This week’s Fiscal Forecast America explained how higher interest rates and a weaker stock market have made U.S. financial markets weaker. Investors who were hoping to cash in on capital gains have been snubbed, both on their stock portfolios and on the markets for corporate and government debt. This has led to weaker tax revenue for the U.S. government, as the highest-earning taxpayers, who pay a disproportionately large share of federal taxes, earn a substantial share of their incomes on investments.

A similar trend is underway in Europe’s financial markets, though its effect on government revenue is less decisive. European governments depend to a larger degree on consumption-based taxes, and on income taxes that are more evenly distributed across income segments. In short: high value-added and excise taxes, and high income taxes already on low incomes have given Europe’s welfare states a more diverse income profile than the American government has.

That is not to say the European governments will escape unscathed as their financial markets shake. They will take a beating, but it will vary from country to country depending on how important those markets are to government revenue. There are, of course, taxes on equity-based income, including rather high taxes on capital gains and taxes on stock dividends. This means that investors get hit by taxes regardless of how they profit from owning stocks: by relying on the speculative rise in stock prices, or by means of more long-term planning with a focus on dividends.

Some countries levy a financial transactions tax on the purchases and sales of some types of assets. In addition, a few unlucky Europeans also have to pay a wealth tax once their investments have made them ‘wealthy.’

In short, financial markets are important to governments that need a lot of tax revenue to pay for their welfare states. The problem with taxes levied on financial markets is that they generate unstable revenue. This is especially the case with taxes on capital gains: when investors in general lose more money than they gain because the stock market is in decline, the tax becomes a de facto loss to government.

Similar losses happen when corporations, due to tough economic times, reduce or cancel stock dividends. However, the stock market is not the only source of volatile tax revenue: the debt markets fall into the same category. All it takes for investors to lose money on those markets is for interest rates to rise. They go up because the price of the debt instrument—the corporate bond or the government treasury security—has fallen. Since the yield is a fixed amount, the lower price technically means the interest rate rises.

When the stock market falls at the same time as interest rates rise, the net effect on financial-market-based tax revenue can be significant. This is happening right now in Europe, and the reason is the continent’s apparently inevitable descent into a recession. Unlike the American economy, Europe—as I explained in last week’s Fiscal Forecast Europe—is seeing unemployment rise and economic activity stagnate.

There are voices from time to time in the media who blame this emerging recession on the European Central Bank’s higher interest rates. This is an incorrect accusation: the European economy is perfectly capable of entering a recession on its own. However, as I predicted in my last Forecast for Europe, it will not be long before the European Central Bank reinstates its expansionary monetary policy.

In fairness to the ECB, they have only had one real period of dedicated monetary expansion: in the 2010s. The first expansion visible in Figure 1, in the first decade of the euro’s existence, was due primarily to new countries joining the currency area:

Figure 1

Source of raw data: European Central Bank

The rapid expansion of the money supply in the 2010s is partly to blame for the long stock-market rally that took place during those years. However, before we get there, let us straighten out how the end of the monetary expansion period has brought about capital losses in debt markets.

The ECB ended its long money-printing period in 2020, as soon as the pandemic and related monetary support programs reached their peak. However, the first phase of reducing the speed with which the supply of euros was growing basically just constituted a return of monetary policy to ‘normalcy.’ In the ECB’s case, this meant growing the money supply at 6% instead of 10% per year.

