A scathing U.S. House of Representatives subcommittee report backs a probable laboratory origin for COVID-19, finds no quantitative basis for the six-foot rule, and argues that officials overstated the vaccines’ ability to prevent infection and transmission.

Eurostat, the statistical agency of the European Union, has published numbers on GDP, economic growth, and related variables for the first quarter of this year. As usual when it comes to national accounts data for Europe, it is overall a depressing read. Adjusted for inflation,

Another striking message in these numbers is that Europe is splitting into a two-tier economy: a smaller group of countries are pulling away in terms of growth and capital formation, while a larger group is sinking deeper and deeper into stagnation and industrial poverty.

Before we get to the individual economies, let us first briefly examine the aggregate numbers for the EU and the euro zone. It has been 3.5 years since the European economy expanded by 2% or more; back in the third quarter of 2022, GDP for the EU expanded by 2.9%. It was a solid number back then, but, in retrospect, that was not a ‘normal’ growth rate. Instead, it was a lingering effect of the rebound from the 2020 pandemic-related artificial economic shutdown.

To be fair, though, the EU, and even more so euro zone figures, are affected by a statistical anomaly: the Irish economy. Due to its very special setup as a domicile for foreign corporations, and therefore as a pass-through for corporate finances, the Irish GDP swings wildly in ways that more traditional economies don’t. For example,

To use an American idiom, such swings are ‘out of whack’ and have disproportionate effects on aggregate figures like the GDP for the entire euro zone. That does not mean the long-term trend of 1-1.5% real GDP growth for the EU is wrong; what it means, though, is that we should be a bit careful when we interpret growth figures for single quarters.

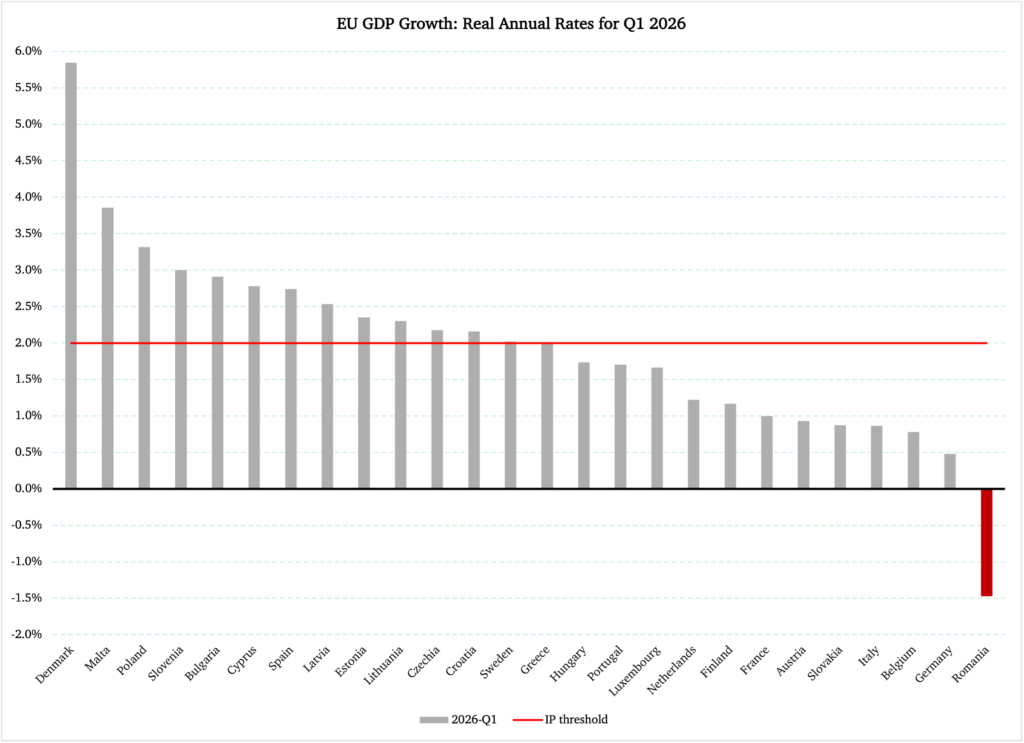

We should also examine how the individual member states are doing. Figure 1 does just that, but in order to avoid the extreme Irish swings, the green island is excluded from this single-quarter picture.

