There is trouble brewing in the market for U.S. government debt. While the Federal Reserve signals that it is at, or near, the end of its interest-rate increases, there is no end in sight to the budget deficits that Congress runs. On the contrary, they are now on track to borrow $2 trillion for this fiscal year.

It is no surprise that the market for U.S. government debt is trending interest rates upward toward 6%. A big part of the reason for this is that investors are worried about the ability of the federal government to honor its debt obligations in the future. However, the government is fueling these worries by sticking to a debt-management policy that actually drives interest rates higher.

Currently, the U.S. government debt is rising at a pace of almost $600 billion per month. This is not a number that will hold up over the longer term: a more ‘normal’ pace would be less than $200 billion per month. The currently higher number is part of an incorporation of the unofficial borrowing that took place during the months earlier this year when the federal government’s self-imposed debt ceiling prevented it from officially borrowing more money.

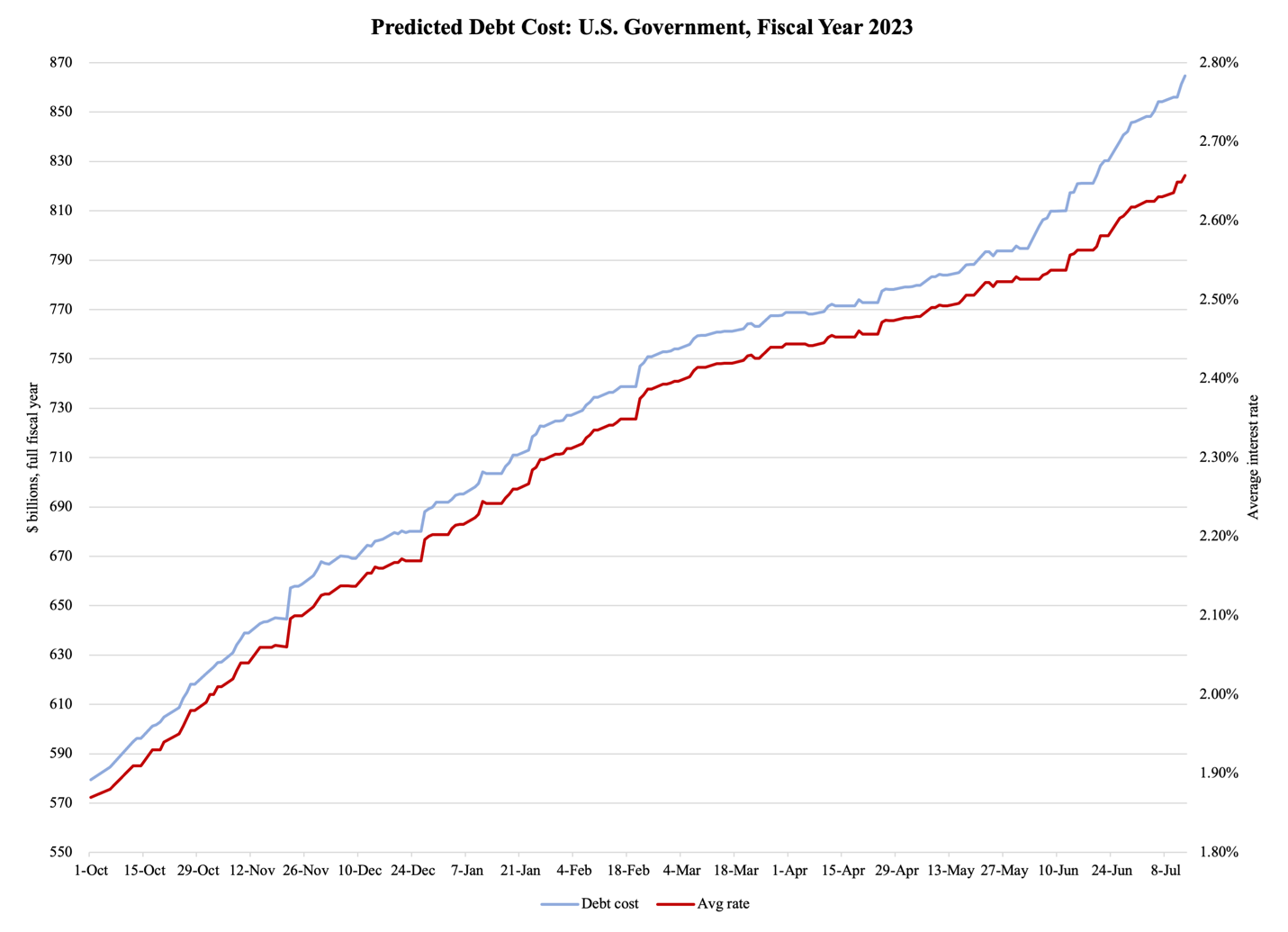

Once the official debt ceiling was removed on June 5th, the federal debt jumped by $358 billion. A month later, the debt was $935 billion higher than the last day under the debt ceiling. Meanwhile, as Figure 1 below reports, the average interest on the debt has been climbing, showing investor doubt in the ability of the federal government to continue to pay its creditors as promised.

Plain and simple: investors have good reasons to wonder just how high the pile of debt will be going forward. The more they wonder, the higher the interest rates will be—exactly as we are seeing happening.

Congress on their end does absolutely nothing to put those worries to rest. As of July 13th, the U.S. government’s debt stood at $32.5 trillion. That is $1.6 trillion more than the debt was on October 1st last year, the start of the 2023 fiscal year. There are two and a half months left in this fiscal year.

To be fair, there are some mitigating circumstances to report. As mentioned, the current rate of increase in debt is $600 billion per month, but the long-term rate is markedly lower. So far during this fiscal year Congress has borrowed $155 billion per month. At this pace, they will add another $467 billion to the current debt before this fiscal year ends on September 30th. While the borrowing pace is likely to slow down a bit in the coming months, we see no signs of that yet; in the first two weeks of July, the U.S. Treasury increased its debt by $210 billion.

This means that unless a miracle happens, Congress will break another borrowing record at the end of September. It will be the first year of normal economic activity—the pandemic years of 2020 and 2021 were exceptional—when they borrow $2 trillion. This gigantic deficit looms heavily over the debt market.

