In line with my prediction from April 14th, Hungary’s incoming Tisza government is going to make euro accession a top priority. A day after my article, hvg.hu reported that Tisza’s prospective finance minister András Kármán has been consulting with Mihály Varga, the president of the Hungarian National Bank, about a path for Hungary into the euro zone.

I cannot let go of the feeling that the incoming Tisza government wants to bring Hungary into the common currency as fast as they possibly can. It would make sense from an accomplishment viewpoint: the adoption of the euro is one of the most irreversible policy reforms a country can make. Once a country gives up its own currency, that is it; like the rest of the euro zone members, Hungary will be stuck under the monetary boot of the European Central Bank.

A fast-tracked Hungarian euro accession would certainly be in line with the ambitions of Brussels. Official statements from Tisza, on the other hand, are trying to place focus on some ‘euro by 2030’ plans. According to Karmán, it is realistic to expect the monetary transition to take four years.

One reason would be that it takes time to transition Hungary out of some price controls, e.g., on gasoline. Another reason is the set of accession criteria that the euro zone requires—most prominent among them are the limits on the government deficit and debt at, respectively, 3% and 60% of GDP. Adjusting Hungary’s fiscal balance to align with such criteria is indeed going to require difficult policy revisions, with the euro taking precedence over domestic policy priorities.

Bluntly speaking, in order to bring Hungary into the euro zone, the Tisza government will have to reduce support for Hungary’s families and raise taxes at a time when the Hungarian economy, if anything, needs lower taxes.

However, as difficult as it is going to be to bring Hungary into euro zone accession compliance, the major economic problems show up after the euro has been adopted. The loss of monetary freedom is an underestimated consequence of European integration. It is one of the factors behind the decline in GDP growth in almost every country that has joined the euro zone.

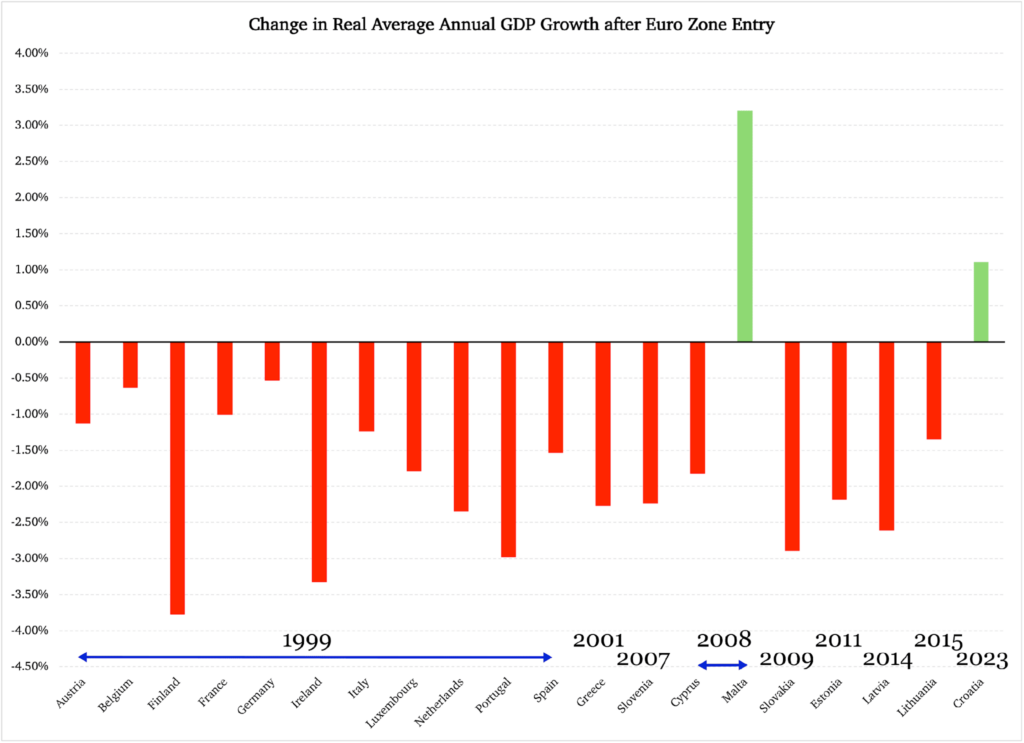

Figure 1 reports the difference in pre-accession to post-accession average annual, inflation-adjusted GDP growth in 20 euro zone countries. (Since Bulgaria joined in January this year, there is no post-entry data on their economy yet.) The consistency is downright frightening: in 18 of the 20 countries, average annual economic growth has declined, and often by substantial numbers.

The pre-euro period starts in 1996 and ends in 2025. Some examples:

The countries reported in Figure 1 are arranged by euro entry date. This reveals that there is no difference between countries that have been in the euro zone for a long time and those that entered relatively recently.

Figure 1

Source of raw data: Eurostat

The only countries that stand out in the opposite direction, Malta and Croatia, are more of statistical anomalies than anything else. They are not suitable as indicators of how the Hungarian economy would fare in the event of euro accession:

Hungary has a diverse economy that in its industrial composition is better compared to Austria, the Netherlands, or Slovakia than to Malta or Croatia. However, even if we disregard the value-added industrial nature of an economy, the brutal statistical message of Figure 1 is that there is a 90% chance that Hungary will suffer a permanent downgrade of its economic growth rate.

But does it really matter how much GDP grows every year?

Yes, it matters a great deal if the economy is growing or not. A country like Hungary is well suited to tell the difference between stagnation and growth: during the years of communist rule, there was no discernible change in the standard of living among the Hungarian people from one decade to another. The Marxist economic model applied by the communists is intrinsically averse to economic growth; it does not even recognize that the economy can expand, i.e., that businesses can do more with fewer resources.

Although the cause of economic stagnation would be very different under a euro entry, the consequences of a stagnant GDP would be largely the same: no progress for households in the standard of living and no incentives for businesses to improve their products and find ways to do more with less.

On a continent-wide scale, this is essentially where Europe finds itself today. When the phenomenon is caused not by communist dictates but by clumsy economic policy under democratic governments, we can refer to the problem of economic stagnation as a state of industrial poverty. Unlike deeply poor countries, which lack most or all of the basic conveniences of a life in an industrialized economy, the people of a country in industrial poverty have those conveniences.

However, without sustained economic growth, there are no economic incentives for entrepreneurs or investors to improve on anything. Businesses bring in capital only to replace old machinery and other items that wear out. There is no basis for raising wages and salaries, for hiring more people, or—over time—to even maintain productive activity in all industries.

A slow decline begins—one that we are already seeing in other parts of Europe. Germany is undergoing a structural industrial decline, and the culprit is its perennial economic stagnation. It is fair to say that Germany is in a state of industrial poverty.

Who are the biggest losers under perennial economic stagnation? The young. When they lose all opportunity to get ahead economically, they lose hope in their own future. When they lose that hope, they lose faith in their own nation.

There is a lot at stake here for Hungary. An entry into the euro zone would inevitably roll back the remarkable economic achievements built over 16 years with a Fidesz government. And that would just be the beginning of Hungary’s economic problems under the boot of the European Central Bank.