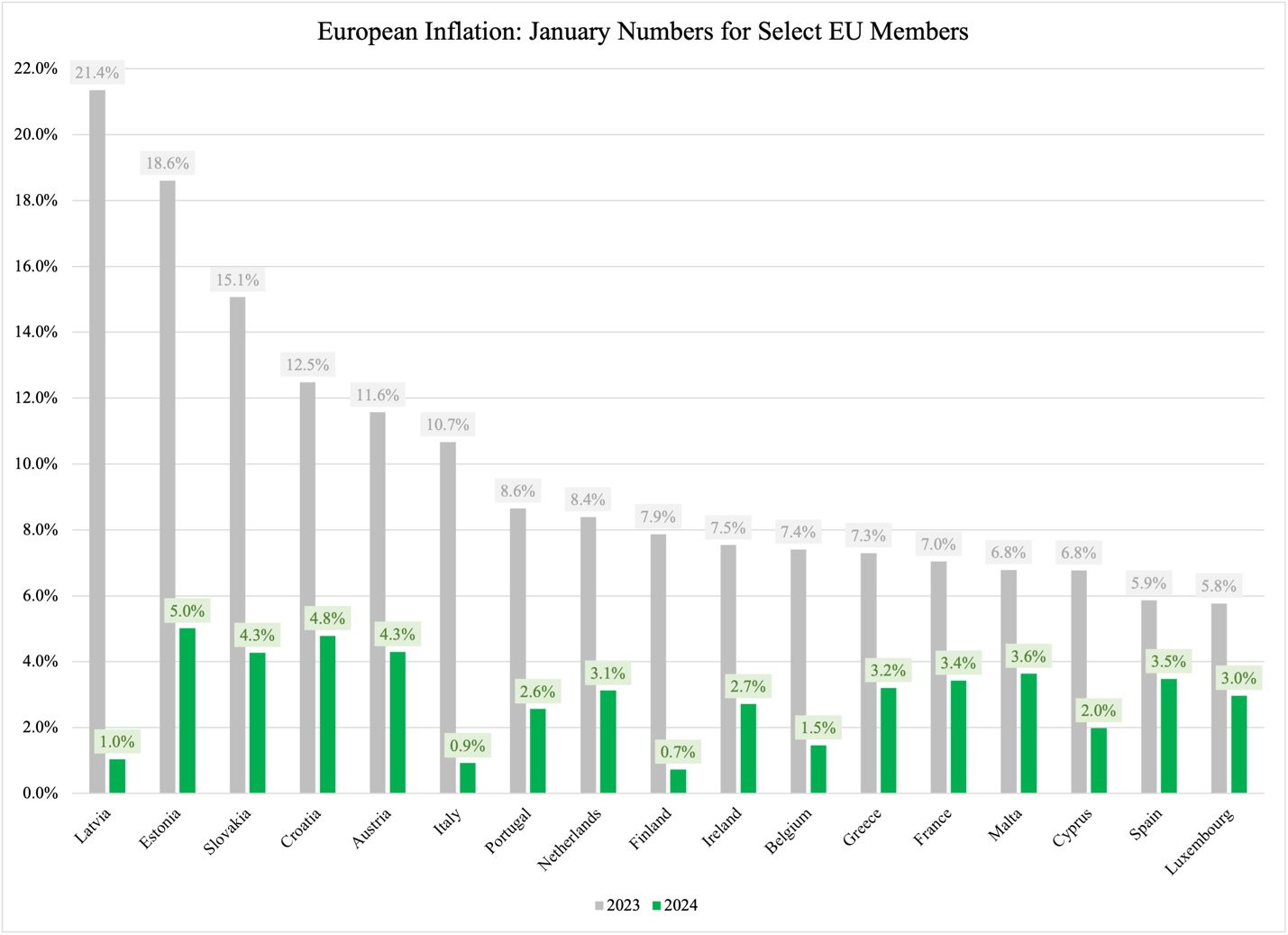

The new year starts with good news on European inflation. By February 12th, Eurostat had published consumer-price inflation rates for 17 EU member states. As Figure 1 shows, the rates for January 2024 are substantially lower than the rates were in January 2023:

Figure 1

Of these 17 countries, Latvia has made the most remarkable achievement in bringing inflation down, from 21.4% to 1%. To date, this is a record in the EU, but it might not stand for too long. A year ago, Hungary led the EU with 26.2% inflation; in December last year, it was down to 5.5%. The downward trend in Hungarian inflation is strong; if it persists into January, the rate should be in the 3-3.5% bracket.

