidity in all forms of assets is of very positive value. It lowers transaction costs, allows for more flexible financial planning, and encourages further innovation in, e.g., the retail industry. However, it also comes with higher risk, as we can learn from the Swedish example: since the point of raising the level of liquidity is to give an asset properties that—as far as possible—match the liquidity of cash, the trade in that asset must also to a large degree mimic cash in anonymity. As a result, crime migrates from cash to electronic payments.

Although electronic transactions can always be monitored and registered, the highest possible level of liquidity—and tradability—of an asset also means downgrading security standards. The Forbes article points to this in the Swedish example. When security standards were lowered for the sake of transaction smoothness, criminals saw an opportunity to steal electronic cash with relative ease.

I doubt that the Swedish cashless future experiment will survive. The Riksbank—the central bank of Sweden—has on a few occasions recently declared that cash is an important asset in times of economic or social crisis. Furthermore, as criminals continue to dig into the potential behind BankID-related fraud, people will come to realize that it comes with greater risks of theft than cash does. If someone steals the $80 I have in my pocket, they get their hands on $80. If, on the other hand, a thief can get access to my BankID-linked bank deposits, he can steal whatever is in my bank account.