Back on August 23rd, I predicted that the Federal Reserve would cut its federal funds rate by 0.5 percentage points. On September 18th, the Fed did exactly that:

In the light of the progress on inflation and the balance of risks, the [Federal Open Market] Committee decided to lower the target range for the federal funds rate by 1/2 percentage point to 4-3/4 to 5 percent.

There were a lot of reasons why the Fed would move with this big cut, but—contrary to what some pundits would suggest—none of them have anything to do with the upcoming presidential election.

First of all, the Federal Reserve has been behind the curve in cutting its policy-setting funds rate. Normally, the Fed leads the ECB by being the ‘pace-setter’ on rate changes: the Fed cuts or raises its rate first, and the ECB follows suit very soon thereafter. This year, the roles have been flipped, with the ECB reducing its policy rates by one quarter-point in June and another one in August.

If the Fed waited much longer, it would have risked injecting instability into the financial markets, centered primarily around the market for U.S. debt.

Right here, we find the big reason why the Fed made its big cut. Over the past two years, the average annualized cost for the U.S. government’s debt has increased from 1.87% to 3.27%. Translated into actual money, this means that for every $1 trillion that the federal government owes, its annual interest payments have gone up from $18.7 billion to $32.7 billion.

This is a 75% increase in the cost of maintaining the debt—and we haven’t even taken into account the fact that the debt itself in the same period of time has increased by more than $4.3 trillion.

As much as the media tries to ignore this, it is a painful fact that the U.S. government is being overrun by the cost of its own debt. With its decisive 0.5-point rate cut, the Federal Reserve has provided alleviation for Congress, where our elected officials can now look forward to a much slower rise in the cost of the debt. As a result, the risk that investors should lose faith in the U.S. Treasury’s ability to pay interest on its debt has fallen.

But that risk has not gone away. The relief is short-term in nature—and the margin is thin between calm and stability on the one hand, and crisis and instability on the other. If the Fed had not made the big cut, but instead gone with the 0.25-point that mainstream analysts expected, it would have sent a sinister signal to debt market investors: the Fed is not taking your debt crisis worries very seriously.

More specifically, the smaller cut would have signaled to investors that the prevailing opinion among policymakers in the United States is that our government cannot suffer a fiscal crisis.

It can. And at some point, it will. The risk for a fiscal crisis has now been lowered—but only for the short term.

This short-term relief is essential. If the Fed had not been as decisive as it was, the interest-rate margin between the dollar and the euro would have increased. This would normally put upward pressure on the dollar, thus appreciating the U.S. currency vs. its European counterpart. Such appreciations worsen the balance of trade but improve the net of financial transactions between the two economies.

The practical meaning of this is that when the dollar increases in value relative to the euro, investors pour money into the U.S. stock and debt markets. The markets for currencies, equity, and debt stabilize and the two economies move along as usual.

In a scenario with no Fed rate cut, or a smaller one, that phase of stability would not have materialized. Investors in the market for U.S. debt would have started selling off Treasury securities. They would have dumped their dollars for euros and other currencies and left the U.S. government to financially fend for itself.

As the sell-offs accelerate, they would depreciate the dollar. This is a dangerous situation: the currency loses value while interest rates remain high and investors leave the market for Treasury securities. At this point, the Fed loses its control over the U.S. economy: since the market has lost faith in the Fed, the central bank cannot cut interest rates to restore stability in the debt market. A rate cut at this point actually weakens confidence among remaining debt market investors.

The only option here is to drastically, radically, and desperately raise the interest rate. When the Swedish Riksbank found itself in this situation 32 years ago, it raised its policy rate to 500% (yes, 500). When the Greek government reached this point during their debt crisis 12-15 years ago, their central bank peaked below 30%, but that was still a very high rate for a weak, crisis-ridden economy.

Since the Federal Reserve chose to make a big rate cut now, it once again leaped ahead of the financial markets and the U.S. economy as a whole. However, the main reason for doing this was to prevent even the first tremors of a U.S. fiscal crisis.

