This is the last of three installments on the incomprehensible proposal from Donald Trump’s presidential campaign to end the independence of the Federal Reserve.

As I explained in Part II, there is only one reason why any president would want to have full control over his country’s central bank: it allows him to cover his government’s budget deficits with newly printed money.

As fellow economist Robert Gmeiner and I explained recently, printing money to pay for budget deficits is the fastest and most destabilizing way a government can cause hyperinflation. As I will show in a moment, if the Trump campaign got what it wanted here, the result would be inflation numbers so astronomical that it would mean suicide for the American economy.

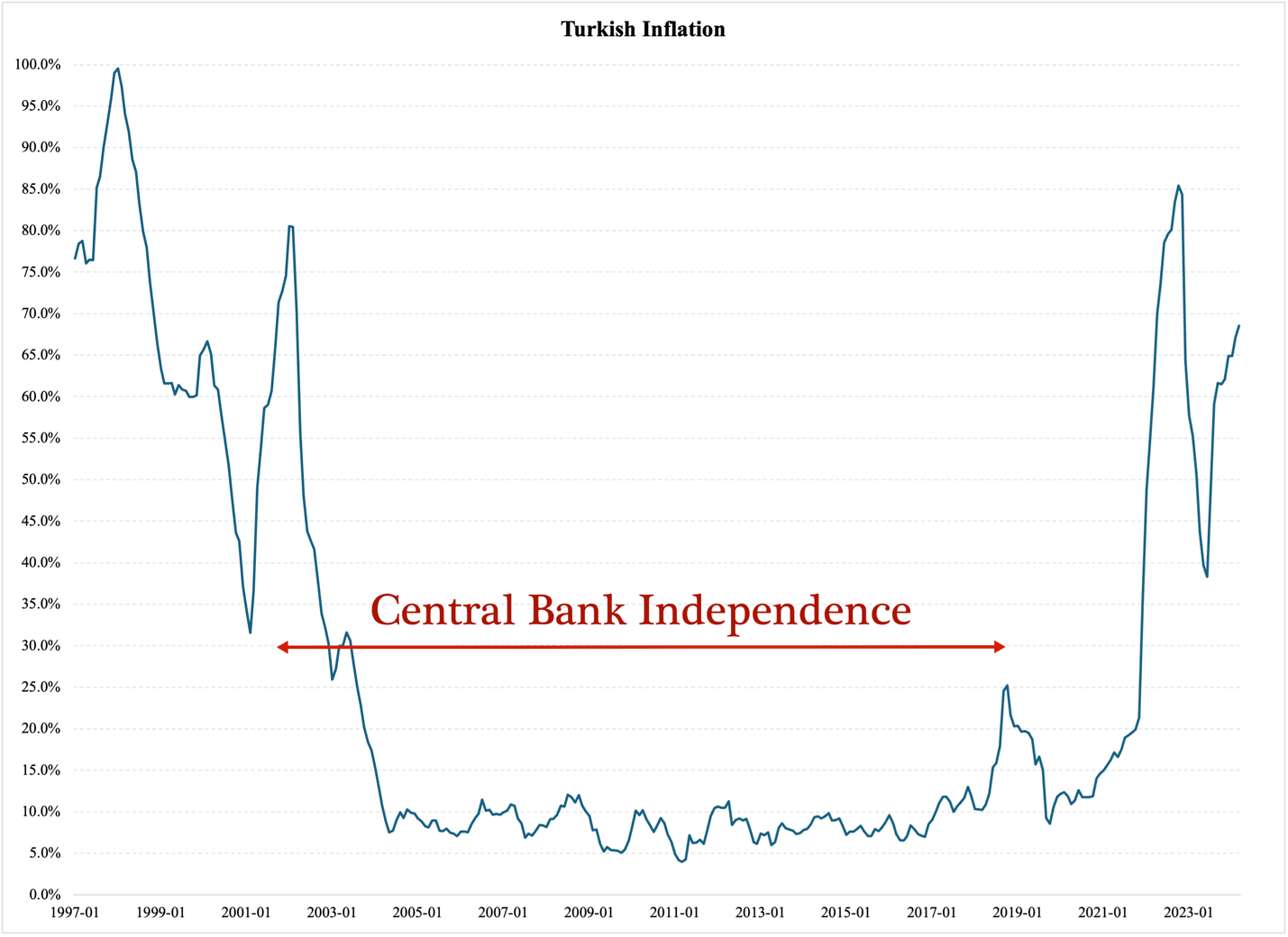

Hopefully, we will not have to argue this point based solely on scholarly research; there is an apparent, recent example of why a central bank must remain independent. Before 2001, the central bank in Turkey operated at the mercy of the executive branch of government. Starting in 2001, the central bank operated as an independent monetary institution; in recent years, though, President Erdogan has de facto ended its independence and forced it to operate at the mercy of his administration.

