It does not happen often that I come across such blatant examples of economic incompetence as this report: From Grexit to Grecovery: Greece’s path out of the woods—and what still needs to be done. It discusses the aftermath of Europe’s largest post-Weimar economic disaster: the implosion of the Greek economy a decade ago.

Its authors, a team of economists at the European Central Bank, have impressive titles: one is “Deputy Head of Division for Euro-area economics,” another is “senior team lead,” a third “principal economist.” Because of their credentials and the size of the team—a total of six contributors—I started reading the report in the hopes of finding a constructive discussion about the Greek economic disaster.

I also looked forward to seeing a mea culpa from one of the institutions that destroyed the Greek economy back in the early 2010s.

I found nothing of the sort. Not with one word does the ECB report acknowledge the role that the central bank played in destroying more than one-quarter of the Greek economy. But that is not all: as I started examining the advice that the report gives to the Greek government on how to reinforce their weak economic recovery, I realized that these economists have no real understanding of the Greek economy.

Their first glaring error is to not include Greece’s recent macroeconomic history. I refuse to believe that this is a willful omission; I chalk it up instead to a competence-based oversight. If you want to understand why the Greek people are struggling to grow their economy now, you first have to understand what happened a decade and a half ago.

From 2008 to 2014—the most intense phase of the Great Recession and the ensuing austerity crisis—the Greek GDP fell by 28% in real terms. Jobs were destroyed at a faster pace than in any other post-War European economy, possibly with the exception of Sweden in 1992. At the height of the crisis, more than half of all young Greeks were unemployed. The population declined thanks to rapid emigration; in 2024, there were 1.2 million fewer Greeks living in their native country than would have been the case had the economic implosion not happened.

This is not a recession. It is a depression at best, an economic collapse at worst.

What makes their depression even worse is the fact that it was almost entirely manufactured by three supposedly reputable institutions: the European Central Bank, the European Union, and the International Monetary Fund. Together, they formed what at the time was referred to as the ‘austerity troika’ or the ‘troika’ for short. For several years, starting in 2010, they strong-armed Greece into implementing destructive austerity packages—spending cuts and tax hikes—that put the Greek economy on a rapid, highly destructive downslope into abject industrial poverty.

Now, a decade after the troika declared a fiscal ceasefire on Athens, the ECB has the audacity to publish a report where their own destructive contributions are not even worth a footnote. Instead, the authors pat the Greeks on the shoulder, suggesting that the country has

achieved a remarkable rebound in economic activity and addressed several of its key crisis legacies such as banks’ [non-performing loans], while its public debt has declined impressively.

This rebound, they claim, has happened because the Greek economy is no longer driven by private consumption, but by capital formation—business investments—and by exports. In line with a wish to strengthen GDP growth further, the ECB economists encourage improvements in the legal framework of the banking system. They also hope that Greece will see increases in labor productivity going forward.

The omission of the ECB’s complicity in annihilating 28% of a euro-area country’s economy is in itself highly criticizable. But what is even worse is the policy advice that this group of highly accomplished ECB economists gives Athens. Their conclusion that Greece needs less consumer spending and more capital formation and exports reveals a disturbing lack of macroeconomic scholarship.

Since they claim that the recovery is driven by capital formation and exports, and since they simultaneously claim that Greece fell into its debt crisis because private consumption dominated the economy, we can check their claims by reviewing some easily accessible (seasonally unadjusted) national-accounts figures from Eurostat.

Let us start with (base-year 2015) inflation-adjusted GDP growth. It was 2.8% per year in 1996-1999. Then came the euro, and Greece got access to the aforementioned price-and-risk signal distorted sovereign-debt market in the euro zone. This was part—but only part—of the reason why GDP growth reached impressive heights in the next several years:

The Great Recession began in 2008. It meant negative growth for at least part of the next four-year period, 2008-2011. However, in the very middle of that time period, right when the government in Athens is struggling to keep it all together, the austerity troika barges in like a bull in a china shop. The result is the austerity phase of the crisis—and a shrinking GDP, on average, for eight years in a row:

Things started getting better in 2016-2019, with an average growth rate of 1.4% per year. From the pandemic through 2025, the Greek economy has grown at a yearly average of 1.9%, again in real terms.

In other words, Greece enjoyed strong economic growth in the years leading up to the Great Recession. A full eight years with 4.4-4.5% real annual economic growth is remarkable for Europe, especially in view of today’s lackluster euro zone economy.

There is no denying that the Great Recession opened a big budget deficit in Greek government finances. The country fell into a debt crisis, again aided and abetted by its membership in the euro zone. The crisis would have been contained, even reversed, if Greece had been allowed to leave the euro zone.

