There are many reasons for European taxpayers to be worried. One of them is that the debt level across the continent refuses to go down. If anything, it is slowly on the rise. Six countries have a debt-to-GDP ratio above 100%—despite relatively good economic times recently.

This does not bode well for the future. But before we get details on Europe, let us remember that America is in no better shape. On the contrary, in fact: on Friday July 26th, the U.S. government passed another sad fiscal milestone. Its total debt passed $35 trillion.

Investors in the debt market seemed to have shrugged their shoulders at this number—the yields on U.S. debt have declined in the past week—but that does not mean the political leadership should. And yet, there is nary a mention of this debt milestone along the presidential campaign trail.

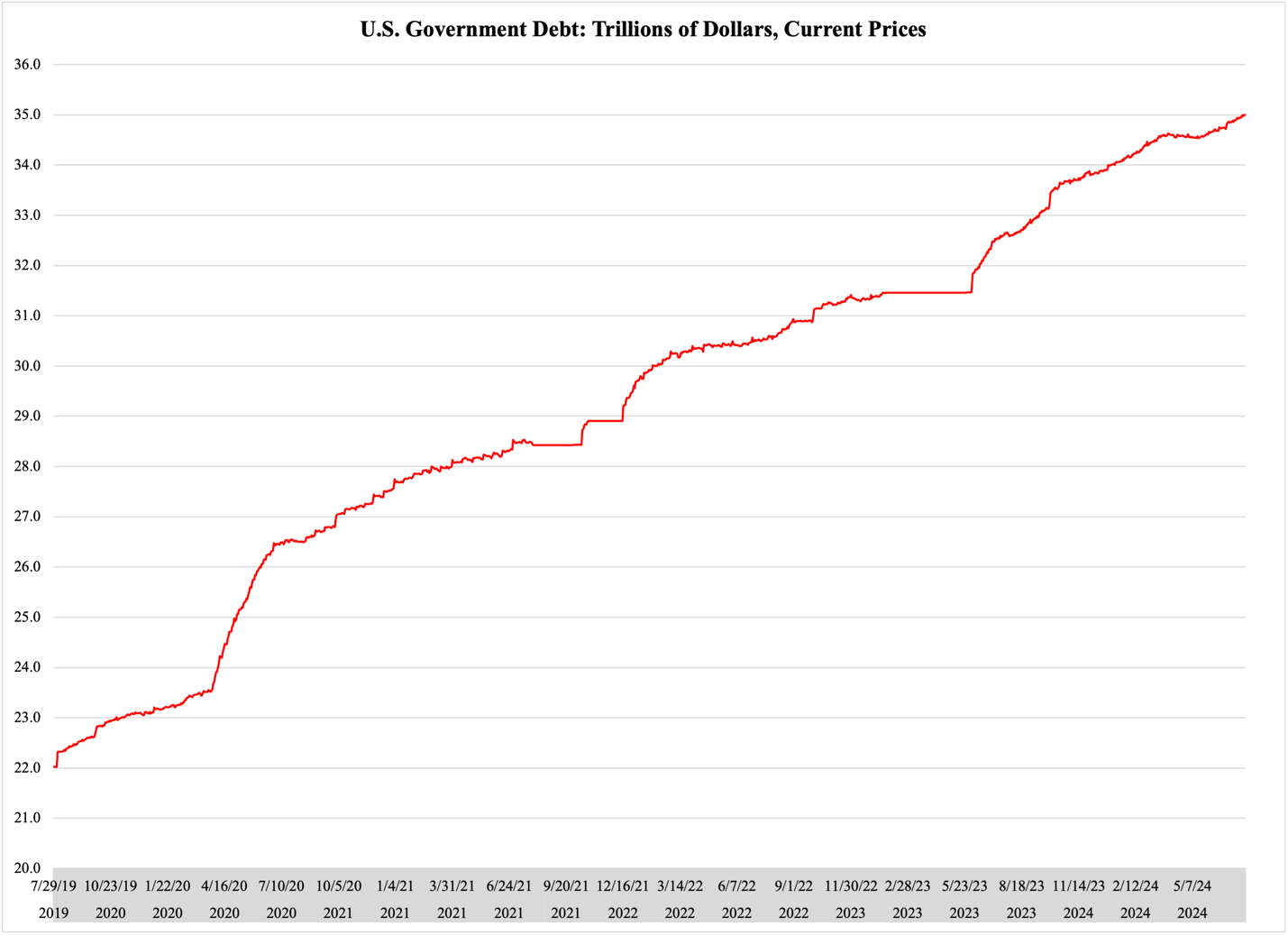

From a fiscal or macroeconomic viewpoint, the number itself does not mean anything. The message it conveys is more important from a dynamic viewpoint, i.e., from the perspective of how the debt has grown over time. Figure 1 has the story for the past five years:

Figure 1

When President Biden took office, the debt was $27.75 trillion; in 3.5 years he has presided over a 26% increase, or $7.25 trillion.