We can see the result with frightful clarity in Turkey’s inflation numbers:

Figure 1

In the years 1997-2000, the average annual inflation rate was 71%. During the central bank’s independence period—defined as starting in 2001 and ending in 2019—inflation averaged 15%. This is undoubtedly a high number, but there were long periods where inflation stayed consistently below 10%.

Once President Erdogan decided that he was better at running the central bank than its central bankers, inflation shot up again. Since 2020, Turkey has been plagued by high and volatile inflation: since 2020, while swinging between 38% and 85%, it has averaged 41% per year.

There are other examples to look at, including Venezuela where inflation reached an unfathomable 10 million percent a few years ago. However, using such examples in the context of a proposal for reforms to the Federal Reserve would be unproductive; inflation rates at such phantasmagorical levels eventually lose their analytical as well as persuasive meaning.

This is not the case with the Turkish example. It has a lot more merit in an analysis of Trump’s Fed reform idea than may at first seem to be the case. If he got his way, we could indeed see Turkish-level inflation rates here in America—and worse.

Yes—I have the numbers to prove it. But before I report them, let us make clear that this proposal for ending the Federal Reserve’s independence is not just a harebrained concoction by free-wheeling campaign advisors; if Trump convinced someone in Congress to write a bill on it, there is a possible path for it at least through the House of Representatives.

There are two reasons for this, the first being Speaker Johnson’s new, cozy relationship with the Democrat minority in the House. After the recent divisions within the Republican caucus, the Speaker has made many new friends across the aisle. They will be more than happy to work with him again in the future.

Which brings us to the second reason why a proposal for ending the Fed’s independence could get majority support. Some 20 years ago, a new ‘economic theory’ emerged under the acronym MMT. It was developed by a group of economists at the University of Missouri, Kansas City, and is short for ‘Modern Monetary Theory.’ It is little more than a call for ending the independence of the Federal Reserve and the monetized abolishment of government debt.

Among the founding contributors to MMT, we find Stephanie Kelton, with a long career as an economist with the Democrat party. Among her accomplishments, Kelton counts advising Senator Bernie Sanders on the virtues of MMT. Although there are more sensible Democrats who reject this ‘theory,’ including reputable economist Larry Summers, the MMT ideas have set down deep and increasingly influential roots on the Left in American politics.

Suppose Trump gets re-elected in November. Suppose also that the House narrowly remains in Republican hands and Mike Johnson continues as Speaker. With the Democrat party veering increasingly to the left, radical ideas like MMT gradually become more mainstream. Imagine then a growing pro-MMT caucus among the Democrats being paired up with Trump-loyal Republicans who adopt his idea for ending the Federal Reserve’s independence.

Could it pass the House? I would not bet against it. The Senate is unlikely to get onboard—but only unlikely. In politics, he wins who is the better deal maker. If enough senators get something from the president that is more important to them than saving the independence of the Federal Reserve, then a reform idea like this could make it to the president for his signature.

If this happened, it would mean economic suicide for America. There is no other way to explain the consequences.

