White House Press Secretary Karoline Leavitt, holding up a sheet showing global interest rates and a message from U.S. President Donald Trump to Federal Reserve Chair Jerome Powell, speaks during the daily briefing on June 30, 2025.

Andrew Caballero-Reynolds / AFP

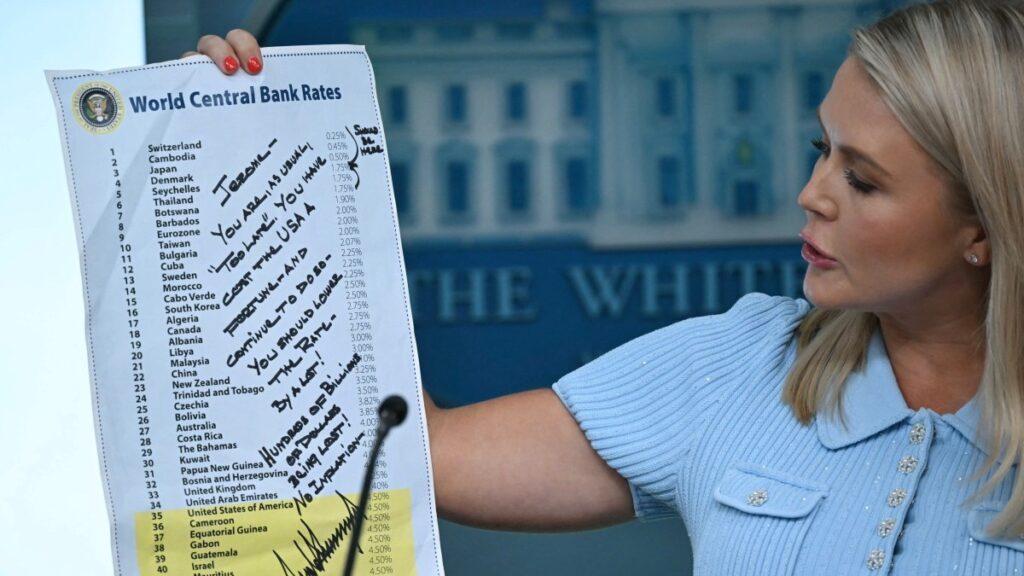

President Trump thinks America deserves to have the same low central-bank interest rates as Switzerland does. He recently put a number on what he envisions, ‘encouraging’ the Fed to lower its funds rate to 1-2% from today’s 4.33%.

This would require a major expansion of the U.S. money supply. You don’t have to be an economist to understand the close connection between money printing and inflation, but unfortunately, it seems as though Trump ignores that connection. But his ignorance does not stop there: he wants the lower interest rates to cut the cost of the federal government’s enormous debt.

In short, the president is getting frightfully close to opening the biggest possible inflationary floodgates in the economy.

Trump’s calls for lower interest rates are so strong, and so intertwined with his criticism of Jerome Powell, the current chair of the Federal Reserve, that it is basically a done deal that Powell’s successor—who will take office no later than May next year—will be the president’s money-printing puppet.

Here is why this is so dangerous: Interest rates are currently high on U.S. debt in part because the Federal Reserve keeps its funds rate high. In part, the rates are kept up by investors in the market for U.S. government debt. Investors simply do not have the level of trust in the solvency of the U.S. government where they are willing to buy our debt at lower interest rates.

For this reason, if the Federal Reserve did what Trump wants it to do and cut its funds rate to 1.5% (the median of his 1-2% range), it would scare away large amounts of investment money. At this point, there is only one investor who can step in and buy the U.S. Treasury’s debt securities.

That ‘someone’ is the Federal Reserve. Over the past 20 years, it has become the ‘buyer of last resort’ of our government’s debt, and it will resume that role again if Trump gets the Fed to cut rates the way he wants them to.

Since the Fed buying government debt is rocket fuel for inflation, I decided to crunch the numbers to see what inflation levels Trump may bring with his next Fed chairman appointment. I present those numbers below, including an overview of how I reached them.

There is nothing strange in itself that a central bank like the Federal Reserve prints money. That is a normal function of a central bank: it expands the money supply to make sure there is enough liquidity in the economy. Liquidity is money as we think of it traditionally—cash and checking deposits, plus various forms of consumer credit that can be used for daily purchases. It is one of the key duties of a central bank to secure an appropriately sized money supply.

So long as the central bank fulfills this ‘normal’ function and does not print more money than what the economy needs for its regular transactions, everything is fine. Those regular transactions are consumer spending, businesses paying their bills (including their employees), banks issuing credit, and the regular government expenses. But when the money supply grows bigger than this so-called transactions demand for money, there is an emerging risk of inflation.

Any money printed for purposes other than liquidity for transactions is filed under the so-called ‘speculative demand for money’. This type of demand is pretty much what it sounds like, and it leads to inflation in three steps:

A common use of this type of extra liquidity is to invest it in equity markets, or in something really safe: real estate or government debt. The more of this speculative demand for money that goes into buying government debt, the faster inflation will arise.

The reason why the purchases of government debt with borrowed money cause inflation is that government always spends the money it borrows. While private citizens often invest their borrowed money, government practically always uses it to pay for current expenses.

When government spends borrowed money, it creates more demand in the economy than there is supply. If the same government spending was paid for with taxes, then we would know there was enough supply in the economy to meet all demand. But when borrowed money pays for daily expenses, there is a shortage of supply—and a rapid rise in prices.

And just like that, we created inflation by printing money.

Now, back to Donald Trump and his requests for low interest rates. In order to push the federal funds rate from today’s level at 4.33% down to 1.5%—the average of his ‘envisioned’ 1-2%—the Federal Reserve would have to print money approximately the same way it did in the lead-up to the 2021-2022 inflation episode. That money printing started about a year before inflation took off; from the first quarter of 2020 to the first quarter of 2022, the Federal Reserve increased its money supply by 39%.

That number is probably an underestimation of the amount needed to cause high inflation; in 2019, the Federal Reserve had lowered its funds rate from 2.4% to 1.55%. In our scenario, where President Trump gets to dictate the Federal Reserve’s policy-setting funds rate, the drop to 1.5% has to come from a starting point above 4%.

At the same time, there is a higher degree of liquidity in the economy today than there was when the last inflation episode started. As of the first quarter of 2025, the money-to-GDP ratio (I prefer not to use the term ‘velocity’) is higher than it was when the Fed started printing money in unprecedented amounts in 2020. Therefore, in the calculations of the inflationary effects from President Trump’s desired interest-rate cuts, I assume a 31% increase in U.S. money supply over two years.

With an economy that is more sensitive to excess liquidity, where the price level is already a little bit elevated (compared to 2019), and where there is a higher risk for tone-deafness from the White House and Congress toward the first signs of a return of inflation, I would place my prediction of inflation in the 10-12% range.

Some economists, especially those with close ties to President Trump and his cabinet, will dismiss my prediction. I would just like to remind them that in early 2021, I was the first economist in the world to predict that the U.S. economy would see inflation in the neighborhood of 9%; the 9.5-10 percent range. The top, which came a year later, was just above 9%.

A return to high inflation would be terrible for America. It would certainly not be part of any agenda to ‘Make America Great Again.’ Inflation in the 10-12% bracket would erode the purchasing power of wages, and it would destroy private investment opportunities.