A scathing U.S. House of Representatives subcommittee report backs a probable laboratory origin for COVID-19, finds no quantitative basis for the six-foot rule, and argues that officials overstated the vaccines’ ability to prevent infection and transmission.

The American economy is leaving Europe behind. It is happening in real time, and nothing can stop it. America has chosen the future; Europe has chosen its own demise.

This is not just a slogan. It is the cold, hard truth visible in stack upon stack of economic statistics. The fact that Europe’s political leadership remains blind, deaf, and willfully ignorant of the economic decline of their continent is one of history’s many self-imposed tragedies.

Few numbers are as devastating to a nation’s economic self-image as foreign direct investment (FDI). A month ago, I reported on the briskly paced industrial decline in Germany. This trend is not limited to domestic investment—it also includes FDI.

My report compared two statistical sources, finding a common trend that spoke with unnerving clarity of the unending German—and by extension European—economic malaise. One of the sources, the annual World Investment Report published by the UN trade agency UNCTAD, explained that in 2024,

FDI fell in more than half of EU countries, with sharp declines in Germany (-89%), Spain (-39%), Italy (-24%) and France (-20%).

We now have even newer data that corroborates the European freefall. The latest release of FDI statistics from the U.S. Bureau of Economic Analysis shows a decline in American investments in the German economy for five consecutive quarters. The U.S. FDI in Germany increased in the last quarter of 2025 and in the first quarter of this year, but from very low levels.

A similar trend applies to the European continent as a whole: in Q1 of 2026, American businesses invested more in Latin America and the Caribbean than in Europe.

Although FDI figures can fluctuate significantly from one quarter to the next, the long-term trends in Europe and North America are clear and steady. While Europe is suffering, America has become a global investment magnet.

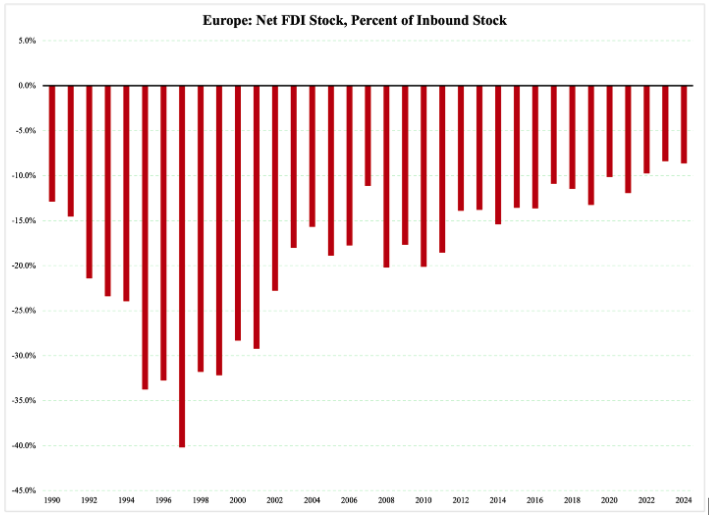

Figures 1 and 2 put this contrast on full display. Figure 1 reports the FDI balance in Europe, a balance that is calculated as follows. The difference between

is divided by the foreign-owned capital stock in Europe.

Suppose foreigners own €1,000 worth of businesses in Europe. Suppose also that Europeans own €800 worth of businesses outside of Europe. The difference is €200. We divide that by €1,000 and get 20%. This is the ‘stock balance’ of foreign direct investment. It is a good balance because it shows that more FDI money has come into Europe than has gone out.

If, on the other hand, the balance is reversed, so that Europeans have invested €1,000 abroad but foreigners have only invested €800 in Europe, then we get an FDI stock balance of -20%. A negative number means that the rest of the world is not as interested in Europe as Europeans are in the rest of the world. Europe is not a very attractive market for global investment capital.

This is exactly what Figure 1 tells us:

Figure 1

Although the FDI imbalance has declined somewhat over time, it shows no real signs of ever reaching zero, let alone switch into the positive.

From 2022 to 2024—the last year for which UNCTAD has published data—both stocks of FDI have declined on average. Europeans have reduced their investments outside of Europe, and non-European investors have reduced their investments in Europe.

