In the summer of 1990, while exploring opportunities for graduate school, I attended a conference in Cambridge, UK, for scholars and students in the history of economic thought. It was a highly enriching experience, but the best part was my personal conversation with Sir Austin Robinson.

Born in 1897, Sir Robinson had spent all his academic life in Cambridge. He was a prominent economist in his own right, as was his wife Joan Robinson. Sir Robinson also worked with the big names of his time, including John Maynard Keynes and Roy Harrod.

I asked Sir Robinson about the banking crisis that was unfolding at the time. The 93-year-old man immediately launched into an insightful comparison with the Great Recession 60 years earlier. I could tell how much he enjoyed explaining current events in the context of his own life experience and his academic scholarship.

He passed away three years later. I am nowhere near Sir Austin Robinson in either age or scholarship, but as I look at the banking crisis unfolding here and now, in March 2023, I can relate to his joy in drawing on experience in explaining current events.

The news media is currently filling up with references to a banking crisis. On March 13th, CNN reported that in the aftermath of the Silicon Valley Bank collapse a couple of days earlier, investors were “on the edge about whether its demise could spark a broader banking meltdown.” Six days later, the British newspaper The Guardian hinted at systemic problems by suggesting erroneously that banking deregulation was behind the SVB implosion. On March 20th, U.S. news outlet CNBC explained that the SVB collapse “has rippled through the broader banking system.”

Statements like these will surely help raise the volume about a possible systemwide banking crisis. I am not going to contribute to that. In fact, we should all be careful about determining whether or not such a crisis is at hand. Having lived through and researched two major economic downturns with significant problems in the banking sector, I am inclined to suggest that so far, we are not in a systemwide crisis. There are no clear signs of one bank’s poor performance contaminating the performance of other banks.

In other words, there are no apparent, direct transmission mechanisms from bank to bank. What we see now is, instead, more reminiscent of what the world experienced in the economic crisis that broke out in late 2008. There is also an element of the crisis from the early 1990s, although the parallels back to that episode are weaker than to the Great Recession.

Both these historic economic crises had in common that banks lost money in part as a result of overexposure to one class of assets. In the 1990s, that class was real estate lending—commercial as well as private—while, in 2008-2012, the problematic asset class was sovereign debt.

But wait: how can banks end up in trouble because they invest in government debt? Is that not the safest type of asset you can possibly invest in?

Under normal, or, shall we say, natural economic circumstances, that is correct. The problem is that government institutions, including but not limited to central banks, have distorted the market for sovereign debt to the point where normal risk assessment no longer applies.

This is what makes this banking crisis—such as it is—different from the crisis of the early 1990s. Back then, the global economy was coming off a long, seemingly unending episode of full employment and economic growth. Banks in some countries—Sweden and Finland are often mentioned as primary examples—had overexposed themselves primarily to the commercial real estate market. A rapid fall in property values left investors upside down in their balance sheets and their cash flows, whereupon their creditors, i.e., the banks, began losing money.

In the early 1990s, the United States lived through a smaller banking crisis centered around so-called Savings & Loans institutions. Operating under different conditions than traditional banks, the S & L institutions included social goals in their activities. In fact, the S & L institutions had “their origins in the social goal of pursuing homeownership.”

For this reason, their asset portfolios were heavily invested in the mortgage market. They were also regulated by the federal government, e.g., in how high interest rates they could pay depositors. When market interest rates exceeded the permitted S & L cap, customers pulled their money and went to traditional banks instead. In combination with a sharp downturn in the real estate market, causing a decline in mortgage values, the deposits drainage eventually brought down the S & L system.

None of this applies to our present-day situation, but the part about mortgage exposure is relevant. It points to the problem with putting too many eggs in the same basket. The crisis in 2008 and 2009 had more of that element to it, so much in fact that this episode has become known as a financial crisis.

The banking problems that emerged during the Great Recession were almost universally caused by irresponsible overexposure to overinflated equity values. Equity values began deflating in the same way as in the 1990s crisis: as I explain in The Rise of Big Government (pp. 93-99), a sharp downturn in economic activity caused unemployment to rise, and businesses to fail. As a logical consequence, debtors defaulted on their obligations and bank balance sheets deteriorated rapidly.

One thing that was different in the Great Recession from the 1990s crisis was the banking system’s much higher exposure to government debt. In my book referenced above, I account for the significant amounts of sovereign debt that banks in Europe gobbled up during the crisis, and how the European Central Bank sponsored those purchases with virtually free credit. In short, the ECB monetized government deficits by using commercial banks as intermediaries.

