The question is not whether Leo XIV has spoken well. It is whether the institutional architecture exists for any temporal authority to answer, and whether any European institution has been authorised to ask the anthropological question the encyclical raises.

When you analyze economic policy in America and in Europe, it is important to understand the cultural differences in how policymakers address difficult situations. While the American approach is to be as blunt as possible, the European strategy just as often balances between convoluted messaging and outright denial of facts.

On April 30th, we saw a glaring example of the latter. The European Central Bank announced its most recent monetary policy decision:

The Governing Council today decided to keep the three key ECB interest rates unchanged. While the incoming information has been broadly consistent with the Governing Council’s previous assessment of the inflation outlook, the upside risks to inflation and the downside risks to growth have intensified.

This is fancy speak for the ECB expecting higher inflation and slower economic growth. It is also a thinly veiled hint that the central bank is worried about Europe sliding into stagflation. A stand-still economy is an economy with high unemployment; a stand-still economy with high unemployment that also experiences higher inflation is an economy in stagflation.

In other words, when the ECB expresses worries about both “upside risks to inflation” and “downside risks to growth,” it is writing the word ‘stagflation’ all over the euro zone. At the same time, the central bank refuses to use the term in the announcement of its policy decision: while the term ‘inflation’ is used 13 times, ‘stagflation’ is not mentioned once.

If there were no statistical evidence of looming stagflation, the ECB’s silence on the matter would make perfect sense. But the statistical evidence is not absent—it is very much present. To begin with, the annual inflation rate for the euro zone has increased from 1.7% in January to an estimated 3% in April. This is a sharp rise that should have merited an interest-rate hike by the ECB.

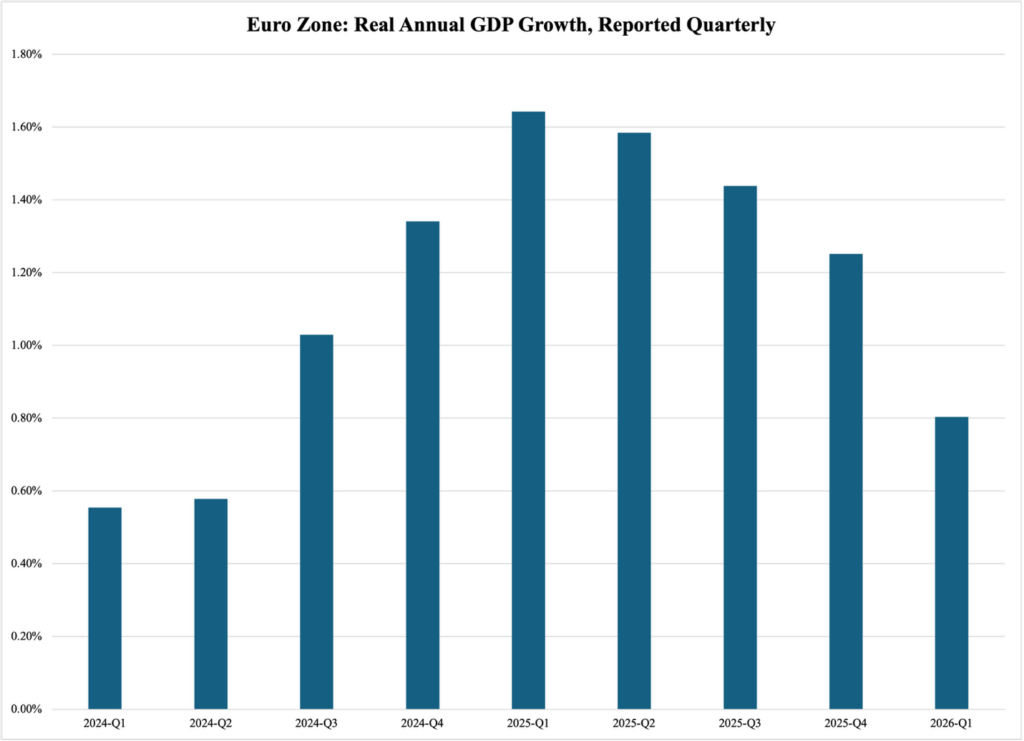

Furthermore, euro zone GDP growth has slowed markedly over the past year. It has fallen by more than half, from 1.6% in the first two quarters of 2025 to a microscopic 0.8% in the first quarter of 2026:

Figure 1

Source of raw data: Eurostat

This pathetic growth rate is a key contributor to the euro zone’s persistently elevated unemployment rate a couple of ticks above six percent. The comparable U.S. jobless figure is consistently two percentage points lower. Since the U.S. economy regularly outgrows the euro zone GDP by 2-2.5 percentage points (adjusted for inflation), it is obvious that the higher European unemployment rate is closely tied to its endless economic stagnation.

In other words, with rapidly accelerating inflation, a standstill economy, and persistently high unemployment, the euro zone is not only on the doorstep of stagflation—it is already dipping its toes into it.

To make matters even worse, the euro countries are already exhibiting stagflation-like characteristics, where high inflation and high unemployment go hand in hand.

In March,

In a normal economy, the relationship between inflation and unemployment would be the opposite: high inflation would be paired with low unemployment, and vice versa. Under exceptionally good economic conditions, an economy can even couple low inflation with low unemployment.

At a time when the euro zone is increasingly suffering from high rates of both inflation and unemployment, I would have expected more from the ECB than a stalwart strategy of stagflation denial. Their policy decision became even more questionable when President Lagarde, in her press conference on April 30th, gave this answer to a reporter’s question about the prospect of euro zone stagflation:

It’s quite popular to talk about stagflation, and it flags a lot of anxiety and all the rest of it. I think we have determined that stagflation is the right characterization of what happened in the seventies. But from our perspective, we think it is better to park it in the seventies, given the facts that we have at the moment. You know, it’s a completely different situation.

It is irrational of Lagarde to try to pretend that stagflation can never happen again. It is irresponsible of her to do so when the trends in the relevant statistical variables point toward stagflation, not away from it.

The ECB’s refusal to recognize the stagflation risk becomes downright problematic since, at the same press conference, Lagarde reveals that the policy-making body at the ECB discussed raising interest rates in response to adverse economic data. This shows that the central bank is very well aware of the stagflation threat.

So why this denial? The only explanation I can find is in one word in the first sentence of her response to the reporter’s question: anxiety. As banal as it seems, the ECB’s fear of the term ‘stagflation’ might simply emanate from a worry of the public’s reactions to it. It is possible that the ECB reasoned as follows: ‘If we confirm that there is a risk of stagflation in the coming months, businesses and households may let panic take over.’

While understandable, this kind of psychological assessment does not exhibit policy leadership. A central bank is supposed to be a policy leader. If its analysts determine that bad news is on the horizon, it is the central bank’s duty to present the bad news to the general public.

The alternative is to deny reality until it no longer allows itself to be contained. At that point, though, when people realize that they were given no warnings about a coming economic crisis, despite the ECB being aware of the looming threat, the central bank could suffer an existential crisis of confidence. I would hate to elaborate on what the ramifications of such a crisis could be.

In fairness to President Lagarde and the ECB’s Governing Council, her worries may also be related to the fact that there is very little the bank can do about stagflation. It cannot stimulate the economy by lowering interest rates: although such rate cuts theoretically reduce unemployment, they also reinforce inflation.

The central bank could raise interest rates, just as Lagarde revealed they discussed at the ECB’s policy meeting. Over time, higher interest rates do have a dampening effect on inflation, but by making household and business credit more expensive, they also make the unemployment situation worse.

In a blunt American manner of speaking, stagflation neuters the central bank. It takes a dedicated fiscal policy intervention to bring the economy back to full employment and price stability.

Again, it is understandable if President Lagarde is reluctant to admit that Europe might be heading into a situation where her policy-making institution would end up stripped of its policy-making powers. However, such concerns are overridden by the ECB’s responsibility to be a policy leader, especially when tough economic times are looming on the horizon.