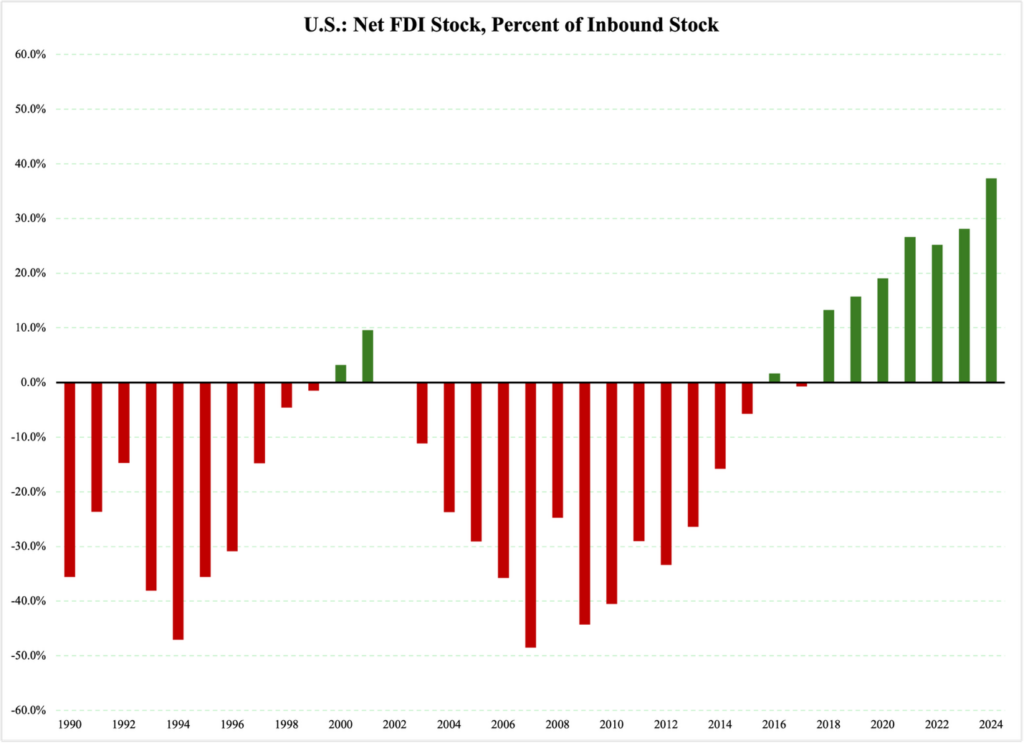

It is not surprising that Europe is having trouble attracting investors, nor is it surprising that America is an FDI magnet. Figure 2 reports the same numbers as Figure 1, but this time for the U.S. economy:

Figure 2

Before 2010, the U.S. economy exported jobs and FDI, primarily to China, Canada, and Mexico. That trend began reversing after the 2008-2010 Great Recession, revealing itself in a shrinking FDI stock deficit. This trend accelerated and morphed into an FDI surplus during President Trump’s first term: his tax reform drastically cut the corporate income tax and in other ways made investments in the United States considerably more favorable.

The result was a sustained positive trend in the FDI stock balance.

The aforementioned UNCTAD report shows a sharp rise in FDI going into the American economy in 2024. Using the more recent figures from the Bureau of Economic Analysis, we can compare four-quarter averages for the past couple of years:

One big reason for this foreign interest in investing in America is a business-friendly, forward-looking legal, financial, and political environment, especially when it comes to artificial intelligence. A recent report by the bank Morgan Stanley shows AI-directed investments in the United States nearly doubling this year to $570 billion—and doubling again in 2027 to top $1 trillion.

A rapidly growing portion of that investment money is coming from abroad. Multi-year investment commitments from abroad are directing hundreds of billions of dollars every year in new FDI funds to the U.S. economy.

The contrast between Europe and America is too sharp to ignore. It is time for European policymakers to fundamentally rethink their approach to economic growth, capital formation, jobs creation, and free enterprise.

When the common-currency euro zone was created a quarter century ago, there were hopes that a more efficient, highly integrated, and seriously business-friendly new Europe would emerge. That has not happened; if anything, the EU and the euro area have become less friendly to businesses.

If Europe wishes to rebuild its prosperity and to have every generation grow up to a brighter future than their parents had, the time for a fundamental shift is now: away from the focus on government as the center point of the economy and onto a path of economic liberty and entrepreneurial dynamism.