It is with rising frustration I watch Europe slowly walk backwards into the future, without anyone raising even a modest voice of concern about it.

Not only do I see this economic stagnation-to-decline trend in chilling economic statistics, but I also hear it being touted as a positive outlook on the future. On December 18th, ECB President Christine Lagarde explained:

Economic growth is expected to be stronger than in the September projections, driven especially by domestic demand. Growth has been revised up to 1.4% in 2025, 1.2% in 2026, and 1.4% in 2027 and is expected to remain at 1.4% in 2028.

Most analysts and commentators will not make it past the first sentence of this quote; their takeaway will be that the euro zone economy—the core of the European economy—will grow “stronger than” previously projected. That, of course, has no practical meaning: an economist’s forecast is not the same as economic reality.

The real dynamite in Lagarde’s statement is the series of GDP growth numbers for the next few years. Let me repeat those inflation-adjusted numbers again:

This is nothing short of an economic disaster unfolding in slow motion. A 1.4% growth rate after inflation is far below what an economy needs over time to preserve its general standard of living.

A slow decline in the standard of living has detrimental consequences that we rarely think about in our daily lives, yet the impact from that decline includes deteriorating health care, weaker education, less money for police, endless tensions around defense spending, and so on.

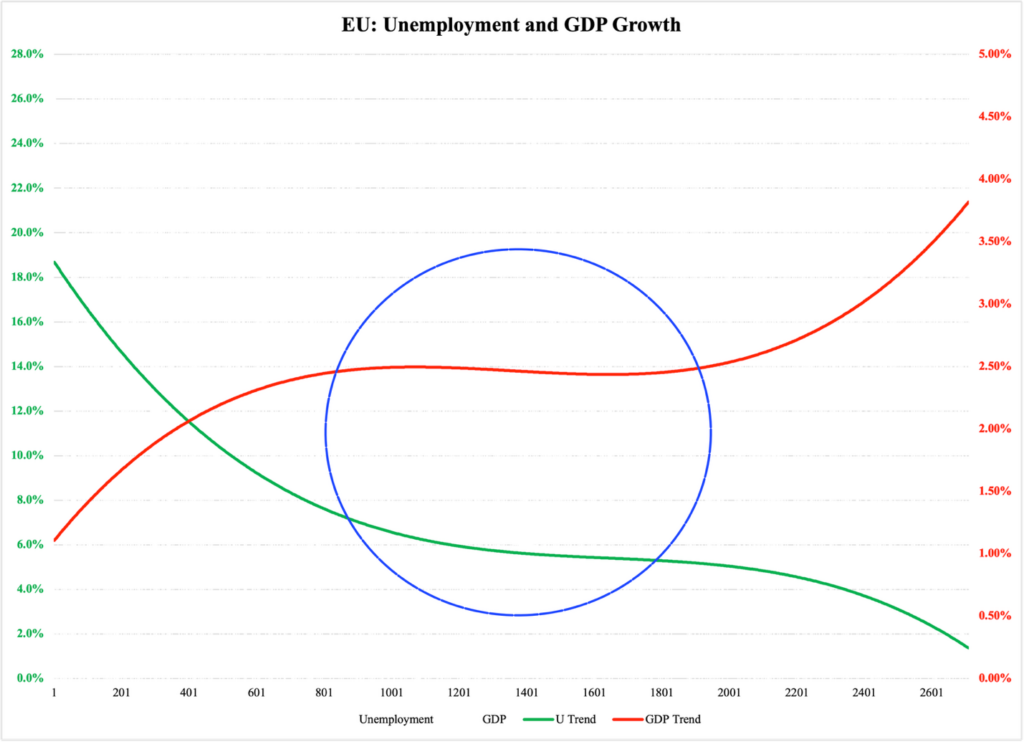

To understand the macroeconomic fallout from the numbers that Lagarde mentioned, let us have a look at some numbers for the European economy. Figure 1 compares the long-term trends of two variables: unemployment and inflation-adjusted GDP growth. The red trend line represents average GDP growth in relation to the green unemployment trend line: for every value of GDP growth there is a corresponding value of unemployment.