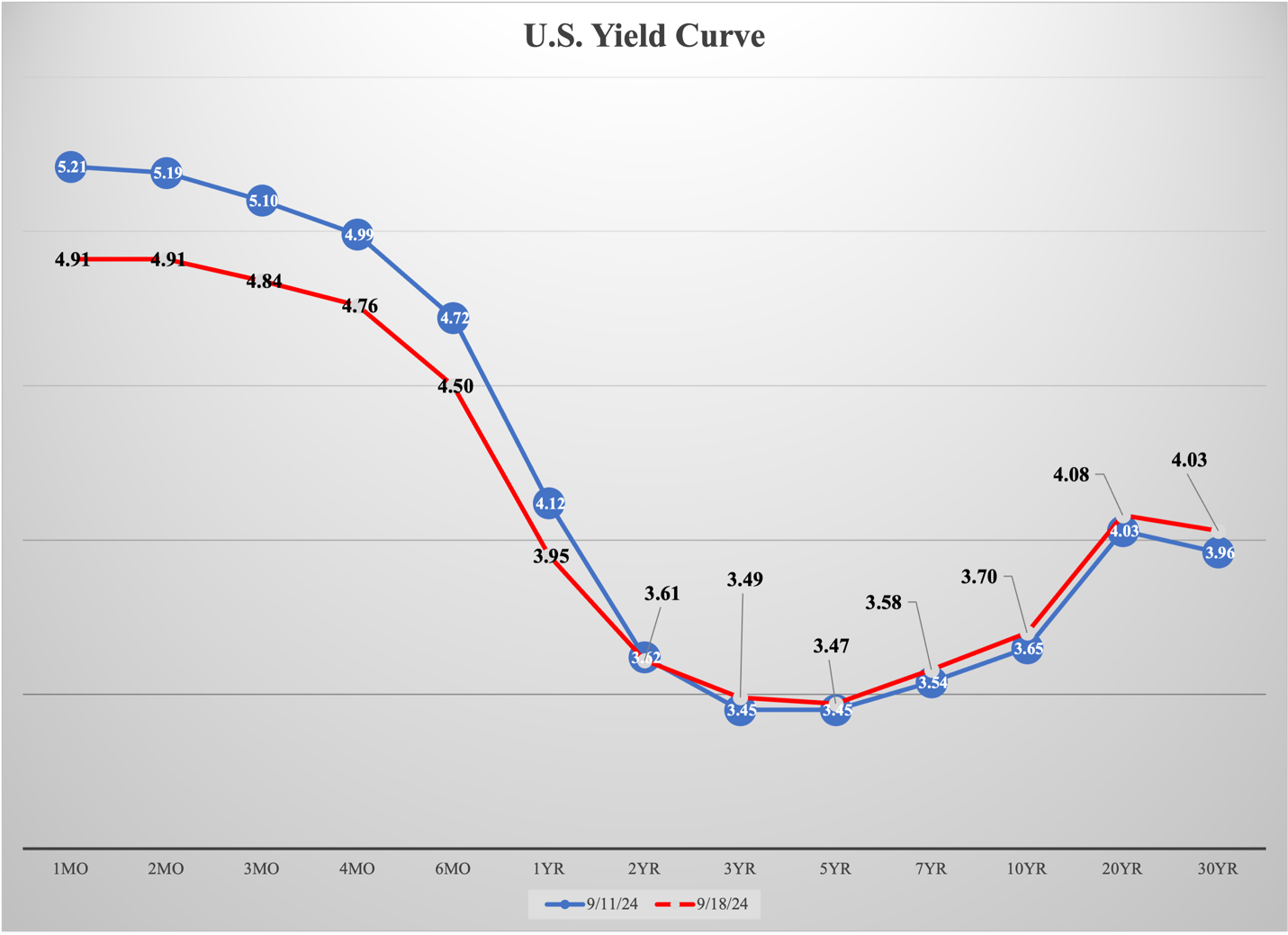

The Fed succeeded—at least for now. Figure 1 shows how much the short-term interest rates on the market for U.S. debt have fallen in the last week; a sizable portion of the decline took place on the same day as the Fed’s rate-cut announcement became public.

Figure 1

Congress has been given some well-needed relief, at least when it comes to the debt cost. But this also means that the ball is now in their court: if the newly elected majority—and the new president, whoever that will be—do indeed take decisive action to reduce the budget deficit, then today’s more or less desperate rate cut by the Fed will have led to something substantive.

If, on the other hand, Congress punts on the debt issue, just as it has for about half a century now, then the relief the Fed just gave them will be short-lived.