On May 21st, Germany’s news agency Wirtschaftswoche reported on a troubling new study from Ernst & Young (EY), a highly respected consulting bureau. The study unveiled scary figures on the decline in foreign direct investment projects in Germany. Last year, the number of such projects

fell by ten percent to 548 projects in 2025 compared to the previous year. It is the eighth decline in a row and the lowest level since 2009. “This is an alarm signal for Germany as a location”, said the head of EY in Germany, Henrik Ahlers

His verdict on the German economy did not mince words:

“In Germany, the high tax burden, high labor costs, expensive energy and at the same time a paralyzing bureaucracy are slowing down investment events”, said Ahlers. Word of Germany’s “inability to reform” has now spread around the world. “Unfortunately, not much remains of the image as a strong quality location and economical rock in the surf.”

This is not the first study to depict a Germany in industrial decline, but it is one of the most frightening of its kind. Since it counts the number of investment projects, it is as close to reality as one can get in a report like this.

But wait—is this really bad news for Germany? The EY study does not look at the value of the investment projects; is it, therefore, not possible that foreign investors are shifting strategy—from many relatively small projects to fewer, larger ones?

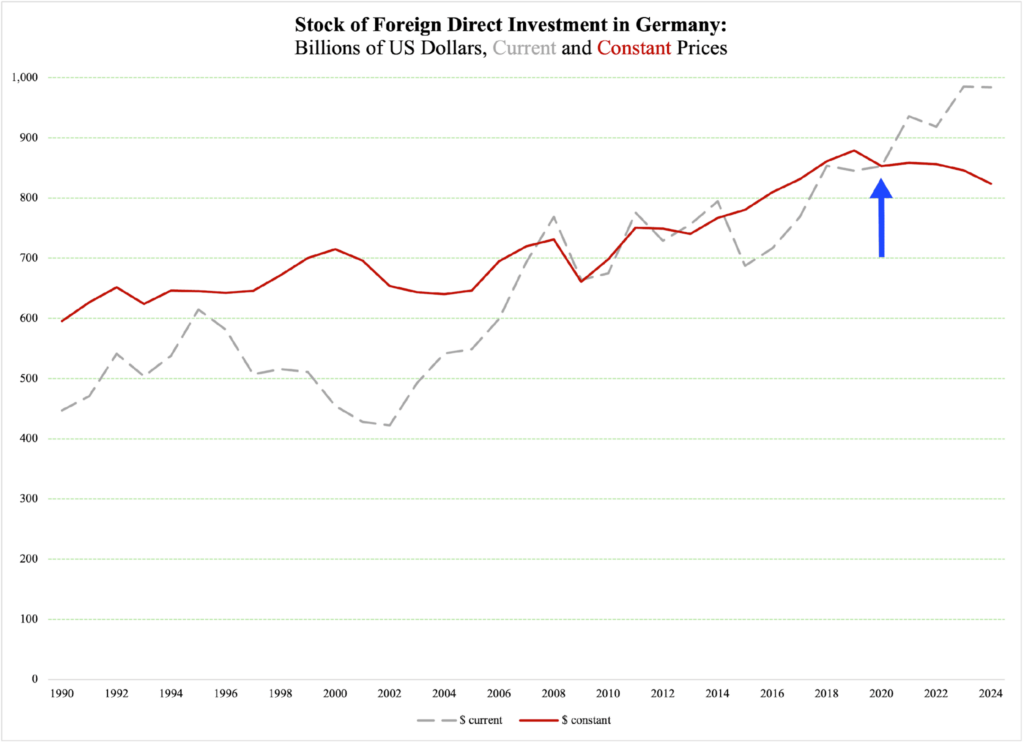

To check for this, we need to review international data on foreign direct investment. Before we do that, though, let us take a look at what capital formation in general looks like in the German economy. Figure 1 presents the volume of gross fixed capital formation, which in practice means the amount of money businesses spend in order to maintain and expand their productive capital stock. While the nominal value in U.S. dollars has kept increasing (the dashed gray line), the inflation-adjusted value (red) peaked in 2019 and has been in decline since then (blue arrow):

Figure 1

The decline in the inflation-adjusted value of general German capital formation is a clear affirmation of the findings on declining FDI presented by the Ernst & Young report. After 2019, when businesses invested to the tune of $878.7 billion, there was a 6.3% decline until, in 2024, total investments amounted to an inflation-adjusted $823.6 billion (all in 2020 prices).

