As was widely predicted, the European Central Bank on Thursday, June 6th, lowered its policy-setting interest rates:

The Governing Council decided to lower the three key ECB interest rates by 25 basis points. Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be decreased to 4.25%, 4.50% and 3.75% respectively

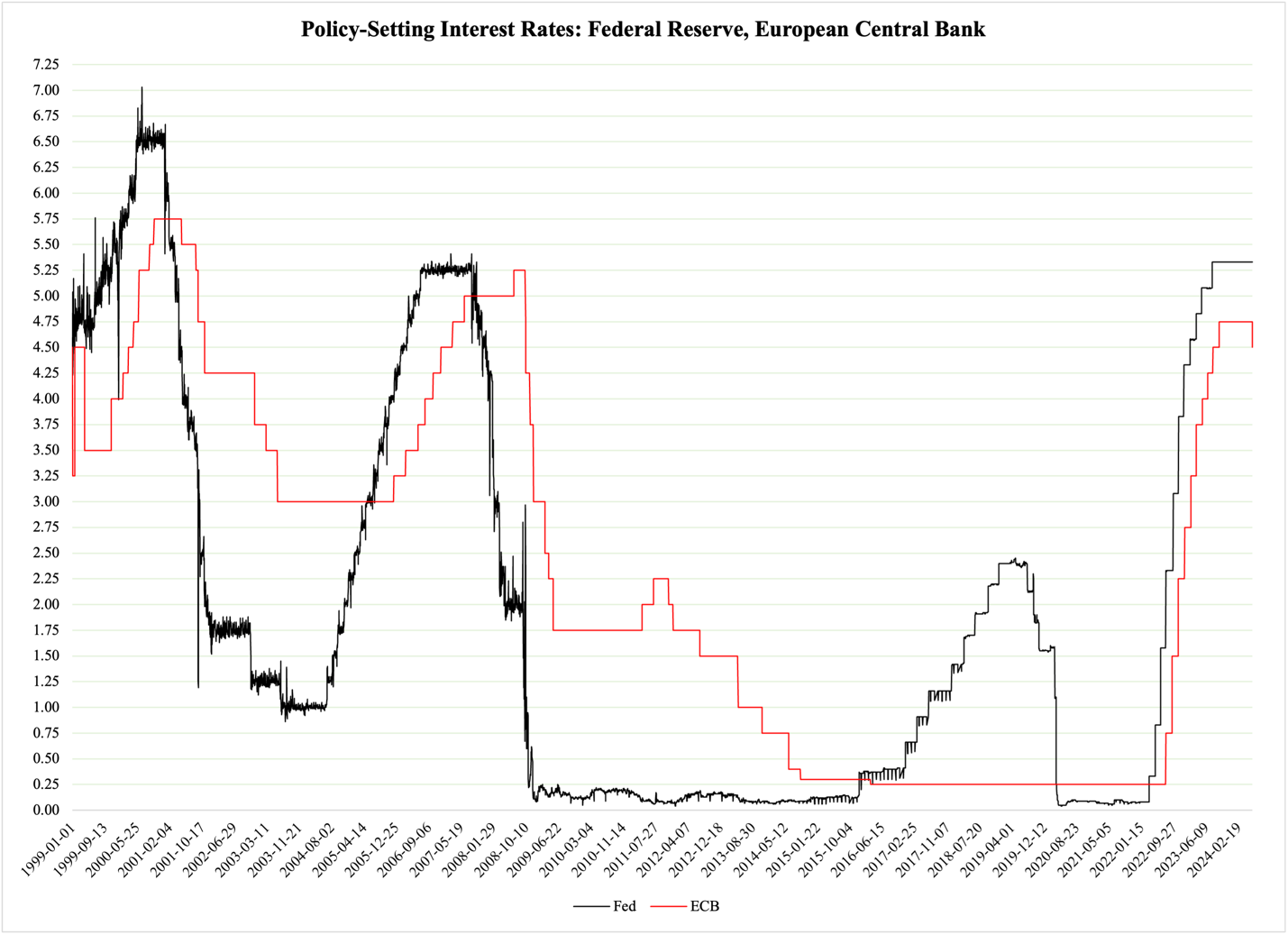

This was not a wise move by the ECB. Normally, as Figure 1 shows, they follow in the footsteps of the Federal Reserve, letting their policy-setting triad of interest rates (red function) shadow the Fed’s funds rate (black):

Figure 1

During the economic recession of 2008-2010, the ECB was slower to run interest rates down toward zero than the Federal Reserve was. Once they got there, though, they stayed put until just after the Fed began raising its rate in 2022. Since mid-2023, the two central banks have remained synchronized and refused rate cuts—until June 6th when the ECB took the lead.

