On Friday, March 13th, a major event took place in Swedish politics. Two parties, the Liberals and the Sweden Democrats, put their long-held differences aside and announced a partnership for the September election.

Ever since the national-conservative Sweden Democrats (SD) were first voted into the Riksdag in 2010, the center-right Liberals have openly opposed the very thought of any government with SD cabinet members. This has complicated things for the center-right in general, which, in addition to the liberals and the SD, consists of the Moderate and the Christian Democrat parties.

After their election victory in 2022, the center-right managed to negotiate a platform for forming a government, where the Liberals’ unyielding opposition to SD cabinet positions produced a three-party government with coalition-strength parliamentary support from the SD. Over the years since, the Liberal Party has lost enough voter support to now poll well under the 4% threshold for winning seats in parliament. Meanwhile, the SD has gained voter support and is now polling 2-3 percentage points above their 2022 election results.

With the risk of fading into irrelevance, and with the risk of costing the center-right coalition its parliamentary majority, the Liberal Party offered an olive branch to the SD. After what party spokespersons referred to as ‘conversations’ between the two, a so-called partnership was agreed upon. It contains concessions from both sides on policy issues where they disagree, one of which is that the Liberals agree to let the SD assume cabinet positions.

Another concession, from SD this time, is an agreement to hold a new referendum on Swedish euro membership. The Liberals are the strongest proponents of replacing the krona with the euro, while the Sweden Democrats are steadfastly opposed to the currency union. This makes the referendum—tentatively slated for election day 2030 but likely to be held much sooner—a major political gamble, especially for the Liberals. The euro referendum in 2003 resulted in a 60-40 vote split against the euro; forcing a new vote on the Swedish people and losing that vote would mean the end for the Liberals.

The Swedish Democrats, on the other hand, will be winners either way: given a center-right election victory in September, they will get cabinet positions long before the euro referendum is held. If the referendum favors the euro, they can point to the ‘voice of the people’ and bask in the light of government power; if the referendum opposes the euro, they can claim total victory as the Liberals wither in the political wilderness.

If the euro referendum were held today, the pro-euro side would probably lose, but the margin would be nowhere near the 60-40 from 2003. The Swedish economy is not in very good shape, which makes it easy for euro proponents to—falsely—claim that a euro membership would solve all the problems with slow growth, high unemployment, and sagging real wages.

This time, it will not be up to the euro proponents to make their case—it will be the euro-skeptic side that must convince the voters.

Fortunately for the euro skeptics, facts are on their side. The euro zone is a ball and chain around the ankle of its members. For a host of reasons that deserve their own article, Sweden would sink further into economic stagnation if they adopted the euro.

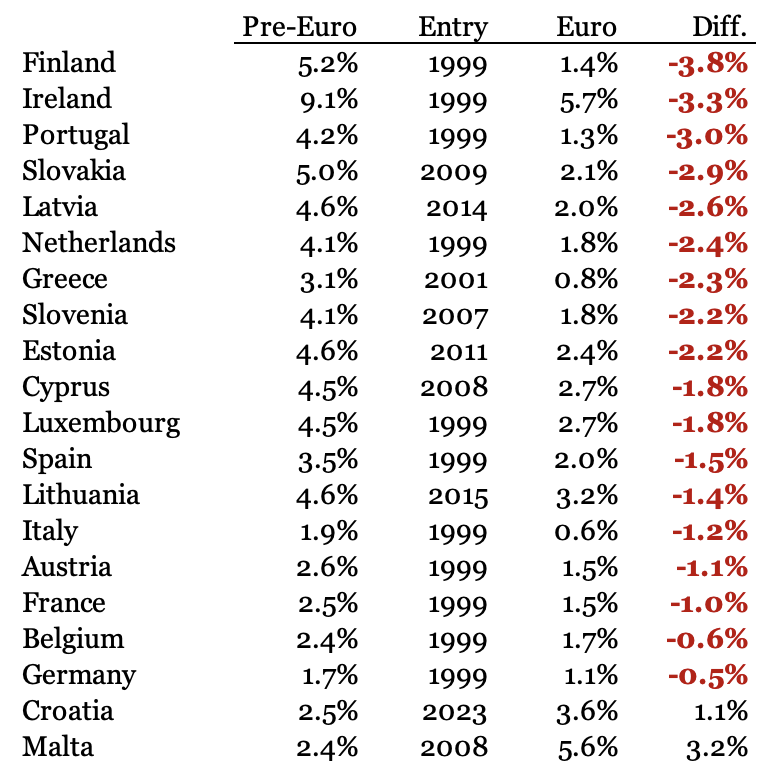

As of December last year, 18 of the 20 members of the euro zone had experienced a weakening of their economy after joining the currency area. The drop in GDP growth was substantial in many cases. Table 1 reports the real, average annual GDP growth rates between 1995 and 2025 for the members of the euro zone; the time period is divided into the years before they joined the common currency (Pre-Euro) and the years since membership (Euro).

The most striking example of lost economic growth is Finland, where GDP expanded by 5.2% per year in 1995-1998. After they replaced the markka with the euro in 1999, their economy has grown by a meager 1.4% per year:

Table 1

It does not matter when a country joined the euro zone, whether in 1999, when its 12 founding members adopted the currency, or in 2014-2015, when Latvia and Lithuania came on board. The decline in economic growth is consistent throughout the euro membership, with the exception of Croatia and Malta:

When I sat down to analyze the pattern of GDP growth for the euro zone members, I frankly did not expect such a thundering image of macroeconomic failure.

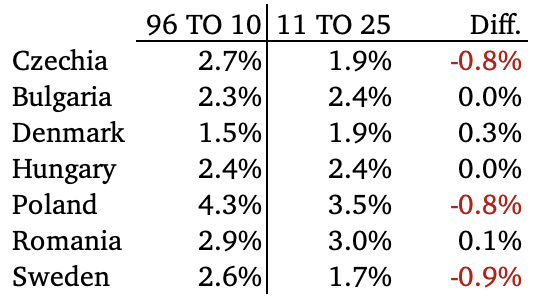

To make sure this was not a trend that cuts across Europe regardless of the euro, I controlled for growth trends in the seven EU member states that, as of December 2025, had not yet adopted the euro. (Bulgaria joined the euro zone on January 1st, 2026.) Table 2 reports a review of those seven EU states for the past 30 years; the period is split in half to identify a possible decline in GDP growth similar to what the euro zone members have experienced:

Table 2

Not only are the variations in growth small, but they also appear to be random—in other words, these economies have not been subjected to the same anti-growth treatment as the countries in Table 1 have. This point is driven home convincingly by comparing the ‘halfway’ growth period split in Table 2 to the time-wise similar experiences of

Slovakia saw a downshift in GDP growth from 5% to 2.1%, while Estonian economic growth was cut almost exactly in half.

The euro zone has turned into a club for economic stagnation. Despite its downshift in growth in Table 2, Sweden has no reason to join that club; whatever the reasons are why the Swedish economy is struggling, it does not need the extra baggage that comes with a euro-zone membership.