In other words, the inflation-adjusted value of investment in general has declined in Germany in recent years.

To find out more about foreign direct investment (FDI), we utilize the excellent database maintained by the UN’s trade agency, UNCTAD. They only report FDI data in current prices, so we cannot immediately compare those numbers to the ones reported in Figure 1. However, I will convert them in a moment.

According to UNCTAD, Germany was home to a stock of foreign direct investment worth $1,209 billion in 2024. Ten years earlier, that FDI stock was worth $860 billion, which means an increase of $350 billion over ten years.

Broken down by year, this means a 4% annual growth in the value of Germany’s FDI stock. This is a respectable number, which can easily lead us to conclude that the EY report is just another alarmist call for attention. However, when we remove inflation from the FDI figures, we see that this is not at all the case. Suddenly, the FDI stock increase shrinks to 1.25% per year—a much more humbling number that lends some credence to the EY report.

We now narrow down the focus further, limiting ourselves to the period 2020-2024, during which, as Figure 1 shows, inflation-adjusted capital formation in Germany has been in steady decline.

The same is true about the FDI stock: foreign investors have reduced their contributions to that stock—in short, their investments—to the point where the FDI stock loses 1.2% of its value from 2020 to 2024.

In other words, the EY report about a declining number of FDI projects in Germany is accompanied by a real decline in the value of those same FDI projects.

This is not the kind of stuff you are supposed to see in one of the world’s most advanced industrial economies. This is the kind of decline that happens in developing countries with unstable governments, shaky judicial systems, unpredictable regulations, and problems with energy supply and workforce reliability.

To be fair, many other countries in Europe are also struggling with retaining FDI—Sweden is one of them—but no other European nation has made such a conspicuous swing from magnet to repellant. No other European country can boast a similarly strong history of using regulations, legislation, and overall economic policy to promote the growth and evolution of an economic superpower—only to turn around on a dime and let the entire economic machinery fall apart, screw by screw, bolt by bolt.

Let me be clear about what is going on in Germany. When businesses scale back their investments, they do less to grow and even maintain the productive capital they have in a country. This means stagnant production, in terms of quality and eventually also in quantity. When a corporation has factories in multiple countries, it prioritizes investments based on where it can get the most return on expanding capacity, improving quality, and increasing productivity.

The decline of German capital formation tells us that corporations, big and small, have concluded that the prospects of a positive return on investments in Germany are shrinking rapidly, or even that they have disappeared entirely. Corporations—once the backbone of the German economy and the unstoppable engines of prosperity—have woken up and smelled the coffee.

Germany is in a state of industrial decline. As shocking as this conclusion is, there is no other way to characterize what the numbers tell us. There is also plenty of anecdotal evidence; in a recent article, I exemplified the German deindustrialization trend with an analysis of the sorry state of Volkswagen. There are countless other examples, all of which add up to an inevitable decline in capital formation.

I have discussed the economic reason for Germany’s decline in other articles; there is also a political reason, directly tied to the Merz government’s obsession with keeping AfD out of any political influence. By forming a government whose only common denominator is a fervent hatred for another party, Chancellor Merz has deadlocked the legislative process to such a degree that it is incapable of producing forward-looking policy.

Bluntly speaking: Germany has a government that guarantees that no reforms will be implemented to stop the industrial decline that fuels the political shift that the chancellor wants to stop with his governing coalition.