Eurostat also reports a preliminary inflation rate of 2.75% for the euro zone. This is a nice, big drop from 8.6% in January 2023.

At the same time, we should also acknowledge that the currency area is unlikely to see further drops in inflation:

The latest number of 2.75% is a projection based on the 17 euro-zone members that have thus far reported inflation data for January 2024. Once the remaining member states have added their figures, the inflation rate is likely to change, but only marginally. The current January number suggests that inflation has stabilized in the currency area—and this is important when we assess which way the ECB may go at its next monetary policy meeting in March.

As another indication of inflation stability, of the 17 EU states that have reported inflation for January, eight had a higher inflation rate than in December. In most of them, the increase was minor, but the Dutch and Portuguese inflation rates went up by a fair amount: from 1% to 3.1% in the Netherlands and from 1.9% to 2.6% in Portugal.

The Portuguese inflation hike is not marginal, but also not something to really worry about. The Dutch inflation spike is more worrisome, but since it is an outlier in the current crop of inflation reports, we can safely conclude that the euro zone has reached a point of relative price stability. The currency area has put this inflation episode behind it.

Does this mean that the European Central Bank plans to start lowering interest rates? We could glean a hint of that from what representatives of the ECB tell us, but that may not yield much information; central bankers are essentially politicians without the ability to promise away other people’s money. Therefore, their statements are often meant to reveal as little information as possible at any given point in time.

A better way to assess the ECB’s policy moves in the coming months is to look at the euro zone economy from a broader perspective. Inflation is, of course, the central bank’s most important indicator when making interest rate decisions. The ECB wants inflation to be at 2%; since the current rate of 2.75% seems to be stable, this would indicate that the ECB is not open to cutting its three policy-leading interest rates any time soon.