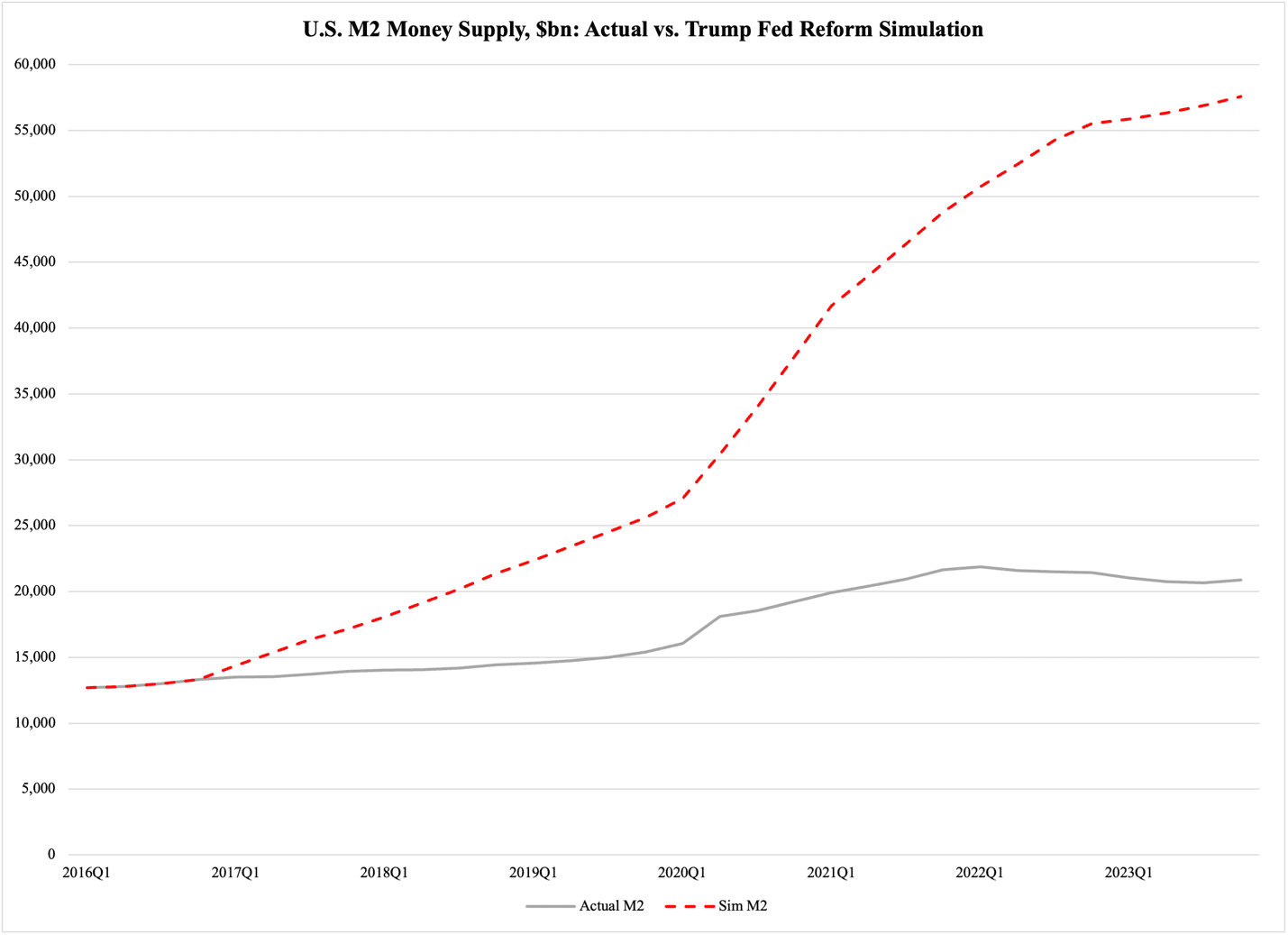

When I first heard about this idea, I decided to do a little experiment, based on the premise that Trump had gotten his Fed reform idea passed into law immediately when he became president in January 2017. Using data from the U.S. Treasury on the federal debt, and from the Federal Reserve on money supply and the central bank’s holdings of U.S. Treasury securities, I made the following assumptions:

The result, reported in Figure 2, is a bona fide macroeconomic horror show. The gray line shows the evolution of the actual stock of M2 money supply; the dashed red line shows how it evolves under my simulation:

Figure 2

At the height of the pandemic, the actual M2 money supply reached $21,861 billion. Under my Fed reform simulation, it would have been 132% bigger at $50,733 billion. From there, the gap would continue to expand until in the last quarter of 2023 the simulated M2 money supply would exceed $57,500 billion. Or $57.5 trillion.

That would be 176% more than the money supply we currently have in the U.S. economy.

What kind of inflation would this trigger? I almost dare not find out. As I referenced earlier, I studied this very question together with Robert Gmeiner. In lieu of an elaborate, model-based simulation, there are two points from our article that indicate how inflation would rise under my Fed reform simulation.

First, the correlation between deficit monetization and inflation is very strong—almost perfect—which means that there is no more capable source of high inflation in the economy than consistent deficit monetization. The more money we throw into monetizing deficits, the more certain is the inflationary outcome.

Secondly, once deficit monetization begins on a large scale, it is nearly impossible to end. On the contrary, given the nature of the entitlement programs that are funded with printed money, monetization demands its own perpetuity. This happens when inflation begins to take off, people lose their jobs or fall under eligibility limits due to the destructive effects of inflation, and the need for monetized deficit spending multiplies through the federal government’s COLA (Cost of Living Adjustments) formula and other eligibility criteria.

Long story short: monetary inflation is inherently unstable. Unless the central bank reverses course very quickly—as the Fed did in 2022—monetary inflation proliferates very quickly through the economy. Like pouring ketchup out of a glass bottle, once it gains momentum there is no stopping it.

Therefore, we cannot simply and proportionately scale up the inflation that we saw in the past couple of years. Just because the actual M2 money supply increased by 36% from 2020 to 2022 and caused 9% inflation, we cannot simply assume that a 72% increase in money supply would cause 18% inflation. Nor can we simply conclude that the 87.4% increase in M2, which my Fed reform simulation shows for that period, would lead to 21.5-22% inflation.

A much more realistic approach is to think of monetary inflation as not increasing steadily, but accelerating. Therefore:

Needless to say, this level of inflation would irrevocably destroy the U.S. economy. Yes, it is the result of an experiment and could therefore be dismissed as purely hypothetical, but consider what even one-tenth of this inflation rate would do to America.

To conclude: I urge Donald Trump, from the very bottom of my professional experience as a Ph.D. political economist, to please come out in force and pledge that if you are elected president again, you will wholeheartedly respect the independence of the Federal Reserve.