The red line represents the 2% real growth rate, which is significant in understanding the long-term strength of an economy.

Figure 1

At 2% annual growth, an economy is able to reproduce its population’s standard of living over time. If an economy persistently grows at a lower rate than that, every growing generation will, simply put, have to work harder than their parents’ generation to achieve the same standard of living.

Although it is never good when GDP growth dips below 2%, there is no material risk for generational losses of standard of living as a result of occasional growth figure dips. The problem arises when GDP stays below 2% per year over an extended period of time—in my original analysis of this phenomenon of industrial poverty, I suggested ten-year averages as the benchmark.

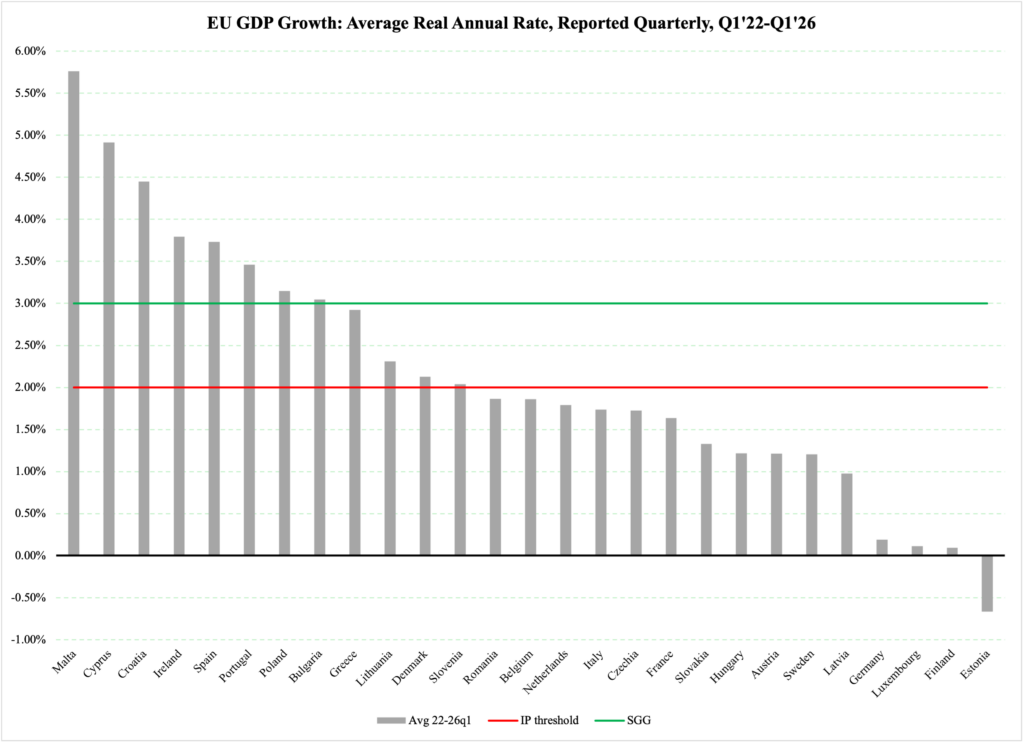

We are not going to go that far today. For now, a look at the post-pandemic years will give us a good idea of where Europe is headed. Figure 2 reports the real, annual GDP growth rate for all the 27 EU members. Since this is a longer average, the outrageous swings in Ireland’s GDP are evened out.

