EU High Representative and Vice-President for Foreign Affairs and Security Policy Kaja Kallas (L) and EU Commissioner for Defence and Space Andrius Kubilius (R) give a press conference on the Defense Readiness roadmap at the EU headquarters in Brussels on October 16, 2025.

Nicolas TUCAT / AFP

We are watching in real time how Europe is building up its defense of Greenland. Suddenly, there is nary a mention of Ukraine in the media anymore; the governments across Europe are conspicuously less vocal on sending military units to Ukraine.

Others may speculate over the reasons for this breakneck-pace shift in strategic defense focus; if there is one thing that shines through here, it is the tightly limited nature of Europe’s military capabilities. It is almost as if Europe does not have the resources to both defend Greenland and plan to become militarily engaged in Ukraine.

Rhetorical points aside, the questions about military deployments to Greenland and Ukraine are stark reminders of another aspect of Europe’s newfound ambitions to defend itself. Europe has a formidable funding challenge ahead if it wants to materialize the dreams of military might that currently dwell in the several capitals across the EU.

As I explained back in May, European governments would have to go deep into debt in order to achieve the often-discussed goal of 5% of GDP in defense spending:

In 2023, the 27 EU member states spent €227 billion on defense. This came out to 1.3% of their total GDP. If their defense budgets had been at 5% of GDP, they would have spent €860 billion, or €378 per actual €100 in defense outlays.

The expansion would vary greatly between the member states, with a 60% growth in the Latvian defense budget and a 1,954% increase in Ireland. However, in every one of the 27 EU member states, an expansion of the defense budget is going to be the single most challenging fiscal policy issue in 2026—provided, of course, that those countries do not scrap their bold plans for building military might.

Based on my calculations from back in May, the extra debt that they would have to accumulate amounts to €653 billion. This may not seem to be very much given that, in 2024, the consolidated gross government debt of the 27 EU member states was €14.5 trillion. However, it becomes quite a bit of a challenge when we look at the annual increases in their total debt.

Over the most recent ten years, 2015-2024, for which Eurostat has detailed government spending numbers, the 27 EU states added €432.4 billion per year to their debt. However, 57% of that debt increase has actually been accrued in the last four years; in 2024 alone the EU-27 added €598.4 billion to their debt.

In view of these numbers, the increase in military spending necessitated by the 5%-of-GDP defense appropriations goal becomes an even greater challenge. Even if the 27 EU states decide to expand their defense budgets in increments—say, by one quarter per year—it still means they have to grow their annual borrowing by 25-30%.

That is no small thing to ask of the international debt market, especially since the European economy as a whole is in poor shape and barely grows at all. This makes the addition of new debt a challenge from a creditworthiness viewpoint; every billion of euros slabbed on top of the EU-27’s ‘regular’ borrowing will set in motion a rapid debt-cost increase.