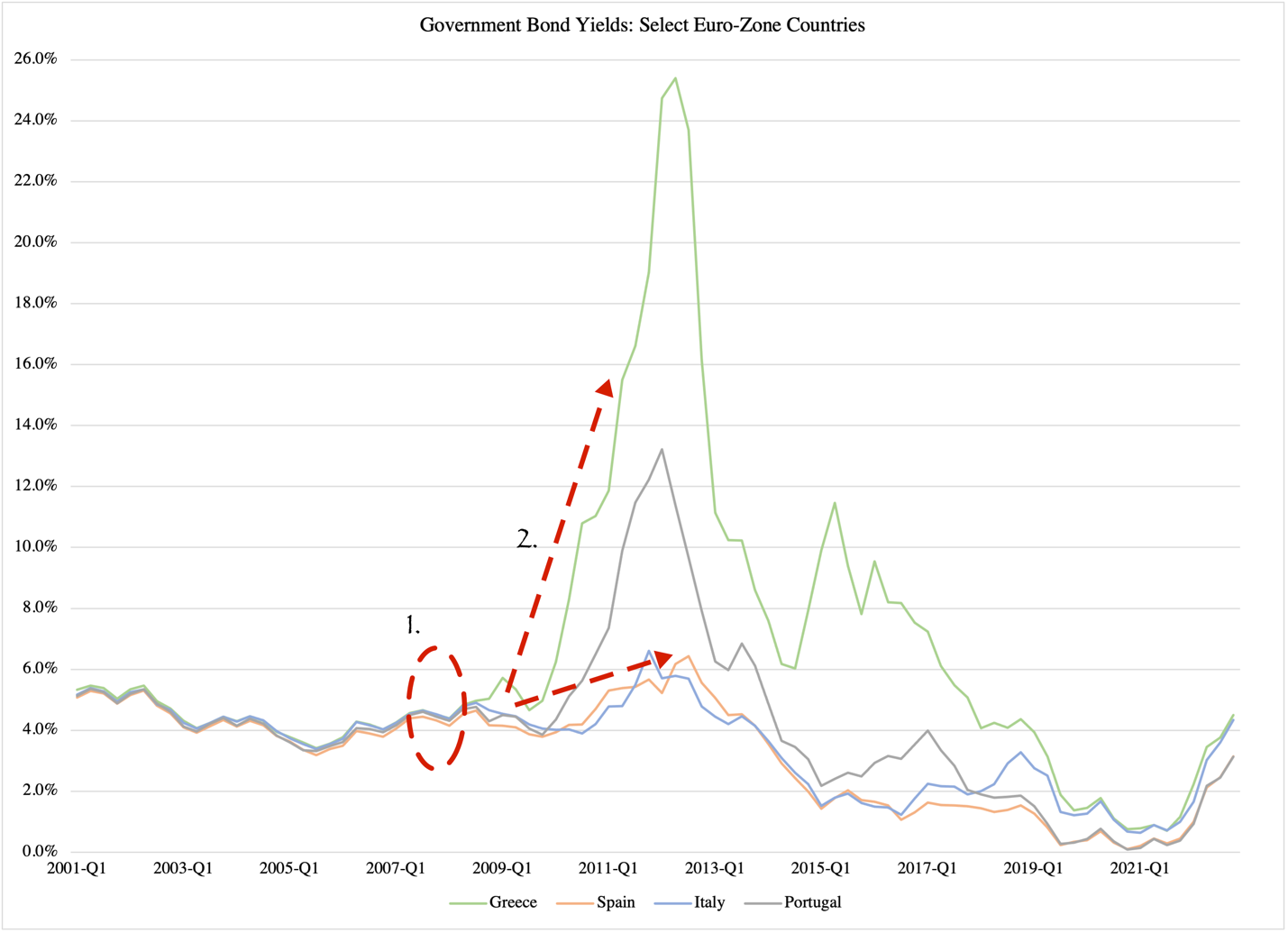

By printing an excessive amount of money in a short period of time, the ECB pushed European interest rates down. It was at this point that many banks acquired government debt; see point 1 in Figure 1 below. Then, as the crisis expanded (due to austerity policies that raised taxes and cut spending during an economic downturn), many governments found it increasingly difficult to sell their debt. This led to sharply rising interest rates—arrows at point 2 below—which is the flip side of falling prices of government securities:

Figure 1

Source: Eurostat

In the couple of years following the outbreak of the crisis in 2008 and 2009, banks holding large portfolios of government debt saw their balance sheets be diminished by falling debt-security prices.