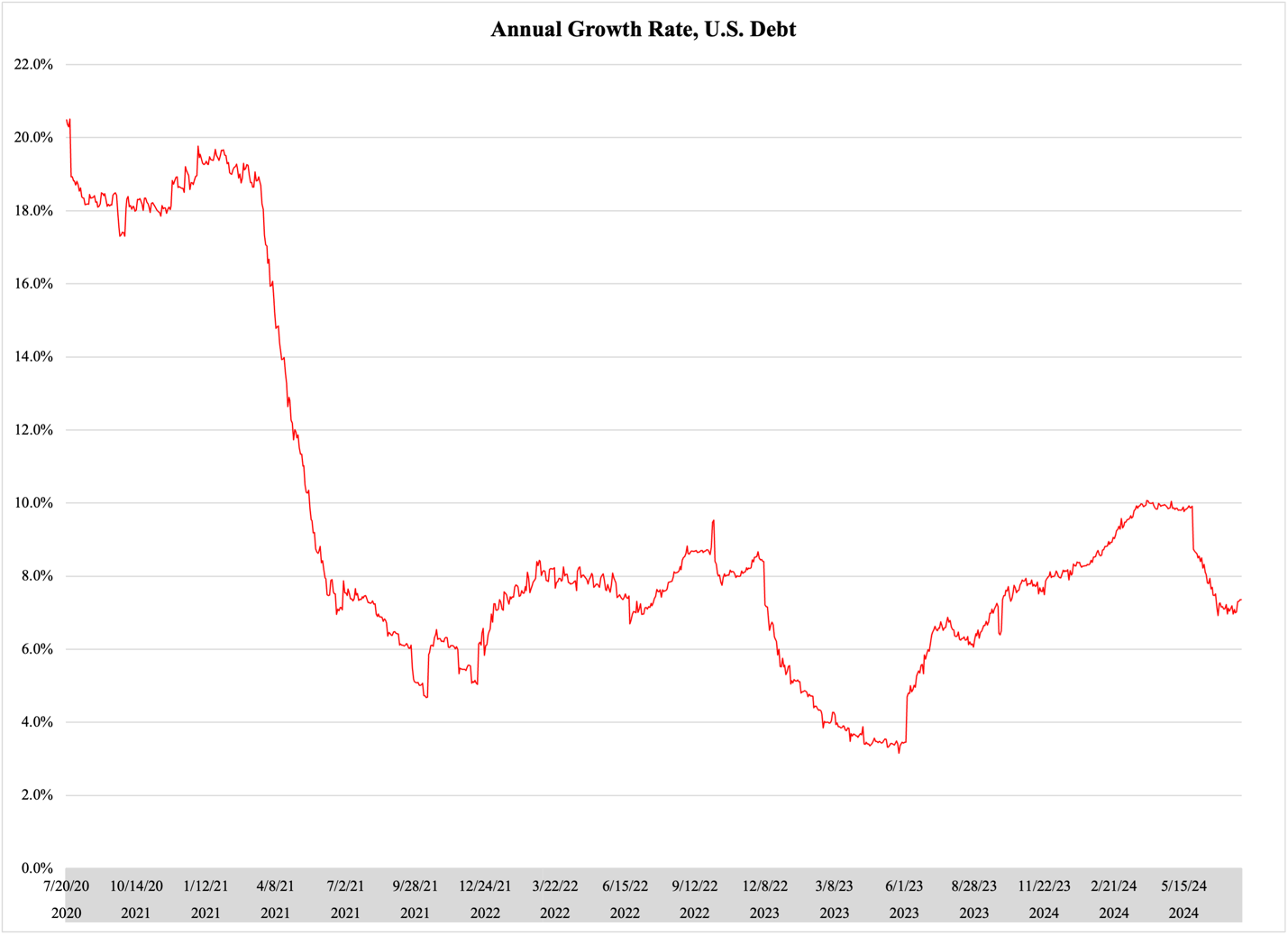

Not only is the debt growing, but the growth rate has accelerated recently:

Figure 2

The reason for the extremely high debt growth rate in 2020 is, of course, that the U.S. Congress at that time was busy spending enormous amounts of stimulus money in response to the economic shutdown that the government itself created during the pandemic. Once the rollout of that stimulus spending was over, the debt growth rate fell to more ‘normal’ levels in the 7-8% range.

Notably, there has been an uptick in the debt growth rate in 2024. It started in late 2023, at first as an increase in borrowing to compensate for the debt freeze when Congress in the spring of 2023 could not agree on a new debt ceiling. Once that agreement was in place, there was a rapid increase not only in the debt (Figure 1) but also in the debt growth rate (Figure 2).

So far in 2024, the growth rate in U.S. government debt has been 8.9%, higher than the 5.7% average for 2023. This is troubling, especially since the U.S. economy is performing well, with growth rates a hair below 3% and with employment basically at the full capacity of the workforce. Current macroeconomic conditions are such that the debt should be decelerating; in an ideal world—which is far from the one we currently live in—the debt growth rate would become negative.

In other words, there would be a budget surplus and the debt would start shrinking. That, however, is not even within the realm of the possible in the United States, at least not right now.