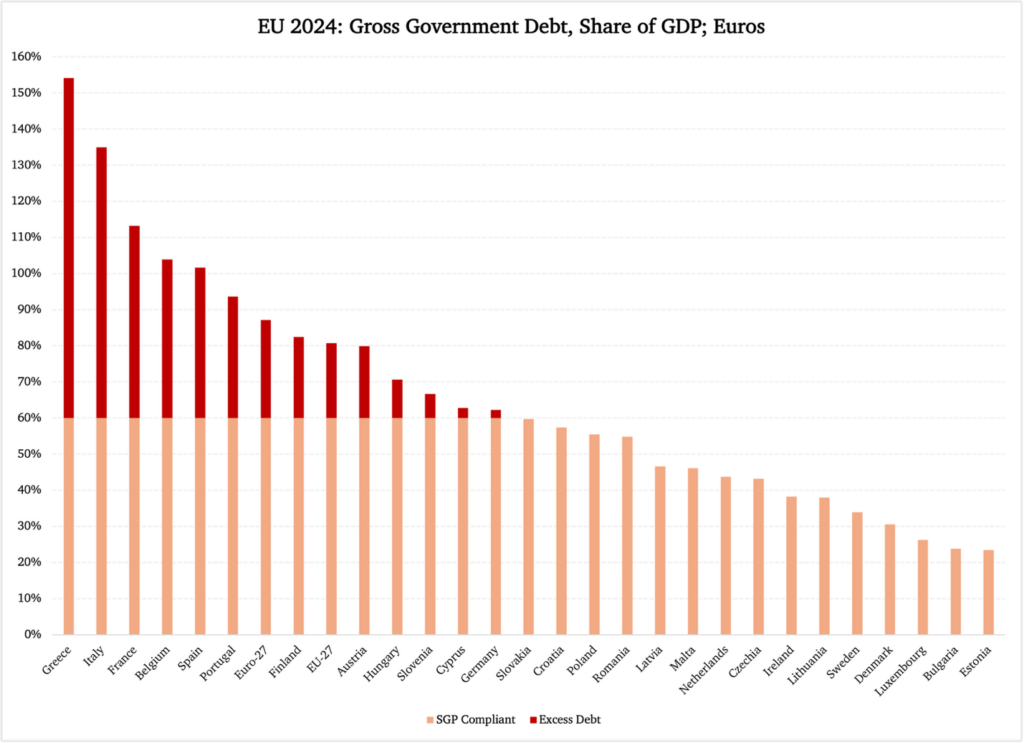

In fact, every relevant statistic speaks against the EU increasing its borrowing. To begin with the union’s own debt limit, 14 of its 27 member states currently violate the 60%-of-GDP debt limit that is enshrined in the EU’s founding documents. Figure 1 reports, with the debt exceeding the 60% limit marked in red:

Figure 1

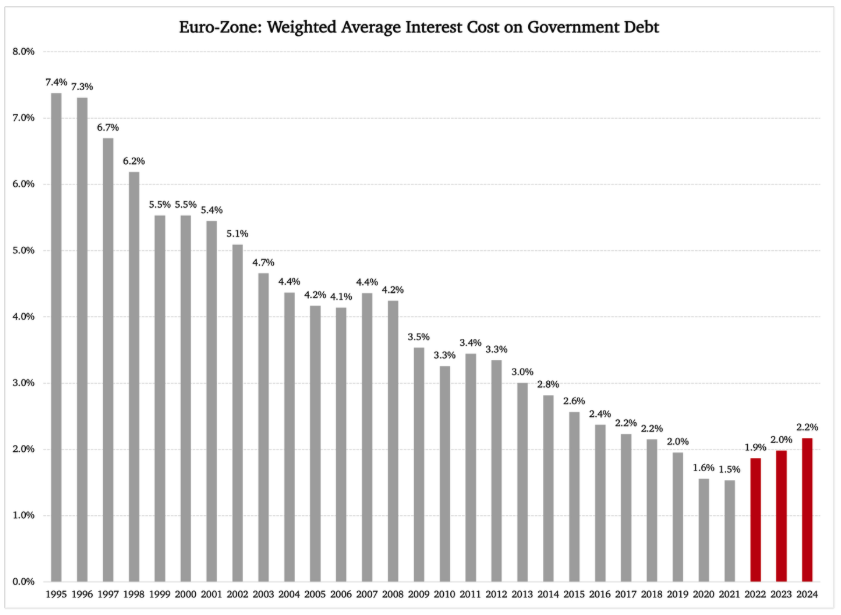

With these numbers in mind, it is difficult to see how international investors—especially large institutional ones—would want to increase their exposure to European sovereign debt. The case for European defense borrowing is not strengthened by the fact that the cost trend for the existing debt has already turned upward. After many years with falling interest costs, since 2021, the EU-27 has seen a slow but steady uptick in its borrowing costs.

Figure 2 has the numbers; we are looking at the euro zone specifically here, since there is more complete data available for that geographic area. The EU as a whole actually exhibits marginally higher costs:

Figure 2

Note the three most recent years with a rising average interest cost. This increase comes from an extremely low level, of course, but that does not make life easier for the fiscal policy makers in the EU’s indebted member states. On the contrary: the low rates they have grown accustomed to in the last several years have worked as enticements, luring them into going even deeper into debt than they otherwise would have done. They have adjusted their public finances and their fiscal policy to the premise that interest rates will remain low for the foreseeable future.

That, of course, is not the case, especially not if the EU states are going to add 25-30% to their annual borrowing.