It is also having a tangible effect on interest rates, which continue to rise. The current estimated average rate on the U.S. debt is 2.66%, up from 1.87% at the start of the 2023 fiscal year. This means that America’s taxpayers are going to have to fork over quite a bit more money in the next 12 months just to keep their government creditors happy.

Since Congress is paralyzed on this issue, it is now up to the sovereign-debt market to decide the fate of the federal government’s credit status—and by extension, the fate of the U.S. economy. As things are now, Congress and President Biden are glacially moving the federal government into a position where its debt overwhelms not only its own budget but the U.S. economy as a whole. At some point—one which is notoriously difficult to predict in time—the sovereign-debt market will decide that it has lost enough confidence in U.S. debt.

At that point, the glacial slide into a fiscal crisis turns into a freefall.

One of the indicators of that breaking point is the average cost of the U.S. debt. As mentioned, that rate is currently 2.66%. This may not sound like much, given that interest rates at Treasury auctions and on the secondary market for U.S. debt often exceed 5%. However, the average rate on the debt is based on the total stock of debt, which includes both newly issued Treasury securities and those that are years, even decades old. To take one example: of the total $32.5 trillion in federal government debt, $2.1 trillion is issued under the Treasury note with a 3-year maturity. The oldest batches under this maturity, issued in the latter half of 2020, pay their owners less than 0.2% per year. By contrast, the batch that was sold last month pays 4.475% per year.

When these batches mature, the Treasury does not simply pay back the money to its creditors (that would be a net reduction of the debt). They borrow new money to fund the repayments. That money, in turn, is borrowed at the rates that investors currently demand.

This so-called debt rollover is a major reason why the cost of the debt continues to rise. The increase in the average rate on the debt since October 1st last year, together with the growth in the debt itself, translates into a substantial increase in the predicted, annualized cost of the debt. As Figure 1 reports, it has risen from $579 at the beginning of the fiscal year to $865 billion today:

Figure 1

Source of raw data: U.S. Treasury. Based on fiscal forecasting model by Futura Forecasting

The predicted annualized cost is not the actual cost of the debt over the entire fiscal year. That cost consists of payments made every month, added up over the 12-month period. Since the average rate rises over the year, this sum total will be lower than the annualized cost at the end of the year.

However, the evolution of the annualized cost is a good tracker of the debt cost as it evolves over time; if the cost rises linearly through the fiscal year, its six-month midpoint will be a good estimate of the total actual cost for that year. Estimated this way, by September 30th, Congress will have doled out $765-770 billion in interest on its debt for the whole fiscal year.