At that time, the ECB had a program in place to buy all kinds of euro-denominated debt: they guaranteed the price, regardless of the credit status of the issuing government. This helped commercial banks, working as a stop-loss measure and helping them maintain or retain their financial solvency.

The problems in the banking sector today appear to be of the same nature. After the 2008-2012 period, the ECB continued its expansionary monetary policy. As Figure 1 above shows, from 2013 to 2021, interest rates declined from their height at the cusp of the Great Recession. (The countries illustrated here are good representatives of the overall trend in the euro zone.) With declining interest rates, again, come rising prices on government bonds. The trend was protracted, encouraging banks to get back into sovereign debt ownership.

By 2021, financial corporations owned substantial parts of government debt across the EU. Table 1 reports these shares for 2018-2021, with red numbers marking an increase in 2021 over 2018:

Table 1

Source: Eurostat

Eurostat does not have fully covering data for all EU member states on who owns sovereign debt, but the numbers they do provide are compelling enough. In countries where financial corporations, i.e., banks, own half or more of total government debt, even a modest decline in the value of that debt will be widely felt throughout the banking sector. The exact impact varies from bank to bank, of course, depending on how much debt they have in their portfolios; some banks will suffer fairly big losses while others don’t.

It is interesting to see how the banking sector has expanded its investments in the very assets that contributed to the sector’s crisis a decade earlier. The losses suffered at that time do not seem to have been discouraging, nor were banks discouraged by the very low interest rates in 2018-2021. When interest rates, a.k.a., yields, are at or below zero, the bank gets no income from owning those securities. At the same time, the very low interest rates clearly suggest that the price of the bond reasonably has reached its peak—it cannot rise any higher. Therefore, the bank cannot expect to reap any capital gains from owning government debt.

Why, then, did banks buy sovereign debt under these circumstances? There are two options: they wanted to expand their holdings of virtually or actually risk-free assets, or they wanted to obtain cheap liquidity for other purposes.

The first option is unreasonable, at least at the proportions needed for the numbers in Table 2. When an asset is so highly priced that it can only lose value, it loses its function as a risk-free portfolio anchor. The point of such assets is that they balance out the risks taken with other assets, such as mortgage loans: if a bank loses €100,000 on a loan to a homeowner who could not pay it back, it can sell €100,000 worth of risk-free assets and restore the lost liquidity.

A government security that is priced at the theoretical top of its potential when the bank buys it—in other words which pays zero interest—cannot serve that function. The price can only fall, and with it, the value of the security.

The risk for a price drop increases if the yield, i.e., the nominal interest rate, is below inflation. In this situation, the security pays a negative interest rate, making it an unsustainable option for long-term investors in general. A negative real rate can only be sustained if the central bank depresses the nominal rate, which in turn means that anyone who wants to buy government securities at a negative interest rate will lose money the instant the central bank abandons its accommodating monetary policy.

Long story short: a commercial bank that wants to keep sovereign-debt securities as a risk-free anchor in its balance sheet does this with the best results if it acquires the bonds when interest rates are relatively high. That was not the case in the years after the Great Recession, and therefore it is unlikely that the numbers shown in Table 1 are the result of risk-management decisions.

This leaves us with the second option, namely that the ECB and non-euro central banks within the EU supplied the banks under their currency jurisdictions with virtually cost-free credit on the condition that they buy sovereign debt. If the cost of the loan was even marginally lower than what they could earn on the debt securities, the deal was positive for the banks. If this allowed them access to almost cost-free loans for other investments as well, and if the ECB offered a buyback guarantee on all euro-denominated sovereign debt, the deal was practically fail-safe.

Until, that is, the ECB changed its monetary policy, drove interest rates upward, and depressed prices on government debt.

It is natural that a large number of banks will take losses to their balance sheets from the price plunge that has followed ECB’s rising interest rates. What is not natural is the price plunge itself, or more correctly, the extremely low interest rates that preceded the price plunge. Those rates were, bluntly speaking, aimed at preventing Europe’s indebted welfare states from going insolvent.

With all that said, it seems unreasonable that the banks in both America and Europe should have bought so much government debt that recent interest-rate hikes would cause a crisis of systemic proportions. I suspect that something else is afoot here. What that might be, I cannot say at this point.