A week after Donald Trump spiced up his presidential campaign by proposing the end of the federal income tax, the market for U.S. government debt is remarkably calm. I was not expecting market turmoil as a reaction—not by any stretch—but there should have been at least a little bit of a hiccup. After all, according to current opinion polls, Trump can expect a comfortable victory in November.

Maybe the players in the U.S. debt market are not taking Trump’s proposal seriously (a big mistake), or maybe they have given up expecting serious fiscal policy ideas from America’s political leaders. Either way, the present calm and quiet feels eerily like the calm before the storm: so far this fiscal year, since October 1st, 2023, the U.S. debt has increased by $1.3 trillion. With the present monthly average extrapolated through September, this fiscal year’s deficit will reach $2 trillion.

That is a mild estimate. A more realistic one puts the final tally north of $2.5 trillion. The end of the fiscal year is normally more deficit-prone than the spring since tax filing season always comes with a surge in tax payments. At the same time, as mentioned, there is no reason for immediate worry about the fiscal fallout of Trump’s next tax reform; although he is in the lead now, it is a political eternity to the November election. Almost anything can happen between now and then.

For the longer term, though, a tax reform even close to what Trump has proposed will have a significant fiscal impact on the U.S. economy. The wisest attitude to it now is to assume that a second Trump administration will send a major tax reform to Congress within the first 100 days of taking office. If it looks anything like what has leaked out so far about his no-income-tax idea, then there will be reason to worry about the stability of the market for sovereign debt.

As it happens, the first 100 days of the next U.S. presidential administration will be about the time frame when the EU’s newfound interest in fiscal responsibility will start having tangible effects on the European economy. All other things equal, the campaign to tighten the fiscal belt across the EU should lead to lower interest rates on euro-denominated sovereign debt, while a tax reform that is expected to increase the U.S. budget deficit will push American interest rates upward.

Again, this is a long-term outlook. The calm that currently characterizes the market for U.S. government debt is mostly superficial, but it is a calm all the same. Part of the reason for this is that financial markets in general are short-sighted. This has the positive effect that they respond quickly to new information; unfortunately, it also means that they are more unstable than real-sector markets for goods, services, capital, and labor.

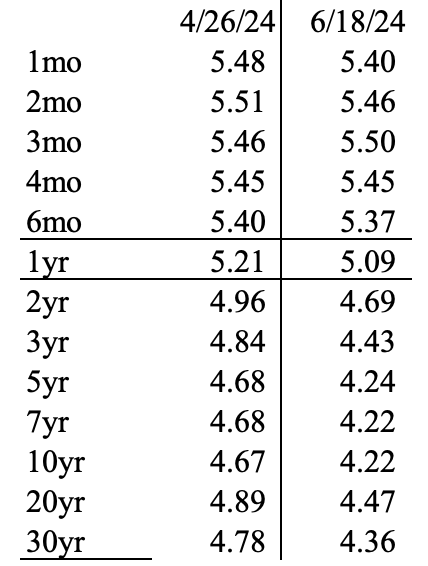

As a sign of the relative calm that currently characterizes the U.S. debt market, interest rates on longer Treasury securities have declined recently. Treasury notes and bonds with a maturity of more than a year pay less yield now than they did in mid-April. That was the time when yields stabilized after having risen from the very first days of January. A month of stability was followed by a small decline.

At the same time, there has been no decline in yields on shorter Treasury bills. The rates on securities of 2 years and more stand in striking contrast to the rates on those that mature in 1-6 months. Table 1 compares the yields on April 26th and June 18th:

Table 1

The decline in longer-term debt yields could be the result of a shift in debt issuance by the United States Treasury. Early in the year, they announced that they were going to reduce the volume sold under its bills (1-12 months), i.e., its shortest maturities, and correspondingly increase sales under longer-term notes (2-10 years) instead.

When this shift went into effect, longer interest rates began rising, just as theory says they would. All other things equal, an increased supply of debt causes the debt price to drop and therefore, the nominally fixed yield rises as a percentage of the price. We see the effect in the rise in interest rates, or yields, on the affected Treasury securities.

The 2-year Treasury note yielded 4.27% on its auction on December 26th. At that auction, investors tendered $152.7 billion while the Treasury accepted $57 billion in debt sales; the tender-accept (T/A) ratio was therefore 2.57.

In contrast, on May 28th, the Treasury offered $73.1 billion, a 28% increase over the December auction. Investors offered $170.1 billion, which is only 11% more. The T/A ratio therefore fell to 2.33; the yield, on the other hand, rose to 4.85%.

Back on December 28th last year, the Treasury sold $40 billion in 7-year sovereign debt; five months and one day later, they sold $46.6 billion. Although investors increased their tenders—in this case from $99.9 billion to $109.4 billion—the T/A ratio fell from 2.5 to 2.35. Expectably, the yield went in the opposite direction, from 3.78% on December 28th to 4.59% on May 29th.

The most recent decline in interest rates is explainable in this context. The market for U.S. debt has adjusted itself to the Treasury’s shift toward longer-term debt. In terms of quantity, this shift is marginal, not substantial, but it has had a relevant effect on the debt market. Once that effect has worn out completely, it is going to be interesting to see where the market goes next.

My bet is on gradually rising yields.