For two reasons, there will be higher rates to pay in the future, the first being the aforementioned pressure from increasingly wary lenders who see the EU grow its debt without any plans to address the budget shortfalls.

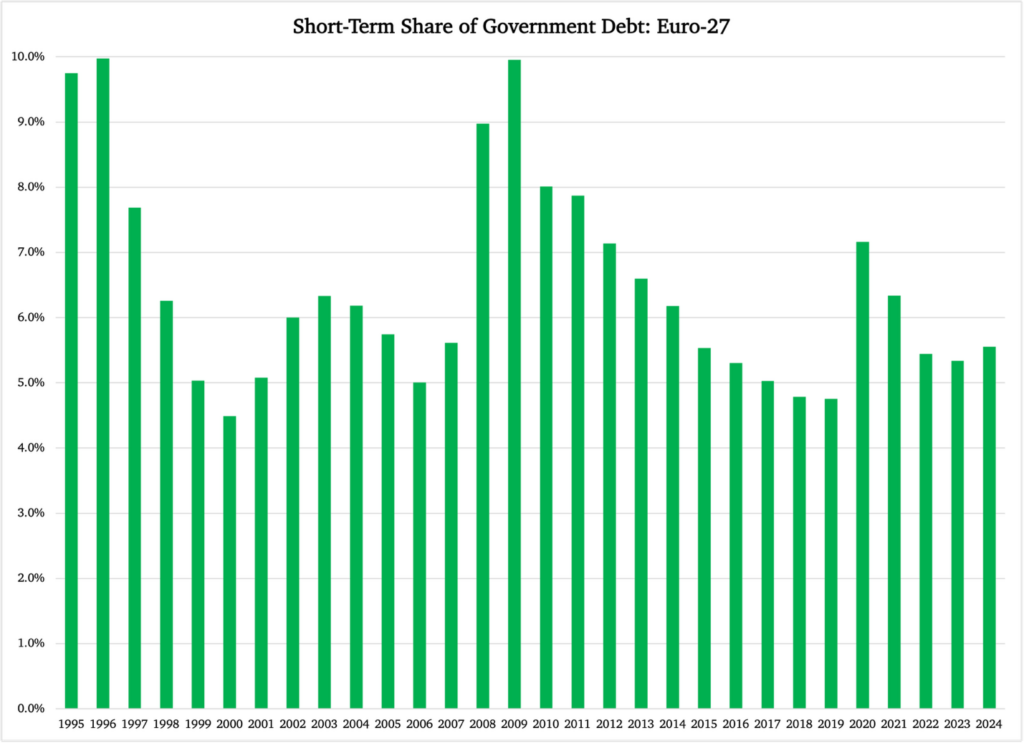

The second reason has to do with the structure of borrowing that a government under pressure has to resort to. In Europe, as well as in the United States, a rapid increase in the government’s need to borrow—‘rapid’ referring to a period of 2-4 years—is typically met with a major increase in the issuance of so-called short government debt. This debt consists of treasury bills with a maturity in the range of 3-11 months; in other words, shorter than one year.

Debt with short maturity is problematic partly because of the need to frequently renew the debt and partly because it tends to come with a high cost, i.e., high yield or interest rate, relative to that high frequency. Furthermore, every time a government has to issue new debt, its creditworthiness is reassessed by the market. The more frequently debt is reissued, the greater the risk that lenders compound bad news or problematic numbers, thus forcing compensating interest-rate increases.

Figure 3 reports how the short maturity share of total government debt in the EU has evolved over the past 30 years. There are two remarkable episodes: the sharp rise in the short-term share around the deep recession in 2008-2010 and the equally sharp rise at the time of the 2020 pandemic.

However, there is a significant difference between these two episodes:

Figure 3

After the Great Recession 15 years ago, the short-term share of total government debt in the EU fell back to its previous low levels. That has not been the case after the pandemic: on the contrary, we see a very recent increase in the short-term share in 2024.

It remains to be seen if it is going to prevail, but if it does, it will definitely add to the cost of any debt increase that the EU member states are planning. If anything, the EU could be forced to rely predominantly, even exclusively, on short-term debt by creditors who see the short-term nature of debt as an insurance policy against rising credit risks. No investor in the market for government debt wants to end up in a ‘Greek’ situation again.