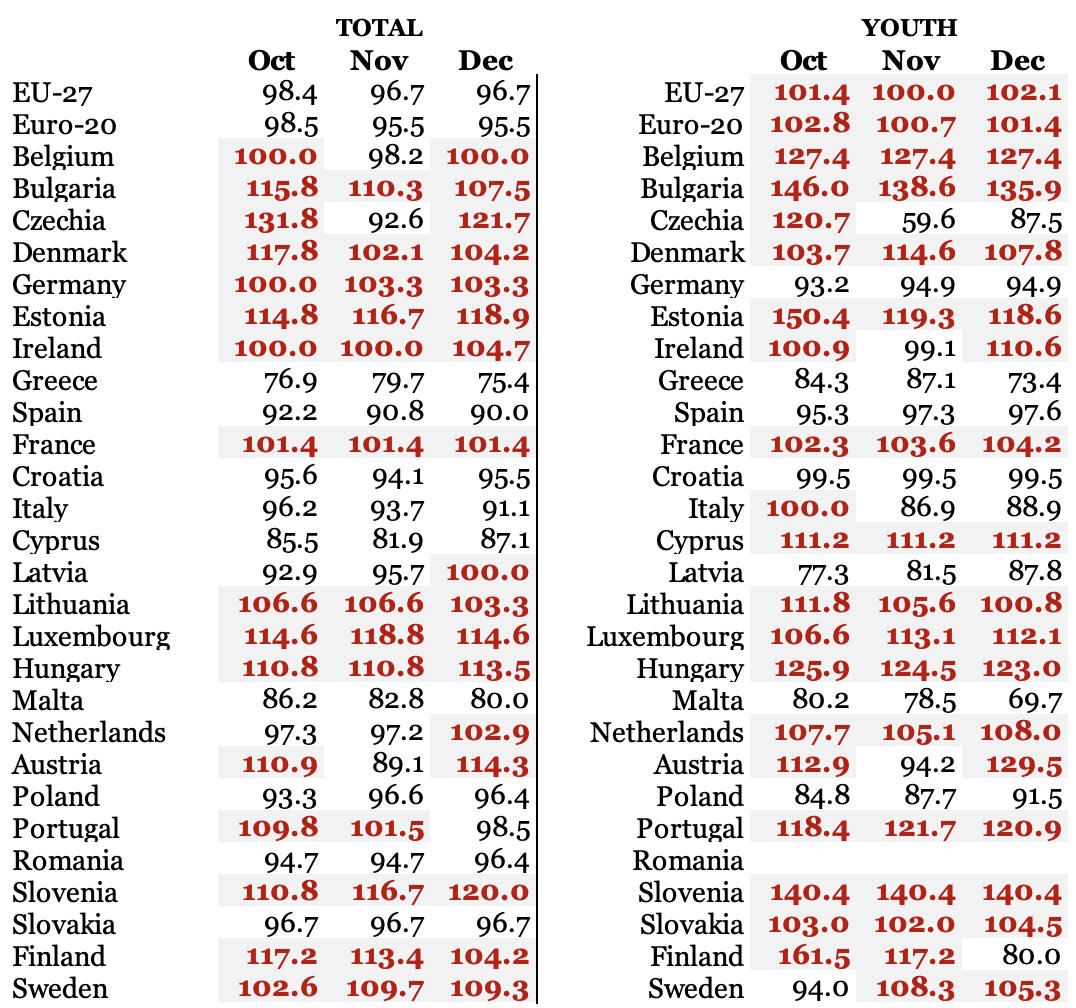

That conclusion is contradicted by an examination of the latest unemployment figures. Table 1 compares unemployment rates in the EU and its member states. The comparison covers the last three months of 2023 with the same period in 2022 and looks at the total labor market (the left column) as well as young workers (right). If the number reported is higher than 100, it means that unemployment is higher in 2023 than in 2022.

For example, in December, the total number reported for Spain is 90, while it is 101.4 for France. This means that Spain had a lower unemployment rate in the last month of 2023 than in the same month in 2022, while the opposite was true in France.

Table 1

This table reveals a problematic trend in unemployment. In the “Total” column, 17 countries had a higher unemployment rate in December 2023 than in December 2022. A surprising 12 of them had a higher rate for all three months covered, revealing a trend of rising joblessness that has been underway for some time.

The “Youth” column is even more troubling. Here, 18 member states saw a rise in youth unemployment from December to December, and 15 of them had the same problem in both October and November.

This is an unusual way to look at trends in the labor market, but it helps us assess trends that otherwise would not be apparent. As far as the labor markets are concerned, Europe is definitely on its way into darker, more troubling times, although it is worth noting that in some instances, the unemployment rate in 2022 was exceptionally low. A slight increase in unemployment in Hungary is not nearly the same cause for concern as it is in Sweden:

Taking into account the differences in actual unemployment rates, the trend numbers shown in Table 1 should ‘encourage’ the ECB to cut interest rates in the near future. On the one hand, total unemployment for the euro zone was lower at the end of 2023 than the same period a year earlier; on the other hand, 12 euro zone countries experienced an uptick in total unemployment. On the youth side of the labor market, the numbers were notably worse.

Eurostat has not yet published GDP numbers for the last quarter of 2023. These figures will tell us a great deal about where the European economy is heading. Given what the unemployment numbers tell us, we should expect a slowdown from the third quarter. This, in turn, would mean that Europe entered 2024 and stepped straight into a recession.

Again, the definitive verdict on that part will have to wait. For now, the combined picture of inflation and unemployment speaks in favor of an ECB rate cut at their meeting in March.