The trendlines are built out of 2,709 pairs of numbers for the two variables from all 27 EU member states. For example, in the first quarter of 2024, Germany had an unemployment rate of 3.1% and a GDP growth rate of -1.1%.

The collected data is quarterly from 2000 through the first half of 2025. The pairs of numbers are sorted from the one with the highest unemployment rate (observation #1—see the horizontal axis) to the one with the lowest unemployment rate (observation #2,709).

At the extremes, GDP growth is either very high or very low; these are the tops and troughs, respectively, of the business cycle. The troughs, to the left in Figure 1, combine low GDP growth with high unemployment; the cyclical tops reverse the combination.

In between the two outlier cases is a large segment of ‘normalcy,’ highlighted with a blue circle:

Figure 1

Over the past 25 years, the normal, or long-term stable state of the European economy has been one where GDP grows at around 2.5% per year, adjusted for inflation. This growth rate is combined with an unemployment rate around 6%.

The most recent unemployment numbers are slightly better at 5-5.4%. Economic growth, on the other hand, is lower than the Figure 1 ‘normal’ value: in the first two quarters of 2025, the EU economy as a whole expanded by only 1.3-1.4%.

Although unemployment is relatively low now, the long-term outlook with GDP growth at this low level is unequivocally pessimistic. Since the ECB forecast through 2028 suggests a GDP expansion below the long-term stable level in Figure 1, unemployment will slowly move upward in the coming years. Let us plot the ECB forecast into Figure 1 as a dashed blue line (I will explain the other dashed line in a moment):

Figure 1a

Since the green and red lines represent historical data, the 1.4% growth rate in the ECB’s outlook is not the same as it will be going forward. This means, plainly, that the European economy is able to maintain a lower unemployment rate now than it was in the past at that same level of economic expansion.

But is this not good? Is it not positive that instead of the 16% or higher in Figure 1, a 1.4% GDP growth rate keeps unemployment below 5.5%?

Sadly, no. The growth rate that Christine Lagarde presented as a new normal has historically been a recession growth rate. Today, it is the level where output—the production of goods and services and the generation of household income—is at a ‘normal’ level.

If we flip the story on its head, we can see what this actually means. According to Figure 1, historically, the European workforce has been able to generate 2.5% GDP growth when unemployment has been at the current level. Today, that same employment level grows the economy at a full percentage point less.

This tells us that Europe suffers from low labor productivity. The workforce—for no fault of its own—is not adding enough value to meaningfully expand Europe’s total amount of economic resources. They used to do that, but now they don’t.

In practical terms, this means that they are not producing enough value to maintain the standard of living they currently have. Herein lies a blunt message for Europe’s future: your children are growing up to a less prosperous life than you had. Their children, in turn, will never reach their parents’ standard of living. Slowly, a couple of percentage points at a time, the European way of life is becoming harder to attain, less common—and eventually a distant memory.

The black dashed line in Figure 1a represents a 2% growth rate that—according to something called Okun’s Law—has historically been considered the ‘least tolerable’ if an economy wants to maintain its standard of living. It has been deemed the growth rate needed to prevent unemployment from rising, while also not being strong enough to reduce it.

This number is based on relatively old data; more recent research suggests that this ‘break-even’ point is higher, possibly closer to 3% growth per year. Either way, it is higher than where Europe can expect to be for the foreseeable future. This means that even with a higher utilization of its workforce, Europe is stuck in a sad state of stagnation. The consequences are dire:

Without any drastic, substantial, and long-term reliable turnaround, it will only take one generation for Europe to fall to the lower global half of living standards. While America continues to thrive, Asia keeps rising, Latin America has learned from its past, and Africa is briskly generating new hotspots of growth and prosperity, the European future is littered with uncertainty, institutional instability, and economic decline.

I refuse to believe that Europe’s peoples are content with this outlook. The only question is: what are you going to do to save your continent?