As I explained the other day, I do not expect the Federal Reserve to follow suit, but rather to keep their federal funds rate unchanged for the remainder of this year. Only a weakening of the business cycle can change that.

This means that the ECB will have to live with a larger interest rate discrepancy between the euro zone and the U.S. economy. In today’s macroeconomic environment, this has more downsides than upsides, and there are signs that the policymakers at the ECB know that they did not make the best of decisions here. They gave an ambivalent motivation for their decision; on the one hand, the trend of lower inflation is reliable:

Based on an updated assessment of the inflation outlook, the dynamics of the underlying inflation and the strength of monetary policy transmission, it is now appropriate to moderate the degree of monetary policy restriction after nine months of holding rates steady.

On the other hand, it is not:

At the same time, despite the progress over recent quarters, domestic price pressures remain strong as wage growth is elevated, and inflation is likely to stay above target well into next year.

Not only do they predict inflation “above target,” but they also predict very slow economic growth:

In view of this forecast, and of the ECB’s repeatedly stated goal to “ensure that inflation returns to its 2% medium-term target,” the decision to lower interest rates comes across as irresponsible, even a bit careless. The main reason is the combination of very slow GDP growth and still-elevated inflation: an economy that cannot even produce 1% real growth, yet operates with an inflation rate of 2.5%, is an economy that does not need any stimulus from the central bank.

From the ECB’s perspective, one could argue (although they don’t) that the rate cut will facilitate supply-side expansion. A lower interest rate would improve credit supply for smaller businesses that lack the internal financing functions that big corporations have. However, in order for a supply-side expansion to follow a cut in a central bank’s interest rate, the rate must—so to speak—be scaled to the rate of economic growth.

In plain English, this means that the weaker the growth rate in GDP, the bigger the rate cut must be to stimulate the supply side. A 0.25 percentage point reduction is at best going to have a marginal effect on the supply side. Businesses do not invest primarily based on the interest rate of available credit, but on the prospect of revenue from the investment in question. With slow growth to begin with, a small rate cut will not improve the equation in favor of more investments, especially not from small businesses.

The effect will likely be bigger on the demand side—and now we are getting to the main reason why this is an irresponsible rate cut. If this rate cut works its way into lower rates on credit card debt and other forms of consumer credit, there is a fair chance that some euro zone member states will see something of an economic stimulus. Banks, eager to make more money in an economy that is essentially standing still, could very well jump on the opportunity offered by slightly lower interest rates and offer their customers access to cheaper credit.

A debt-driven increase in consumer spending in the second half of 2024 would make a moderate addition of economic activity to the euro zone economy. Since it is debt-driven—as opposed to being the result of higher wages—it does not emanate from the production of more economic value. For this reason, it is a bit more inflationary in nature than a ‘value based’ increase in economic activity.

This does not mean that the euro zone will see higher inflation as a result of this rate cut. For that to happen, the ECB would have had to make a much bigger cut. However, this rate cut will likely slow down or even cancel the expected decline in inflation for the remainder of the year.

To what extent it is strong enough to keep inflation elevated into 2025 is too early to tell. To determine this, we would need to know more about what effect this rate cut will have on government spending. As I have repeatedly pointed out, Europe is littered with governments running hopeless budget deficits; it is almost like 2007 all over again, when Europe stood on the precipice of a major public finance crisis.

Today’s budget deficits are now going to be funded on slightly cheaper terms; the rate cut allows governments across the euro zone to sell sovereign debt at lower yields. I expect the rate cut to be strong enough for sovereign debt markets to offer deficit-plagued governments noticeably lower debt costs. This, in turn, will motivate most, if not all of them, to borrow more money.

In other words, we will probably see a bigger fiscal stimulus in the euro zone over the next 12 months than would otherwise have been the case. In some countries, it could conspire with a moderate increase in debt-driven consumer spending and cause a small uptick in inflation.

None of these effects will be substantial, but they will—again—be noticeable, especially in countries prone to higher inflation.