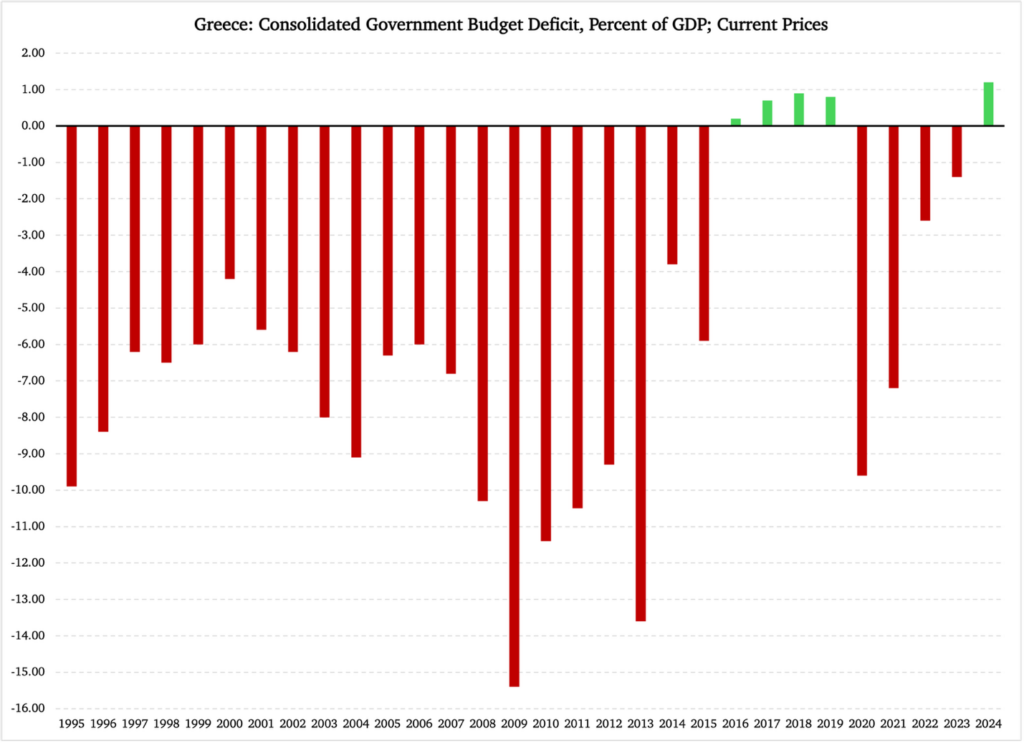

Here is what the public finance balance in the Greek economy has looked like over the past 30 years:

Figure 1

Instead of leaving the euro, Greece was run over by the ECB-EU-IMF troika. The austerity packages they forced upon Athens hit the entire government sector, and, thereby, services and other benefits that were especially important to the poor. Everything from health care and education to infrastructure and social benefits was cut. Some benefits for the poor, needy, and elderly were slashed by 50-90%.

Meanwhile, the total tax burden on the Greek economy increased by 11 percentage points of GDP. This is one of the most drastic tax hikes in modern macroeconomic history.

