It sometimes feels pointless to sound the alarm about the bad shape of the European economy. Every time there is a new batch of data released, I see an image before me of a car stuck in mud, slowly sinking while the driver makes no effort to get out.

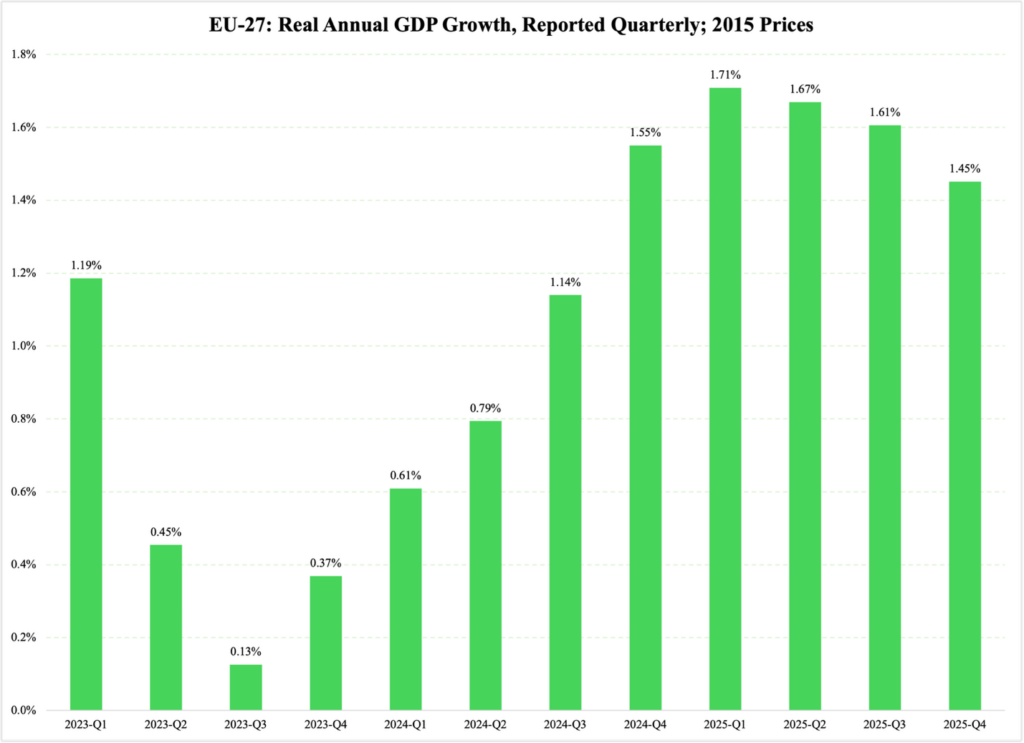

The fourth-quarter European GDP data brings out that image. I had hoped the last part of 2025 would be economically stronger, but based on the 18 countries for which Eurostat has thus far published GDP data, the EU is getting nowhere fast:

Let me be the first to acknowledge the silver linings in these numbers. One of them is that the EU growth rate is higher than the 0.5% in 2023 and 1% in 2024. But as the old saying goes, no joy lasts forever. If we break down these numbers by quarter, the picture darkens again:

Figure 1

Over the past three years, the European Union has been through the ‘peak period’ of a business cycle. That peak occurred a year ago, when the economy of the 27-member union expanded at 1.7%. Since then, GDP growth has slowly tapered off, and it has done so in a pattern that is symptomatic of an economy on its way into a recession.

Given these numbers for the ‘growth period’ of a business cycle, the very thought of a pending recession is downright horrifying. A stagnant economy is not just a problem for academics and number crunchers at the government’s treasury. It is a problem with great consequence for working families whose career opportunities erode as unemployment creeps up; for entrepreneurs whose small businesses find their markets squeezed by stagnant consumer spending; and for politicians who struggle to balance the government budget.

The last point is not to be taken lightly. Quite the contrary—the tighter the fiscal conditions get, the more we will see

In other words, a stagnant economy exacerbates Europe’s political dysfunctionality. It does so by compounding the political ailment already prevalent in countries where national governments are struggling to keep national conservative parties out of government. More governments will do so in the near future as national conservatism becomes a natural popular answer to Europe’s deteriorating political landscape.

As their economies drift into stagnation, more European governments will also have to deal with rising tensions from increasingly untenable fiscal demands. Those tensions add another conflict layer to government affairs.

The result of this fusion of ailments is a frightful Catch-22:

With all this in mind, we should also recognize the bright spots where we find them. Not all EU member states are in immediately bad shape. A small number are in fact doing exceedingly well; the economy of Cyprus grew by substantially more than 3% over the past three years. In 2024 and 2025, their exports grew at impressive rates, and capital formation increased by more than 32% from 2023 to 2025. Private consumption went up by 3.5-6% per year.

These are very good numbers, almost matched by Bulgaria, where businesses have increased their investments—capital formation—by an inflation-adjusted 7% per year since 2023. Ostensibly, this has been in anticipation of Bulgaria’s euro zone entry; if so, there will be a backlash once the stagnant effects of the euro zone make themselves known. Until that happens, though, we should congratulate Bulgarian families on expanding their private spending by 4.9% in 2024 and a whopping 8.2% in 2025 (all numbers, again, adjusted for inflation).

Poland is the third country with 3% or more in GDP growth in 2025. Their economy exhibits a balanced strength, with exports growing at 5% per year and consumer spending gradually accelerating (3.5% last year).

Sweden and Germany have ended up at the opposite end of the scale. Although the Swedish economy managed to increase by 1.7% last year, it was entirely export-driven. Businesses do not seem to be very optimistic about that country: after growing by 0.3% in 2023 and 0.1% in 2024, they climbed to a tepid 1% last year. Consumer spending is equally depressing: up 1.5% in 2025.

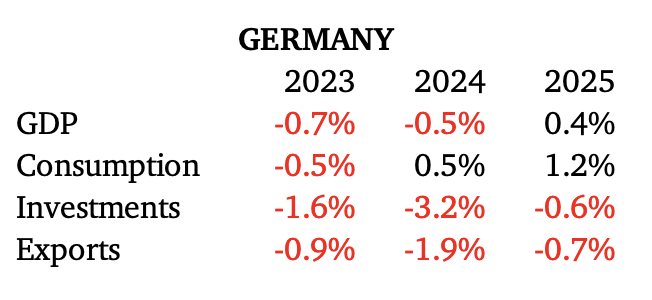

The most precarious problem, though, is Germany. No matter how you slice the largest economy in Europe, the picture looks equally bad. Table 1 has the story:

Table 1

In the third quarter of 2025, businesses invested €7.1 billion less in fixed prices in the German economy than they did in the first quarter of 2023. That is a 4.3% drop in less than three years—in constant prices.

If, since 2023, business investments in Germany had grown at the same impressive rate as in Poland, there would have been some €126 billion more in capital formation over the past three years.

At a time when there is much talk about a more cohesive Europe, the economic performance of the continent points in the very opposite direction. As if dysfunctional national governments were not enough, there is no help to be expected from Brussels. Despite fanfare to the contrary, the EU has lost its ability to provide the continent-wide leadership that it was entrusted with when the European Union was founded.

One Response

Capitalism would cure Europe’s problems. Reduce government, allow people to invest in property. Reduce taxes and regulations. Create less dependency on government. Reject Socialism, Communism, Islam and any other oppressive leadership. Educate people so they know how to vote to insure their freedom and basic human rights.