Figure 2

With 15 of the 27 member states below 2% on average, it is fair to say that the European Union is in a state of economic stagnation. The 12 states that have enough growth to improve their economic well-being over time are not always comfortably above the 2% threshold:

Eight of the remaining nine countries climb above 3% per year, a rate that represents a high, reliable degree of economic resilience and progress. The individual growth rates of the nine range from 2.9% in Greece all the way up to Malta’s 5.8% per year. While their reasons for having a stronger-growing economy vary, these nations show that economic stagnation is not a given—it is the result of choices in terms of tax policy, the size and scope of government spending, and regulations on important industries and markets, e.g., energy and the labor market.

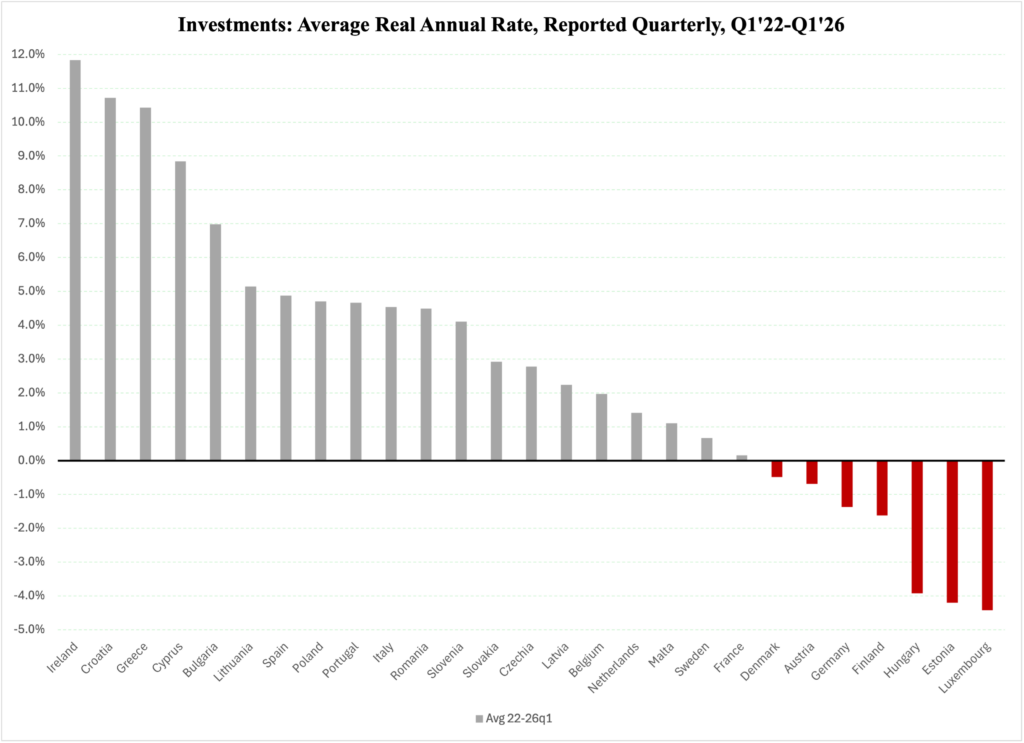

The long-term ability of an economy to grow depends in large part on how committed businesses are to investing there. The formation of productive capital usually only contributes 17-20% of GDP, but it does not need to be greater than that in order to set the pace for the future of an economy.

Unsurprisingly, the four EU member states with the highest rate of business investments over the post-pandemic period are also among the 12 reported in Figure 2 with the higher than 2% real GDP growth.

Figure 3

Overall, the European economy refuses to move forward at anything that resembles healthy, respectable growth rates. The exceptions attract business investments and therefore seem to offer a more future-oriented economic climate than other EU members; it would make sense for legislators in the most growth-challenged countries to look at their better-performing peers for lessons to be learned.

Each country has its own challenges, but they all have in common that they defy, to a larger or lesser extent, some simple, fundamental economic principles: lower taxes are better than higher; a smaller government is better than a bigger one; fewer regulations are better than more regulations; and law and order is preferable to high crime.