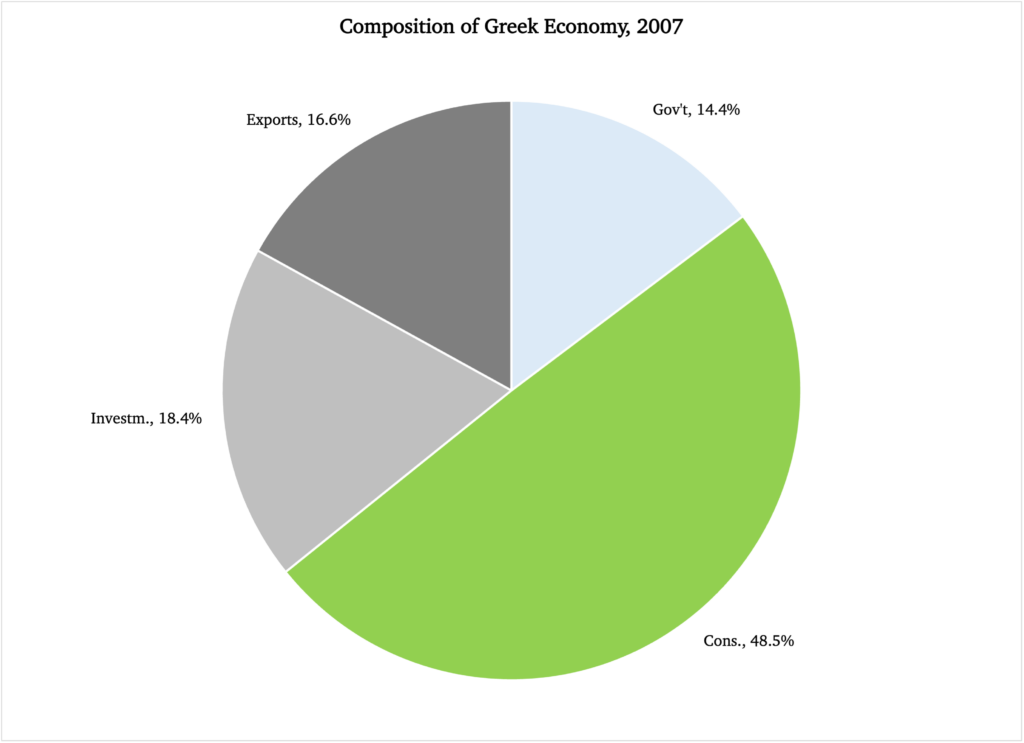

To understand the force of destruction that these austerity packages unleashed, let us have a look at the composition of the Greek economy around this point in time. Figures 2a and 2b show how big the four traditional economic activities of consumption, government spending, investments, and exports were at two points in time. In 2007, private consumption used up 48.5% of all the resources available (GDP plus imports), while 18.4% were used for investments and 16.6% for exports:

Figure 2a

According to the venerable Greek-reporting ECB economists, it was the large share of private consumption and the small shares of exports and investments that caused the debt crisis. They also claim that Greece is now recovering thanks to larger shares of exports and investments and a smaller share of private consumption.

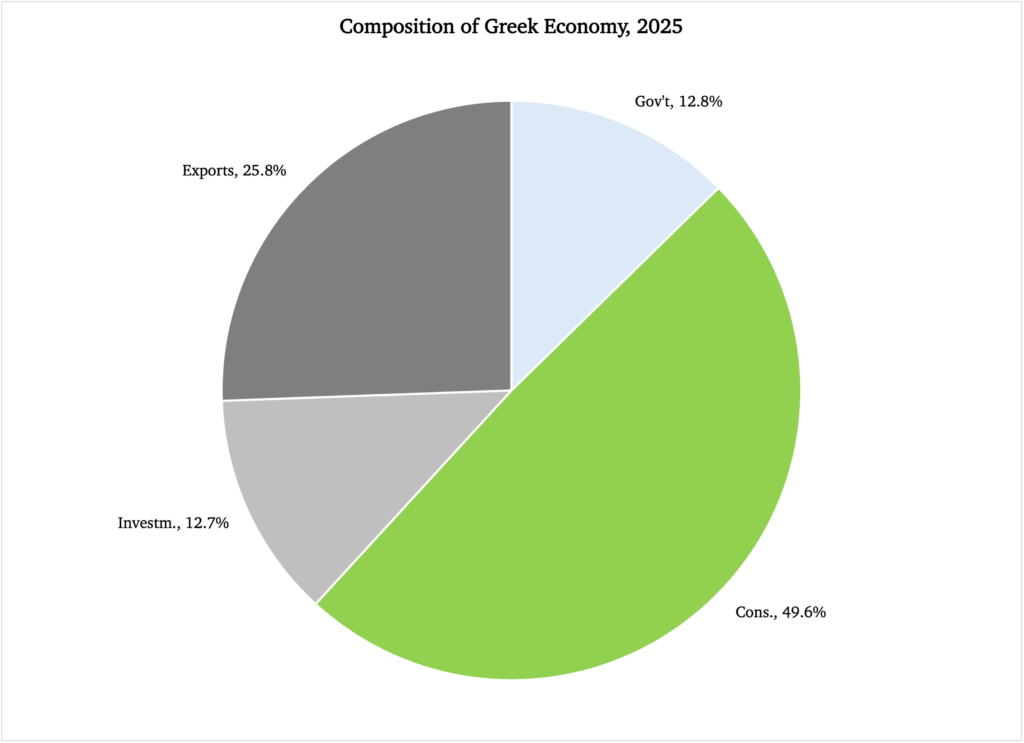

Well, let’s check Figure 2b and the same numbers from 2025:

Figure 2b

Exports are certainly more important now. Does this mean that the Greek economy is recovering thanks to growing exports?

Yes, that is possible, but under one condition: that exports exceed imports, in other words, that net exports are positive. If net exports are negative, i.e., if Greece runs a trade deficit, then their trade balance is actually a negative for their GDP growth.

According to Eurostat’s national-accounts database, Greece has run a trade deficit every year for at least the past ten years. In other words, the ECB’s Greece report is downright false in claiming that the Greek economy is recovering from its decade-and-half-long slump because of growing capital formation and stronger exports.

We should also note that capital formation accounts for a much smaller share of the Greek economy now than it did back in 2007. This refutes the ECB report’s claim that the Greek economy is benefitting from rapidly expanding investments.

So what is driving the Greek recovery?

To begin with, Greece is experiencing far less than half the economic growth today that it had prior to the Great Recession. While its GDP expanded by 4.4-4.5% per year from 2000-2007, it barely reached 1.7% per year in 2016-2025.

As slow and frail as this recovery is, it is nevertheless a recovery. It began for one simple reason: the troika finally declared a fiscal ceasefire on Athens. What the Greeks need now is peace and quiet so they can continue to rebuild their economy. They need more consumer spending, which organically will generate more investments.

The last thing they need is more bad economic advice from the ECB.