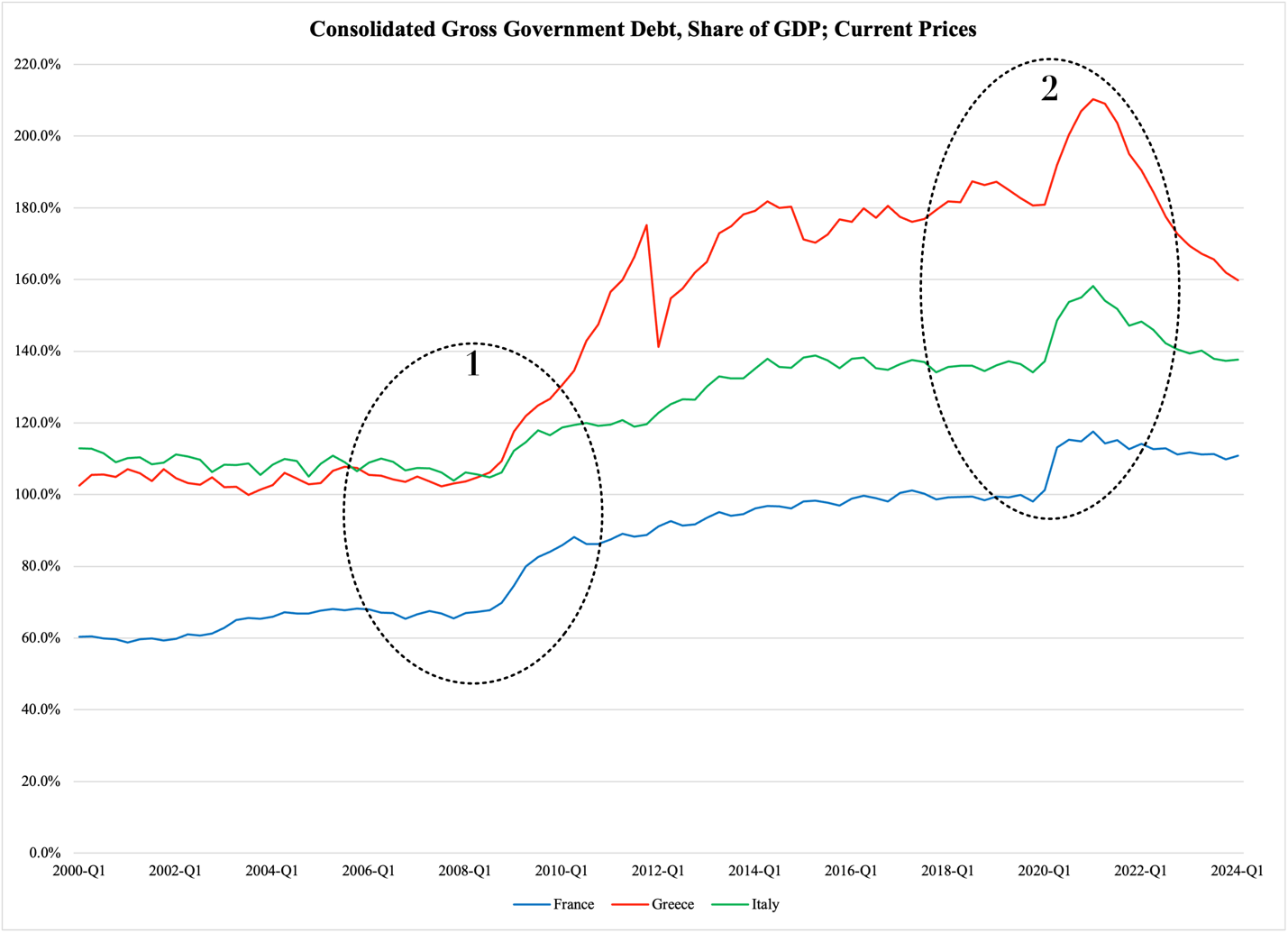

Unfortunately, the situation is not much better in Europe. Figure 3 reports the ratio between consolidated government debt and GDP for France, Greece, and Italy.* These are the three most indebted governments in the EU:

Figure 3

France, Greece, and Italy are three of the six EU states that have a government debt in excess of 100% of GDP; the other three are Spain (108.9%), Belgium (108.2%), and Portugal (100.4%).

Concentrating again on the three most indebted EU members, there is a trend in their borrowing that is a deep cause for worry—and which is never discussed in the public debate. Compare the debt hikes that happened in 2009 (Oval 1) and in 2020 (Oval 2). The latter was decidedly temporary in nature, i.e., consisted of stimulus money to keep businesses and households afloat amid the artificial economic shutdown. When that type of spending ended, the debt levels more or less returned to their previous levels. (There is an exception in Greece, which we will return to in a coming article.)

None of the same happened in 2009. A deep but economically natural—organic—recession caused a sharp rise in unemployment and widespread loss of economic activity. Most of Europe recovered relatively quickly, almost at the pace America did, but the same did not happen with the debt-to-GDP ratios.

The persistence of government debt is in itself a problem, but of greater concern is the fact that it tends to grow even in good economic times. Inevitably, this builds up to another fiscal crisis.

*) Consolidated government debt accounts for the entire public sector, from national down to local. The numbers for the U.S. refer only to the federal government, which is why no debt-to-GDP figure is reported for the American economy.