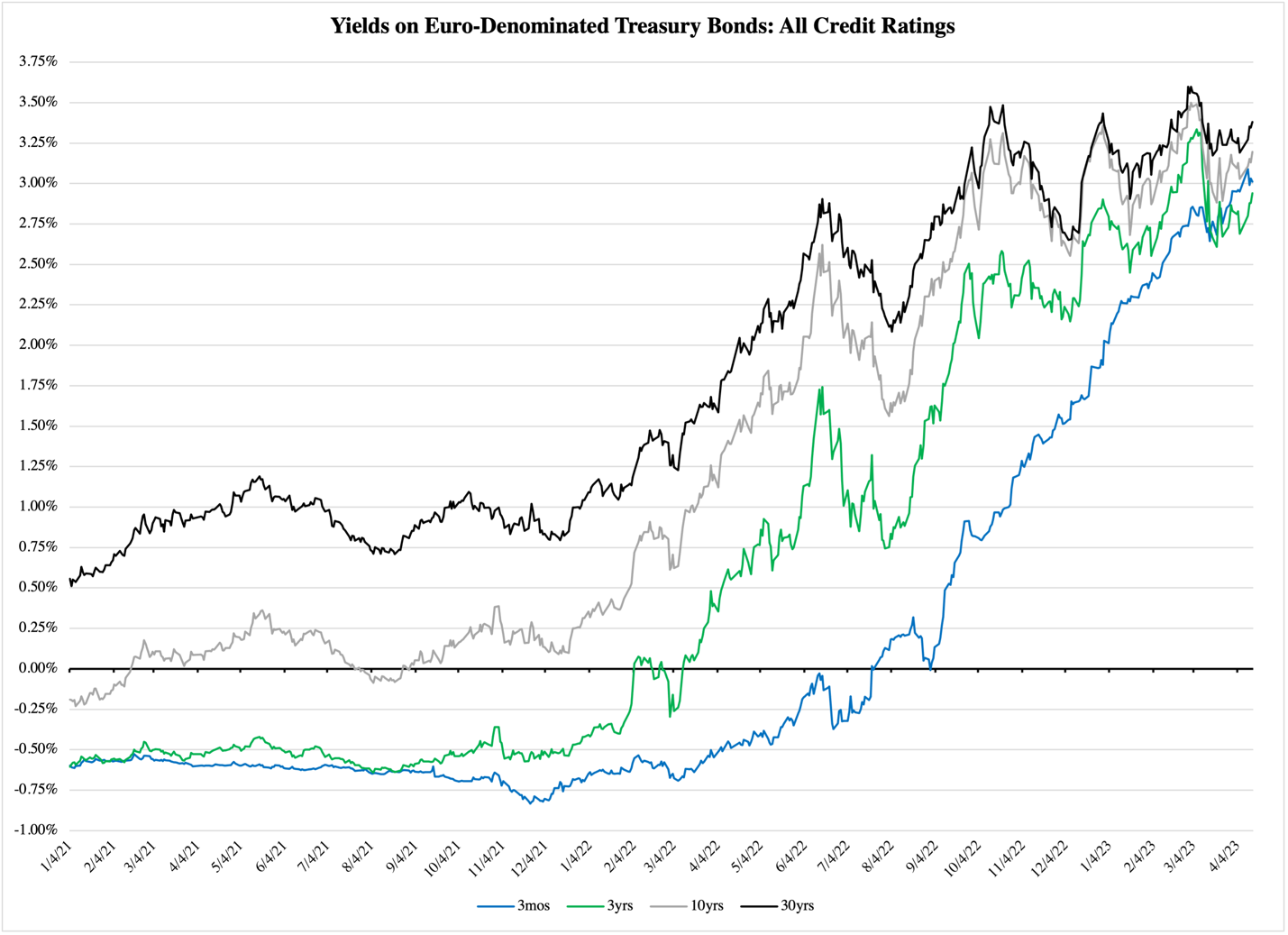

The actual shift in monetary policy happened in early 2022. It was the ECB’s inevitable response to the Federal Reserve’s shift from monetary expansion to monetary contraction. It led to sharply rising interest rates: in about a year, the yields on euro-denominated sovereign debt rose from less than 1%—and negative yields for some maturities—to 2.75-3.5%. Figure 2 reports a sample of maturities:

Figure 2

Source: European Central Bank via Eurostat

These rising interest rates, or yields, have a chilling effect on investor portfolios: when yields go up, the value of the underlying asset falls. This means that those who purchased euro-denominated government debt when interest rates were low, i.e., prior to 2022, have to shift their portfolio strategy or perish in the dark shadows of capital losses.

To governments, the shift in bond markets from rising value to rising yields does not have to be bad. If the rising rates outweigh capital losses as a basis for tax payments, government could even make out as a winner.

That is very difficult to do on the stock market. The primary reason is that there is no inverse correlation between dividends and capital gains: while the rise in interest rates on bonds depends directly on the decline in the bond price, the dividend on stocks may actually fall with the price. A dividend is not written in stone but can be changed by the stock issuer. If the company is going through financial difficulties and investors sell its stock, the company may use a dividend cut as a way to reduce its financial obligations. If they do, the dividend and the stock price fall together.

