The European Parliament voted to open negotiations on the most ambitious monetary project in Europe since the creation of the euro—without any independent body having examined whether the ECB had the Treaty authority to propose it in the first place.

Sometimes, big news comes in small packages. Two decisions by two different central banks—normally news that only dedicated policy wonks would pay attention to—in combination paint a grim, dramatic picture of the future of the European economy.

The first central bank decision was that which the Governing Council of the ECB made on June 11th, when it kept its policy-setting interest rates unchanged:

The Governing Council is committed to setting monetary policy to ensure that inflation stabilises at our two per cent target in the medium term. In line with this commitment, we today decided to raise the three key ECB interest rates by 25 basis points.

They motivated the decision with the Israeli-U.S. war on Iran, which “is generating inflation pressures” on the euro zone economy. In reality, there is quite a bit more drama behind that decision, drama that became clearer when, six days later, the Federal Reserve decided to keep its policy-setting federal funds rate unchanged.

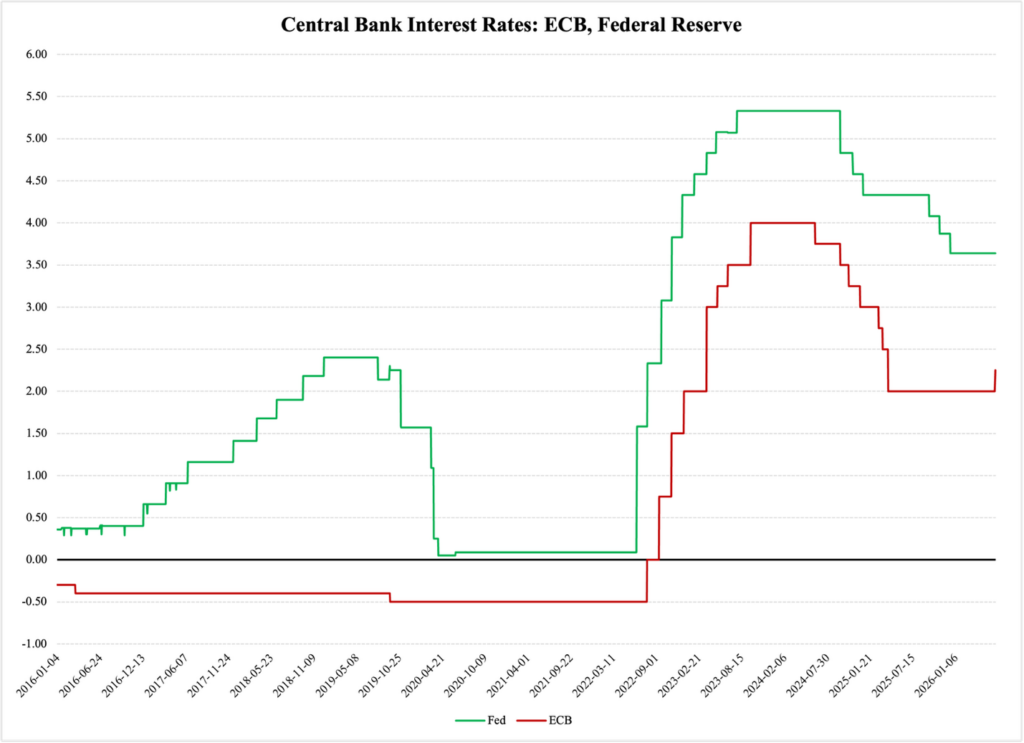

The Fed’s decision was unusual. As Figure 1 reports, these two central banks have coordinated their interest-rate decisions over the past few years and done so with almost uncanny precision:

Figure 1

By not raising its interest rate at this week’s policy meeting, the Federal Reserve has allowed for a much-needed strengthening of the euro vs. the dollar. That was not the explicit purpose behind the Fed’s decision, but it was such an obvious consequence that it cannot have escaped the Fed’s policymakers.

The euro is in much need of stabilization and appreciation, and more so in the coming months than at present. While the euro zone economy is for the most part standing still, the American economy is moving forward with relative ease. It is experiencing a reinforced inflow of investment money due in part to President Trump’s tariff revisions. With imports becoming more expensive as a result, there has been a rise in U.S.-bound foreign direct investment and in repatriation of capital by American companies.

Altogether, this puts appreciation pressure on the dollar. In addition, there is an ongoing U.S. stock-market bonanza, driven primarily by AI giant Nvidia and the market introduction of Elon Musk’s multi-tech company SpaceX. Although a stock market cannot forever live off the expected profits of two corporate behemoths, the current Wall Street boom is showing no real signs of abating.

When the conflict in the Middle East winds down, oil prices return to more normal levels, and the conflict-related overall uncertainty subsides, America’s relative economic strength will benefit the dollar at the expense of the euro. This creates a major problem for the European Central Bank: stagflation, or the combination of rapidly rising prices on the one hand and high, unyielding unemployment and idling productive capital on the other.

Stagflation is a danger that can sink even the strongest economies. It neutralizes the effects of traditional fiscal and monetary policy. You cannot cut taxes or increase government spending to help the economy grow, as such expansionary fiscal policy measures would only reinforce inflation. On the monetary front, you cannot cut interest rates for the very same reason, but also because—again—rate cuts rapidly lead to additional imported inflation.

In the past, I have criticized both the ECB and the Fed for refusing to mention ‘stagflation’ in their policy documents. I maintain that criticism: it is abundantly clear that the fear of stagflation is driving ECB policies right now. By discussing the problem openly, the central bank could gain a great deal more sympathy from Europeans in general when it is forced to make a painful decision, such as raising interest rates when the very core of the euro zone is suffering from unending economic stagnation.

A public debate over this problem is obviously needed not only to fend off stagflation itself but also because stagflation can rapidly aggravate another, even more serious problem threatening the euro zone. This problem is existential in nature and in itself a pressing reason for short-term increases in interest rates. If not addressed properly, it could lead to a fracturing of the euro area—and at least in theory, it could grow to such proportions that the common currency itself is in jeopardy.

This potentially existential threat to the euro zone emanates from the diverging growth rates I discussed recently. The core of the euro zone economy is standing still, while a group of countries on the outer rim are seeing their GDPs expand and, over time, their job growth accelerate.

When a group of countries decide to share currency, they also de facto decide to coordinate economic policy over a range of issues: taxes, government spending, the labor market, even foreign trade. Back in December, I explained the economic theory behind this need for sweeping policy coordination and how the euro zone cannot live up to these coordination requirements.

In addition to policy convergence, a currency area is strengthened by the convergence of economic growth rates. Today, the euro zone is experiencing growth divergence, the very opposite of what it needs to remain cohesive and free of structural frictions. If stagflation sets roots in the euro zone, its consequences will be felt more strongly in countries where GDP is already growing at anemic rates. This will exacerbate the differences between the moderately successful economies and the ones that are deeply troubled by stagnation.

So far, growth divergence is only a moderate empirical problem for the euro zone. It will take a couple of years of increasingly conspicuous differences in GDP growth before there are any visible signs of fracturing in the euro zone. At the same time, if the ECB cannot fend off stagflation—if the stagnant core of the currency area is plagued by rapidly rising prices while large swaths of its population are unemployed—the existential threat of economic divergence will rapidly become more serious.