As Figure 1 reports, the cost of the debt rose linearly last fall and then slowed down in the first few months of this year, when the federal government hit its own debt ceiling. The acceleration of the cost after the debt-ceiling suspension at the end of May suggests that a linear estimate is not a bad bet after all; unless something radical happens between now and September 30th, the actual debt cost is going to be close to $800 billion.

This is a rise of approximately one-third over 2022. However, we have to keep in mind that the $800 billion figure is based on the assumption that nothing radical happens throughout the remainder of the 2023 fiscal year, i.e., up to September 30th. This is where we have reasons to worry: interest rates on the debt continue to creep upward, with no end in sight. Tables 1a and 1b report the yields at the last four auctions of Treasury bills (1a, auctioned weekly) and of Treasury notes and bonds (1b, auctioned monthly):

Table 1a

Table 1b

Source: U.S. Treasury

We can expect investors to continue to demand higher yields in order to come back and buy more of its debt: the yields in the secondary market are almost all higher than the auction yields. Since the secondary market trades all U.S. securities of all maturities daily, it sends a stronger signal than the auctions do of where investors want the yields to go.

The upward trend is particularly noticeable in shorter-term debt. This should really worry the U.S. Treasury, and by extension the president, Congress, and all of us U.S. taxpayers. The reason is in the composition of the debt: since October, the Treasury has increased the share of the debt that matures in one year or less, from 15% to 19%.

In dollars and cents, since October last year, the Treasury has sold $1,687.6 billion in new debt under maturities of one year or less. They have sold this debt to fund an increase in the total debt of $1,613.4 billion.

These two numbers together are sensational. The U.S. Treasury has not only funded the entire increase in the debt with the most expensive form of debt—that which matures quickly—but they have also replaced some cheaper, longer-term debt with these costliest of debt instruments.

This is a baffling debt management strategy. A simulation of an alternative strategy, where all the new debt is issued in the 2-10 years maturity spectrum, would have lowered the debt cost by at least $80 billion for the whole fiscal year. This estimate assumes that interest rates would not have been affected by an extra $1.6 trillion of new debt being sold under the longer maturities. We can reasonably make this assumption: at the start of the 2023 fiscal year, the debt under the 2-10 year maturities, a.k.a., Treasury notes, was 4.5 times larger than the debt under short maturities, i.e., Treasury bills.

In other words, the debt market could more easily have absorbed the significant debt increase if it were directed toward the ‘notes’ segment instead of the ‘bills’ segment.

One consequence of the Treasury’s crazy debt strategy is that the yield curve on U.S. debt is inverted. This means, plain and simple, that investors make more money on buying short-term debt than long-term debt; the flip side of that coin is a higher cost to taxpayers for short-term debt:

Figure 2

Source: U.S. Treasury

A normal market for sovereign debt would pay investors more for lending their money over several years, as opposed to a few months. However, the market for U.S. debt is not normal at the moment.

The inverted yield curve is in part the effect of inflation expectations, which motivate investors to demand higher yields for as long as they believe inflation will remain elevated. If their expectations stretch over a year, then any debt sold with a maturity beyond one year will come with a lower yield; the inflation premium, so to speak, is taken out of the picture. By contrast, when inflation is low and expected to remain low, yields will be governed by the risk premium that investors demand for lending their money over a longer period of time.

All of these common-sense properties of the debt market are valid under the assumption that there is no relative change in the supply of debt. If the supply of debt rises relative to the demand for debt, the price of the debt security falls, just like the price of oil drops when supply increases relative to demand. A drop in the price of a debt security means that the interest rate rises; when the Treasury substantially increases the supply of debt under short maturities, the interest rates on those maturities rise.

We have seen exactly this happen since late last year: the increase in supply has conspired with investor demands for inflation-compensating yields, resulting in an inverted yield curve on U.S. government debt. Over time, with inflation expectations subsiding, the slope of the yield curve has remained negative, suggesting that the U.S. government’s insistence on using the shortest maturity segment of its sovereign-debt instruments has cemented high yields in that debt segment.

All of this, again, puts a fool’s spotlight on the Treasury’s debt management strategy. We have reasons to worry that they will stick to this strategy. Therefore, we also have reasons to worry about debt yields becoming unmanageably high.

At some point, this leads to a fiscal crisis for the U.S. government.

Is anyone on Capitol Hill paying attention?