In this instance, government stands to lose tax revenue from two sources; unlike the debt-market securities, there is no compensatory effect on the income side for losses on the capital-gains side.

There is a clear trend of stagnation in stock markets right now; this is a good time for tax collectors to expect less revenue from capital gains. The Frankfurt stock exchange is a telling example: as Figure 3 reports, using the leading Dax Index to illustrate, the stock market recently offered a long streak of rising prices. From at least 2012 through 2018, capital gains were easy to come by.

After a pause through 2019 and a hiccup during the pandemic, stocks traded in Frankfurt began rising again. However, when interest rates started rising, stock prices declined again; the rebound that happened late last year has not yet returned to the Dax Index peak in late 2021:

Figure 3

Source: TradingView via Frankfurt Stock Exchange

The Paris Exchange offers a similar view. Its historical data of the CAC 40 lead index goes back further in time, offering a nice comparison of the long capital-gains friendly streak over the past decade to the previous two decades:

Figure 4

Source: Paris Stock Exchange

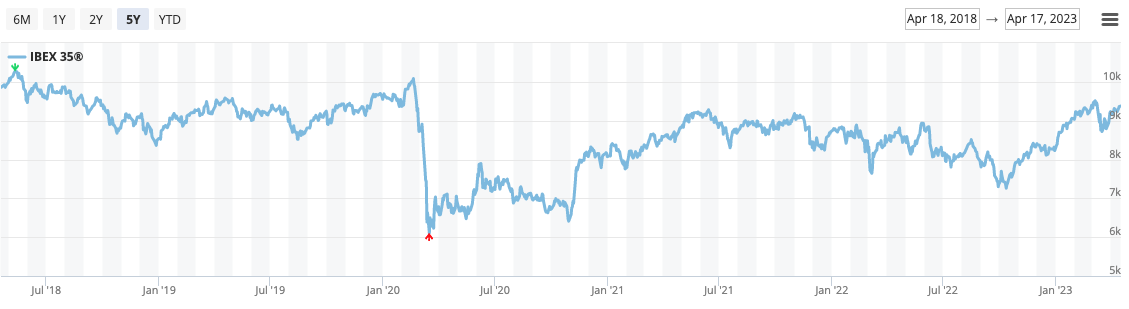

Not all euro-zone stock markets have shown this kind of strength. The Madrid exchange has been weaker, at least over the past five years (the maximum period for which it offers public data), with the IBEX 35 index being stagnant already in 2018:

Figure 5

Source: Madrid Stock Exchange

The weakness of the Spanish stock exchange is likely a product of the perennial weakness of the Spanish economy, but it is also a product of the fact that Spain belongs to the euro zone. To explain this point, consider the Swedish stock market, which has performed on par with the largest exchanges in the euro zone. The two countries are comparable from a macroeconomic viewpoint: Sweden has not done much better than Spain in the past 10-15 years. However, since Sweden remained outside of the euro zone, its currency has been allowed to move with the ebbs and flows of the currency market.

For Sweden, this has meant a slow, gradual depreciation of the krona vs. the euro. In 2012 €1 cost SEK8.35; in 2020 the price had risen to SEK10.50. This has attracted a steady flow of foreign investors into the Stockholm stock market: with the krona getting cheaper, foreign investors evaluate Swedish investment opportunities more favorably. This led to a continuous inflow of money and rising stock-market values, despite the weak underlying Swedish economy:

Figure 6

Source of raw data: Stockholm Stock Exchange

Things changed drastically when the stock market peaked. As much as the slow depreciation of the krona was a blessing for stock-market investors over a long period, it became an acute problem when the market no longer produced capital gains on the balance. The shift in the market came abruptly:

Over the same period, the Swedish krona lost 7% of its value against the euro, one of its biggest losses in recent years. Foreign investors made sure to bring their money out of Sweden while they could cash in net gains, despite the weakening currency.

All these examples of stock markets illustrate how rapid shifts from capital gains to capital losses can appear almost overnight, and how quickly they can therefore affect government budgets. If there is any place where easy tax-revenue gains rapidly turn into easy tax-revenue losses, it is in the financial markets.

Given the current trend in these markets, and given that the broader macroeconomic context points to a recession, it would be wise for Europe’s lawmakers to prepare for revenue losses, courtesy of weaker financial markets. Depending on how bad the recession becomes, those losses could turn significant.